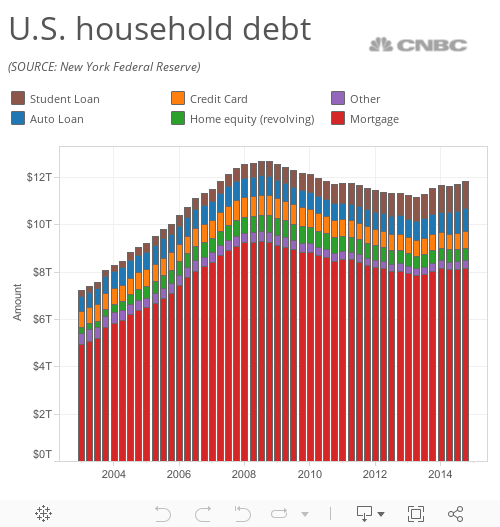

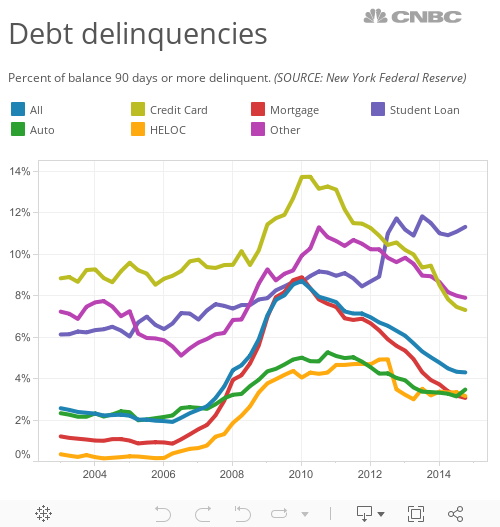

Even with an improved job market, those student loans are getting harder to keep up with.

While households are generally doing a better job making payments on their mortgages and credit cards, the delinquency rates on student loans worsened in the last three months of 2014, according a new report from the New York Federal Reserve.

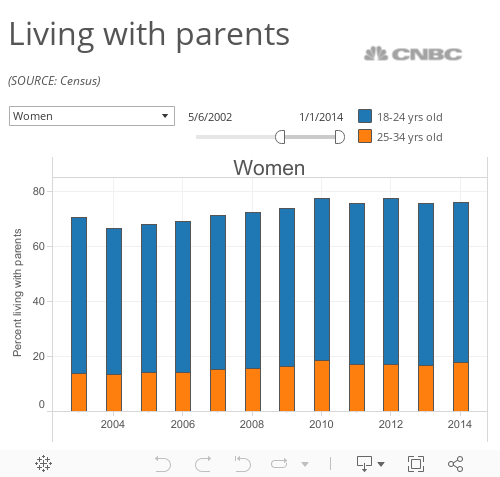

"Although we've seen an overall improvement in delinquency rates since the Great Recession, the increasing trend in student loan balances and delinquencies is concerning," said New York Fed researcher Donghoon Lee in a statement. "Student loan delinquencies and repayment problems appear to be reducing borrowers' ability to form their own households."