There is no way to sugarcoat this: The savings rate in this country is dismal.

In fact, Americans have done such a lousy job of saving for retirement that a majority of income in their golden years will have to come from Social Security benefits.

There is no way to sugarcoat this: The savings rate in this country is dismal.

In fact, Americans have done such a lousy job of saving for retirement that a majority of income in their golden years will have to come from Social Security benefits.

That's the bad news. The good news is, I found a glimmer of hope that some people do recognize that saving and investing can be a viable option versus buying a red sports car when they turn 50.

People, you either have money to spend on expensive toys or you don't. The problem is that credit cards, home equity loans and loose lending arrangements make it relatively easy for consumers at any income level to spend money they just don't have.

(Read more: Don't get blown off course by a windfall)

Put simply, regardless of how much people make, if they spend beyond their income, their finances will eventually fall into a downward spiral.

So while we live in a society addicted to conspicuous consumption, it's comforting to know that our CNBC audience is so much more savvy and smart than the rest of the country.

Let me explain.

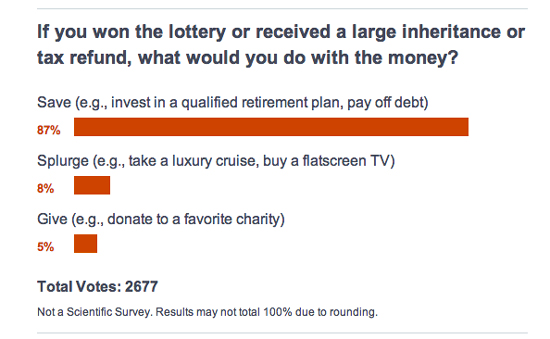

Last week we included an opinion poll in a guest column—"Forget flashy cars and save up instead"—from financial advisor Allan Katz. The question we asked was, "If you won the lottery or received a large inheritance or tax refund, what would you do with the money?"

While it was obviously not a scientific study, of the more than 2,600 people who responded, 87 percent said they would save (e.g., invest in a qualified retirement plan, pay off debt). Just 8 percent said they would splurge (e.g., take a luxury cruise, buy a flatscreen TV). Meanwhile, only 5 percent said they would give money to charity.

These CNBC readers—let's call them the 87 percenters—get it.

(Read more: How to grow your 401(k) at any age)

They are obviously savvy enough to understand that the path to a successful retirement is to save money now and to find a way to invest in a qualified retirement plan.

We are all aware that study after study has concluded that Americans are not prepared for retirement.

In fact, some recent research from the National Institute on Retirement Security reported that 90 percent of working-age households in the U.S. are not saving enough for retirement. Even more alarming, the study concluded that 45 percent of those households have nothing saved at all. Zip, zero, nothing.

The problem, of course, is that Americans have not adjusted to the fact that they have to personally take on the responsibility of saving for their own retirement.

(Read more: It's never too early to save for retirement)

It's all about a live-for-today attitude and not being concerned about what tomorrow brings.

Well, I am happy to report that the CNBC 87 percenters do understand proper saving habits. They understand that it's essential to save today for tomorrow's retirement.

Kudos to them!

The obvious question for the rest of America is: Should you try and find ways to save more money? Of course, you should; just ask the CNBC 87 percenters.

How much more clear can the answer be? Saving and investing and paying down debt will help secure a stronger retirement.

"By not planning ahead for retirement, those Americans will discover that they will be forced to work longer ... and will be forced to rely heavily on their Social Security benefits."

Other folks, not counted among the CNBC 87 percenters, are in for a rude awakening.

By not planning ahead for retirement, those Americans will discover that they will be forced to work longer (for example, well into their 70s) and will be forced to rely heavily on their Social Security benefits.

What's more, if and when they actually do retire, they will be forced to dial back on all those golden-years plans. The money they saved will never align with how much they'd believed they would be able to spend in their retirement years.

Let's face it: People fantasize about traveling to exotic places in their retirement. They dream of eating at fancy restaurants and enjoying the finer things in life that they could not do in their working days.

(Read more: Make sure your nest egg doesn't crack)

They envision themselves as the 60-something couple in those TV commercials who are yucking it up as they walk on the beach at sunset with their golden retriever. In reality, most will simply not have the funds to support that lifestyle. In fact, they will be lucky if they can support their current lifestyle—which includes no frills.

So while a majority of Americans may be facing a rocky retirement, the CNBC 87 percenters will be smiling as they watch that sunset from the beach.

—By Jim Pavia, CNBC.com. Follow Jim on Twitter @jimpavia.