Politics and the economy are both looking up. President Obama's big-government spending, planning, and executive-branch overreach were crushed at the polls, showing how elections really do matter.

The GOP has been rejuvenated, and Republican governors will lead the way. The Republican majorities in the House and Senate haven't been this big since the 1920s. They know what to do—develop a positive agenda that includes lots of 'pros': pro-growth tax reform and spending limits, pro-energy. Pro-strong dollar and Fed monetary reform.

Add on to that pro-health-care choice, pro-immigration reform and pro-marriage and family policies.

Read MoreElection changed little of nation's psyche: Poll

An American renaissance is in the making. Let the GOP put its best policy foot forward. If Obama vetoes the growth reforms, so be it. The 2016 agenda will be set for a Republican presidential victory.

So why can't 2015 be an optimistic year? The psychology of pessimism and negativism that has engulfed America for so many years can melt away overnight.

Retiring Oklahoma senator Tom Coburn recently told me that America is a better country than it is showing. I believe we are now poised to show it.

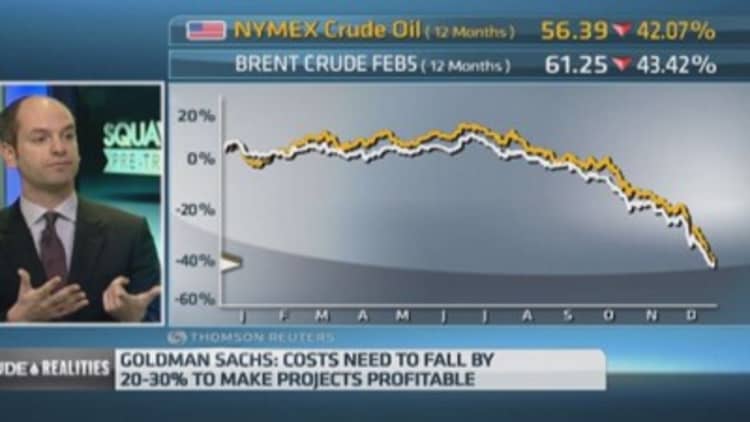

Inside the economy, things are looking better. Thanks to the fracking revolution, free-market forces have led to a halving of oil prices, to the enormous benefit of consumers and businesses. While our production cost structure for goods and services has plunged, America has become much more competitive.

Read MoreThe real silver lining of falling oil prices: Kudlow

Yes, inside the energy sector, there will be displacements. Marginal producers may fall away or consolidate. Extraordinary energy profit margins will normalize. There may even be some debt defaults.

Don't sweat oil's drop

Economist Scott Grannis estimates there's about $180 billion of high-yield energy debt. But only about $30 billion will likely default. That's a tiny fraction of $5.1 trillion in high-grade corporate debt, and an even smaller fraction of $28.3 trillion in U.S. Treasury, corporate, and mortgage-debt market value. Additionally, it comprises a small piece of the $23.4 trillion in U.S. equity-market value.

Forget the naysayers. There is no systemic energy banking risk that's comparable to the 2008 meltdown. Not even remotely. The energy supply shock is unambiguously good.

Lurking behind the energy-price drop (AAA gasoline nationwide is about $2.20, a buck less than a year ago), don't forget $3 , which is increasingly gaining energy-market share. Also, there's the matter of the economic havoc falling like boulders on our oil-producing enemies in Russia, Iran, and Venezuela. The U.S. energy revolution has done for national security what President Obama seems incapable of doing.

Read MoreLow oil good for Americans, not global growth: Pro

Then there's the economic power of the rising . 'King Dollar' is at an eleven-year high against its major counterparts. It's attracting capital from around the world. It's holding down inflation. It's providing major new purchasing power for consumers and businesses.

Lower production costs and commodity costs will increase our exports and give us more buying power for the purchase of imports. All this helps the global economic recovery.

Most people have this story wrong. It's not Europe and Japan that are going to hold the U.S. down. It's a resurgent America that's going to build them up—despite all their structural policy mistakes.

Also inside the economy, business investment is improving, housing is slow to recover but is recovering, and wage and salary income are finally growing at 4.5 percent. With less than 2 percent inflation on consumer prices, that leaves over 3 percent of real spending power. It may not be fabulous, but it is good.

Looking at Treasury bond yields, real rates are rising—a sign of better growth—while inflation fears are declining. Banking risk indicators, like 2-year swaps spreads, are very low. And profits, the mother's milk of stocks and the lifeblood of the economy, stand at a record-high share of growth. They are likely to keep growing in a 5 to 10 percent range.

Fortunately, the Federal Reserve's balance-sheet expansion never really worked. Excess bank reserves never circulated throughout the economy. The money supply has been quiescent. And that's a good thing, because if quantitative easing (QE) had worked, the inflation rate could actually have been 10 or 15 percent instead of less than 2 percent.

Meanwhile, the federal government's spending size has dropped from near 25 percent of GDP to less than 21 percent of GDP.

Obama's so-called spending stimulus has been stood on its head. In the early years more spending generated less growth—the worst recovery since WWII. But in recent times less spending is producing more growth—probably toward a 3 percent trend. (We need roughly 4 to 5 percent growth in the years ahead to reclaim America's 70-year average of 3.5 percent.)

A final optimistic thought: A big tax cut for large and small businesses combined with King Dollar is the exact supply-side-growth mix that generated booms in the 1960s, '80s, and '90s. We can do this.

Commentary by Larry Kudlow, a senior contributor at CNBC and economics editor of the National Review. Follow him on Twitter @Larry_Kudlow.