Sources: Freddie Mac, S&P Case Shiller and National Association of Realtors.

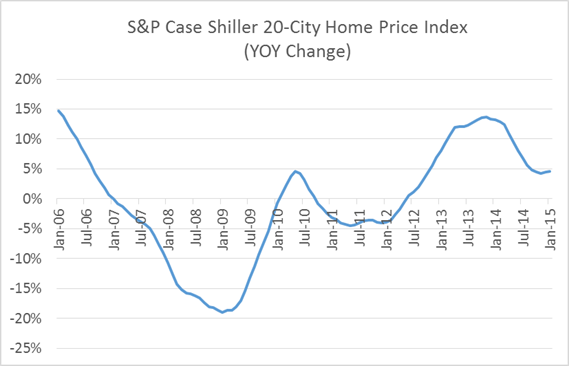

A recent article in the Wall Street Journal ("Spring Puts Bounce in Housing Market", by Spencer Jakab) discussed the positive housing-price data from S&P Case Shiller. Jakab attributed the stabilization in home-price growth to both lower mortgage rates (compared to a year ago) and looser credit conditions (federal agencies have relaxed the criteria for obtaining a mortgage). However, at the end, he cautions that, should 30-year mortgage rates go up 1 percent in the next year and housing prices rise 5 percent in that time, then a monthly mortgage payment would climb by a whopping 18 percent.

Read MoreA hopeful sign for housing

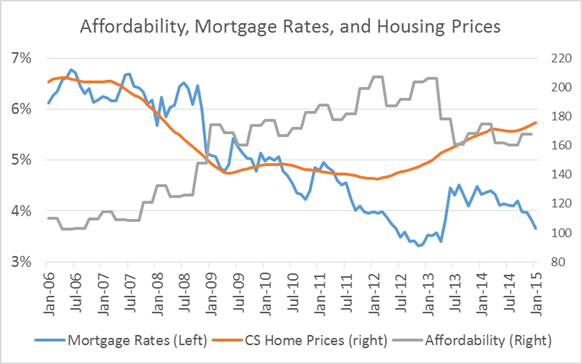

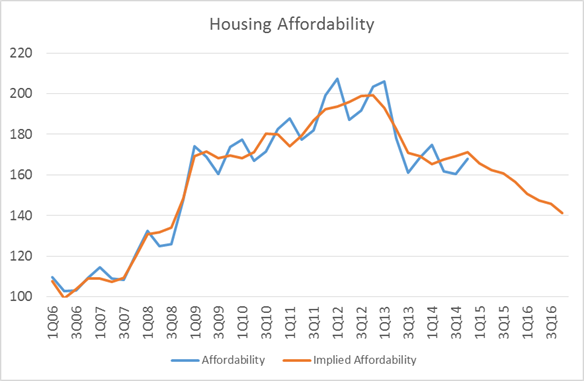

This is a fairly shocking statistic that supports our thesis that the economy's growth potential is capped for the foreseeable future. Growth in an economy as heavily dependent on loose credit conditions (read: low interest rates) cannot possibly be expected to accelerate if/when interest rates start to rise, even moderately. To illustrate our point further, the chart below shows the results of a regression analysis we did using the two most important determinants of housing affordability — housing prices and mortgage rates — to predict the NAR's Housing Affordability Index through 2016.

The blue line represents actual historical levels for the Housing Affordability Index as reported by the NAR. The orange line represents affordability levels produced by us through regression analysis using 1) actual historical data for mortgage rates and housing prices through the fourth quarter of 2014; and 2) assumptions for mortgage rates and housing prices for 2015 and 2016. If we make the assumptions that 1) housing prices grow 5 percent annually in 2015 and 2016; and 2) mortgage rates drift 1 percent higher in equal increments through 2016, then our regression predicts that the affordability index will decrease to about 140 (a level last seen in 2008) by the end of 2016. Does anyone believe that housing prices will keep going up if we are face with another 16-percent drop in affordability on top of the 23-percent drop since the first quarter of 2012? I sure don't.