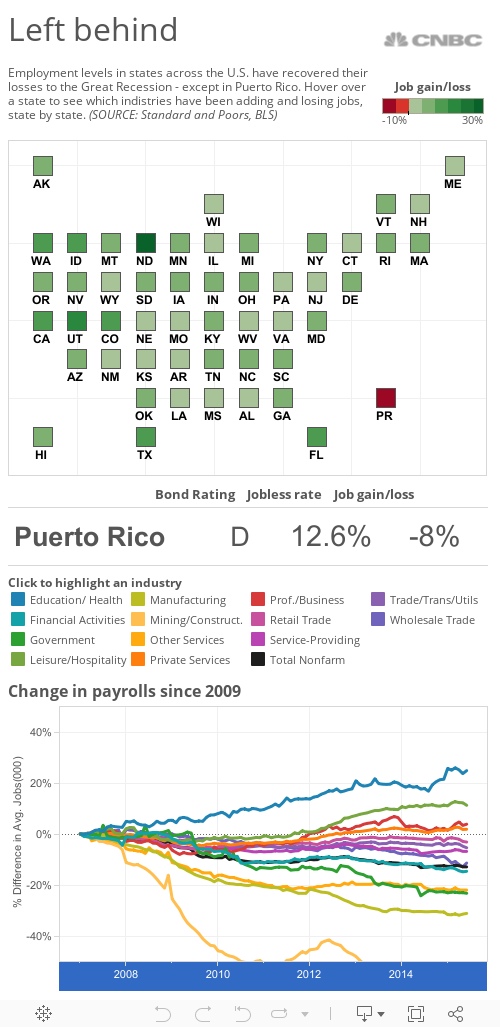

It's about jobs.

Since the Great Recession ended, employment levels have recovered on most of the U.S. mainland, and companies have added to payrolls. Jobs gains have ranged from just above breakeven in states like West Virginia to North Dakota's big, 28 percent boost, which came thanks to the boom in oil and natural gas exploration in that state.

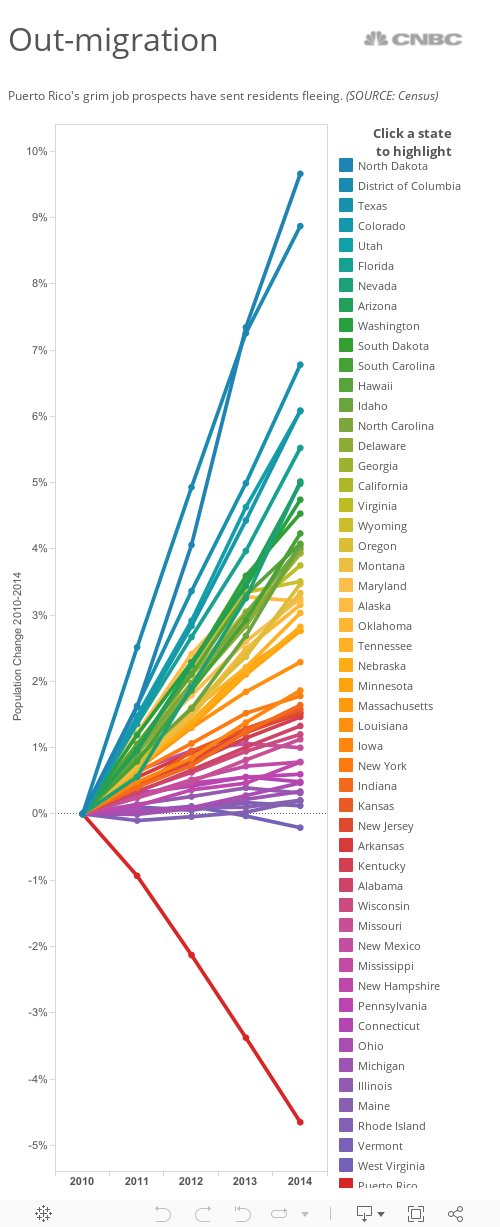

But Puerto Rico's job base continues to shrink, taking its economy along with it. Since the recession ended, overall payrolls have contracted by 8 percent, as a lack of job prospects has sent many Puerto Ricans fleeing to the mainland, where the job market is much stronger.

The out-migration began before the recession sent the U.S. economy into reverse in 2007. From a peak of 3.8 million in 2004, Puerto Rico's population fell to about 3.5 million last year, according to census estimates, marking a fall of roughly 8 percent.