Under normal circumstances, most people spend very little time reviewing their workplace health-care benefits during the open enrollment period.

This year, amid the coronavirus pandemic, employees should take a longer look.

"Something that wasn't important to you in the past may be important to you now," said Paul Fronstin, director of the health research and education program at the Employee Benefit Research Institute.

Typically, open enrollment starts in mid-October and runs through early December, but getting a head start will help. Here are a few things to look out for:

1. Health insurance

Health insurance is the most significant component of your benefits — this year and every year.

For starters, consider what your coverage costs you now that premiums and deductibles have been going up.

Annual family premiums for employer-sponsored health insurance — the amount you pay each year for insurance, often divided into 12 monthly payments — rose 5% to more than $20,500 last year, according to the Kaiser Family Foundation.

On average, workers paid $6,015 toward the cost of their coverage, while employers paid the rest.

More from Invest in You:

Picking the best retirement savings plan for you

Hidden fees are taking a bite out of your retirement savings

With remote work flexibility, some people opt to relocate

In addition, more workers have a deductible — the amount you pay before coverage kicks in — and that deductible is rising, as well. In 2019, the average single deductible was $1,655 for workers who had one, twice what it was a decade ago.

"You should always look at what's being offered to you and whether or not that's the right plan, Fronstin said. "It all depends on how often you are going to the hospital or if you will see more doctors or take expensive prescription drugs."

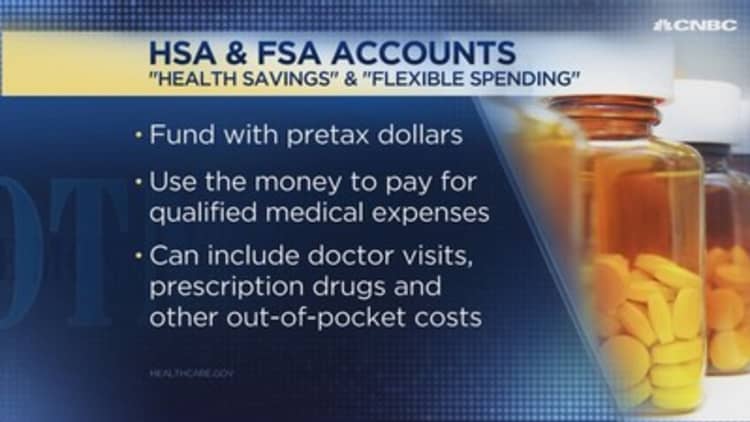

2. Health savings accounts

One way to help with health-care costs is by looking for ways to use tax-advantaged accounts for medical expenses — specifically, health savings accounts or flexible spending accounts.

In both cases, you use pretax money to cover out-of-pocket expenses, including doctor visits and prescription drugs.

To be able to use an HSA, you need to be enrolled in what's called a high-deductible health plan, or HDHP. Contributions then grow on a tax-free basis, and any money you don't use can be rolled over year to year.

You don't need to have a high-deductible plan in order to be eligible for an FSA — in fact, you don't need health coverage at all to sign up for one. However, you generally must use the money by year-end or you lose it.

3. Life insurance

Nearly half, or 45% of U.S. workers don't have or don't know if they have life insurance, according to a recent survey by employee benefits provider Unum.

"It feels a little morbid but it's really important that people have adequate life insurance," said Rob Hecker, vice president of global total rewards at Unum.

Even if you do have a life insurance policy through work, it could be a fraction of what you need to protect young children or other dependents.

Hecker recommends having a life insurance policy that's seven to 10 times your annual income to protect your family from financial fallout.

Consider what's the right amount for you, then weigh whether you want to buy additional coverage, or supplemental insurance, through your workplace group plan or shop for your own individual term life insurance policy, a move many advisors recommend.

4. Disability insurance

Disability insurance is often the most overlooked employee benefit. However, these plans can help replace a portion of your paycheck if you get sick or injured and can't work.

More than half, or 55%, of adults don't protect their income with disability insurance, Unum found. Seven out of 10 baby boomers also forgo this kind of coverage, despite being more likely to need it.

In general, plans will pay 40% to 60% of your salary and they are considered the most cost-effective form of income protection you can buy.

"Having a solid disability policy in place is fairly inexpensive," said Unum's Hecker. "I would certainly recommend that."

While you are at it, see if your employer offers other voluntary benefits.

Many companies have begun to include mental health services among health-care coverage options, as well as offerings such as teletherapy to help employees deal with work-life stressors and personal issues.

Before the coronavirus crisis, Americans were slow to pick up on the virtual trend. Now, nearly half of Americans said the pandemic was having a negative effect on their mental health — and employers are responding with a flood of mental health resources.

SIGN UP: Money 101 is an 8-week learning course to financial freedom, delivered weekly to your inbox.

CHECK OUT: My side hustles bring in $5,000 a month: Here's my best advice for getting started via Grow with Acorns+CNBC.

Disclosure: NBCUniversal and Comcast Ventures are investors in Acorns.