Most college students are better at spending money than saving it since they're not used to having money.

But it is crucial that college students start saving money now. Emergencies and unexpected expenses don't wait until you're established in your adult life to happen. They can happen at any time. And, what's more, the sooner you start saving and investing your money, the more you will have. And who doesn't want more money?

Love it or hate it, you need to know about money and how to invest it. That dictates many of the choices you make, from where you live to what you'll buy. Now, no one is saying you have to become an expert, but you have to know the basics, and it's important to start while you're still in college.

More from College Money 101:

An easy guide to help college students set up their first budget

How college students can start investing — and making — money

How I learned about investing in stocks — and you can, too

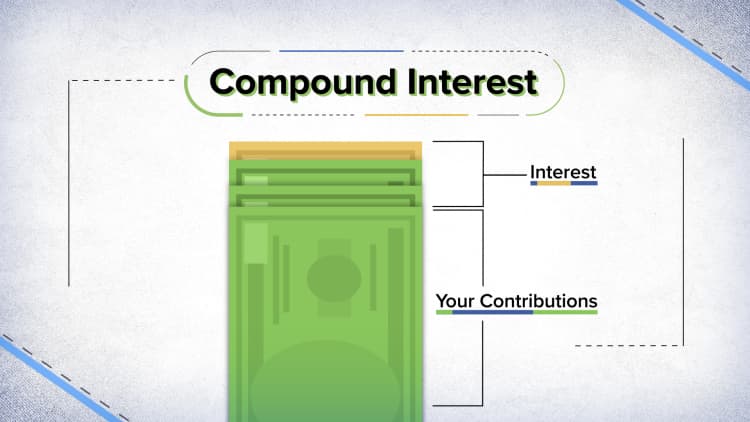

There's a saying in the investing community: "The best time to invest was yesterday. The second best time is right now."

What that means is that the earlier you are able to start, the earlier your money grows. This is done through the magic of compound interest! That means the money that you will be making when investing will grow exponentially based on the earnings made previously. It is what people mean when they say "make your money work for you."

Here's an example: Let's say you invest $1,000 in a stock and it goes up 5%.That's $50. Now your investment is worth $1,050. Let's say you make 5% the next year. That's now 5% of $1,060, which is $53. If you make 5% the next year, that's now 5% of $1,113, which is $56. Your original $1,000 is now worth $1,170. Now, imagine that over 20, 30 or 40 years. It adds up. By not investing right now, you are basically letting that money slip away.

A lot of people already have an intuitive sense of what to do with money, but they may not know or utilize the tools that can help grow that money exponentially.

It's not enough to just try to save or save when you get around to it. You need to make saving a habit and keep it going — and growing.

A simple way to do it is to use the 50-30-20 rule. This is where 50% of your income goes to necessities (such as rent, student loans and other bills), 30% goes to wants (such as that new pair of shoes or that spring break trip) and 20% goes to savings.

If you are a college student with a job or internship and you aren't able to save in this ratio right now, that's OK.

"When I was in med[ical] school, I was spending 95% on needs, 5% on wants. However, I knew that I would be able to use the rules of thumbs with a grain of salt since it didn't fit my situation," said Carolyn McClanahan, founder and director of financial planning at Life Planning Partners.

What's important is that you start saving some money. Whatever you can — $25, $50 or $100 — a month.

"The more you save, the sooner you reach financial flexibility," McClanahan said. "Having money set aside allows for more choice."

That means you will be ready for emergencies when they inevitably arise and you'll be able to afford more of the things you want.

One thing that helps is automating it. Just set it and forget it. Set up an automatic transfer of a set amount each month, and you'll be surprised how fast it grows. Then, check back in with yourself regularly (like you are your own financial advisor) and see if you can increase what you are saving. Even if you only increase it a little bit each month or every few months, it will add up.

How can you save and invest?

First, even if you don't have a lot of money to invest, it's important to split your savings into two distinct buckets — liquid and illiquid.

Liquid savings, in the simplest terms, means money you can access anytime. That's like your checking and savings accounts. This is for your day-to-day cash but also unexpected costs that may come up. You need to be able to either write a check or pay someone via payment apps like Venmo, PayPal, and Apple Pay.

What is the opposite of this? It's called "illiquid assets," and this is the type of money that you can't access so easily. This ranges from your stock/investment portfolio to even shoes you're trying to flip for a profit online. You can't just cash out of these things quickly, and in some cases, there are penalties for withdrawing too early if there is a fixed date on that investment.

Why would you want money you can't access quickly? Simple: It tends to generate a higher rate of return than a checking or savings account. But both are equally important to have.

If you have zero savings right now, the most important thing is to figure out how much money your bills are every month and start stashing away in a saving account or financial app three to six months of your expenses. So, if your monthly bills come to $2,000, then you need at least $6,000 in an account that you can access anytime if you need it. Even if that seems like a lot, set it as a goal and work hard to get there. Figure out where you can trim expenses even a little bit to stash more into savings.

"[E]veryone needs an emergency fund ... to able to breathe in case something goes wrong," McClanahan said.

Get in the right money mindset

My best tip is to keep your expenses consistent. You may have heard the expression "life is a marathon, not a sprint" — well that totally applies to your money, too. Think of the big picture, the long term. Sure, you will have a couple of anomalies, such as buying a new phone or laptop, but aside from that, keep your spending consistent. And that comes down to one word: discipline.

"Contrary to what some people may think, paying rent isn't that hard," said Dominic Wash, a psychology student in Michigan State University. "What's hard," Wash said, "is knowing how much you can afford to spend on things like going out and eating out."

"I've spent more on food than I do on rent and any other expense combined," Wash said. "It's not that I'm not able to budget my groceries; it's just that I need to discipline myself."

Erin Yi, a biopsychology, cognition, and neuroscience major at the University of Michigan, said it's also important to think of durability — how long something you buy will last vs. having to replace it, which means spending more money.

"When I'm shopping, I think about the long-term benefits," Yi said. "For example, I usually want to buy clothes for how long it will last me. I usually don't want to do fast fashion. With groceries, frozen food all the time. Even when I eat out, I try to calculate how much more I can stretch it out when I take it back home."

By actively seeking out the opportunities to save money, you prepare yourself for longevity, building up funds that can be used for better use. Now, this does not mean you can't treat yourself every once in a while! You can always go out and eat and go on a small shopping spree, but it is crucial to be proactive, keeping in mind how your decisions will affect your future.

Where to start

After you set up a savings account and build up a few months expenses in savings, think about using an investment account or app to get some of your money really growing.

The best thing to do is set up a self-directed stock account and set up automatic contributions, said Stephen Engel, a senior private wealth advisor at Palumbo Wealth Management.

"Start early, then learn," Engel said.

Of course, when you get your first full-time job, most of those will offer a 401(k) retirement plan with a matching contribution from your employer. Here, you are able to put your earnings into an account where untaxed money goes in, grows in the account, and then gets taxed later on when you withdraw it (in retirement). If you move to a new job, you can roll that over into an individual retirement account (IRA). You can also invest in what's called a Roth IRA, where there is a contribution limit but there are tax benefits down the road. The Roth IRA is different form a 401(k) as it allows you to invest earned income that has already been taxed. Both of them are great ways to put your earned income into stocks and let grow through compound interest.

Remember: Think big picture!

The best way to start learning about ways to invest is to start doing some online research. You don't have to spend hours studying — just read an article here, look up a term there. Keep at it, and that little bit of information gained will also grow over time.

Don't be afraid to make mistakes either! It can be nerve-racking to be clueless at the cost of your own money, but with the right amount of knowledge and common sense, you'll learn to manage those risks with your finances as well. Just don't invest huge amounts of money (not that most of us have it while we're in college) in any one place until you learn a little. Even then, it's smart to diversify: Have your money invested in a wide variety of things. That way, if any one investment falls, it doesn't take your whole life's savings with it.

Don't abuse credit cards

Credit cards are a necessity for establishing your financial history — and trustworthiness. If you have a credit card that you use and pay your bill on time every month, it shows that you are trustworthy when it comes to money. You will get a credit score based on that, and it will be something creditors look at throughout your life: when you go to rent your first apartment, buy or lease your first car or down the road, buy your first house.

"If you never had a credit card, that means you don't have credit history, so it will be difficult to buy house without a record," but "debt is a big problem," Engel said. "Never build up debt. If you set up a credit card with a $10,000 limit and you charged $10,000, interest will pile up."

The average credit card interest rate is 18.32% for new offers, according to WalletHub's recent Credit Card Landscape Report.

Credit cards charge what's called an annual percentage rate, so on $10,000, that's $1,832! You don't pay that all at once, a portion of that is charged each month on your monthly bill. But! That's not it. Remember how we talked about compound interest? How that can work in your favor when it comes to saving, investing and growing your money? Well, it works against you if you carry a balance. So, if you carry a balance month after month, it will keep compounding (you'll be paying interest on the original amount plus the interest charges you accrued last month and the month before, etc. It will be a lot harder to dig out of that cycle. So, start good habits early and don't carry a credit card balance.

Discipline.

One of the great things about graduating and starting your adult life is you get to make your own decisions about everything. But that also includes your money! So, you have to be smart about it. You don't want to be in a situation where you need to pay rent by midnight and you're wondering where that money is coming from. So, make sure you have a balance of liquid and illiquid assets in order to take care your life expenses now and your paradise in the future.

″College Money 101″ is a guide written by college students to help the class of 2022 learn about big money issues they will face in life — from student loans to budgeting and getting their first apartment — and make smart money decisions. And, even if you're still in school, you can start using this guide right now so you are financially savvy when you graduate and start your adult life on a great financial track. Jacob Shin is a senior at the University of Michigan, studying film, television, & media. He is an intern for CNBC's digital video unit. The guide is edited by Cindy Perman.

SIGN UP: Money 101 is an eight-week learning course to financial freedom, delivered weekly to your inbox. For the Spanish version Dinero 101, click here.

CHECK OUT: Calculate how much you need to save each paycheck to reach your money goals with Acorns+CNBC

Disclosure: NBCUniversal and Comcast Ventures are investors in Acorns.