By nearly every measure, the U.S. economy made a stunning recovery after the coronavirus pandemic spurred mass shutdowns and layoffs nationwide.

The labor market has added back millions of jobs and wages have gone up substantially, even among lower-paying positions.

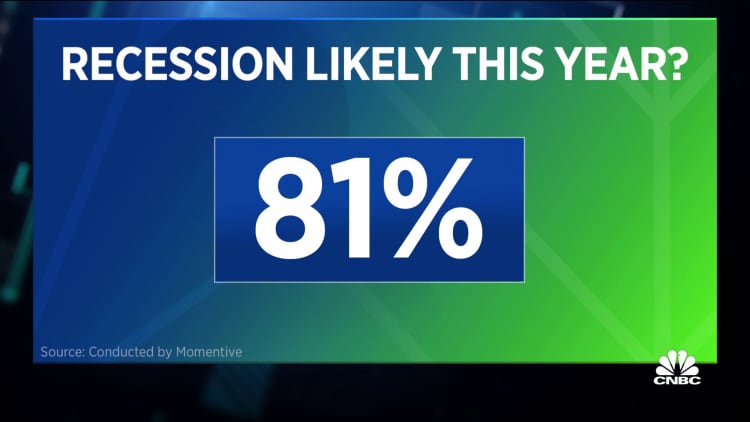

But soaring inflation and rapidly rising interest rates have most Americans worried that the good times will be short lived.

More from Personal Finance:

Emergency savings take a hit

Climbing interest rates mean good news for annuity buyers

It's a good time for young investors to put money in market

"Are we going to have a recession? It's pretty likely," said Larry Harris, the Fred V. Keenan Chair in Finance at the University of Southern California Marshall School of Business and former chief economist of the SEC.

"It's very hard to stop inflation without a recession."

To tame the recent inflationary spike, the Federal Reserve signaled it will continue to raise interest rates.

When rates are high, consumers get a better return on the money they stash in a bank account and must shell out more to get a loan, which can trigger them to borrow less.

"Rising interest rates choke off spending by increasing the cost of financing," Harris said.

There will be a day of reckoning, the question is how soon.Larry Harrisformer chief economist of the SEC

That leaves less money flowing through the economy and growth begins to slow.

Fears that the Fed's aggressive moves could tip the economy into a recession has already caused markets to slide for weeks in a row.

The war in Ukraine, which has contributed to rising fuel prices, a labor shortage and another wave of Covid infections are posing additional challenges, Harris said.

"There have been huge things happening in the economy and enormous government spending," he said. "When balances get large, adjustments have to be large.

"There will be a day of reckoning, the question is how soon."

The last recession took place in 2020, which was also the first recession some younger millennials and Gen Zers had ever experienced.

But, in fact, recessions are fairly common and prior to Covid, there had been 13 of them since the Great Depression, each marked by a significant decline in economic activity lasting for several months, according to data from the National Bureau of Economic Research.

Prepare for budgets to get squeezed, Harris said. For the average consumer, this means "they eat out less often, they replace things less frequently, they don't travel as much, they hunker down, they buy hamburger instead of steak."

While the impact of a recession will be felt broadly, every household will experience such a pullback to a different degree, depending on their income, savings and financial standing.

Still, there are a few ways to prepare that are universal, Harris said.

- Streamline your spending. "If they expect they will be forced to cut back, the sooner they do it, the better off they'll be," Harris said. That may mean cutting a few expenses now that you just want and really don't need, such as the subscription services that you signed up for during the pandemic. If you don't use it, lose it.

- Avoid variable rates. Most credit cards have a variable annual percentage rate, which means there's a direct connection to the Fed's benchmark, so anyone who carries a balance will see their interest charges jump with each move by the Fed. Homeowners with adjustable rate mortgages or home equity lines of credit, which are pegged to the prime rate, will also be affected.

That makes this a particularly good time identify the loans you have outstanding and see if refinancing makes sense. "If there's an opportunity to refinance into a fixed rate, do it now before rates rise further," Harris said. - Stash extra cash in I bonds. These inflation-protected assets, backed by the federal government, are nearly risk-free and pay a 9.62% annual rate through October, the highest yield on record.

Although there are purchase limits and you can't tap the money for at least one year, you'll score a much better return than a savings account or a one-year certificate of deposit, which pays less than 1.5%.