If you're looking for a relatively safe place for cash, Treasury bills have recently become more attractive, experts say.

Backed by the U.S. government, Treasury bills, or T-bills, have terms ranging from four weeks up to 52 weeks, and investors receive interest when the asset matures.

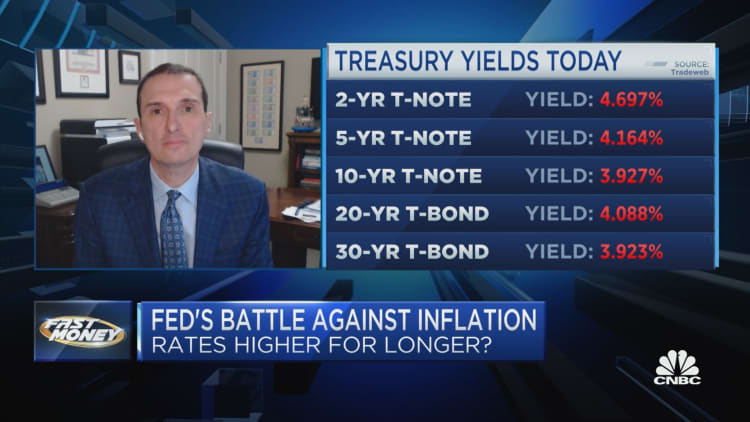

Over the past year, T-bill yields have jumped following a series of interest rate hikes from the Federal Reserve — with the possibility of more to come. T-bill yields have been low since the Great Recession, with the exception of 2018.

Treasurys

"I think people are shocked that yields are as high as they are," said certified financial planner Anthony Watson, founder and president of Thrive Retirement Specialists in Dearborn, Michigan.

Currently, shorter-term Treasury yields are higher than longer-term yields, which is known as an inverted yield curve. "What that means is the market is expecting rates to come down in time," Watson explained.

Still, T-bills yields are competitive when compared to other options for cash, such as high-yield savings accounts, certificates of deposits or Series I bonds, he said. Of course, the best choice depends on your goals and timeframe.

How interest rates affect bond values

Another factor to consider is the current economic environment, including future moves at the Fed.

That's because of the inverse relationship between interest rates and bond values. As market interest rates rise, bond prices typically fall, and vice-versa.

Duration, another key concept, measures a bond's sensitivity to interest rate changes. Although it's expressed in years, it's different from the bond's maturity since it factors in the coupon, time to maturity and yield paid through the term.

More from Personal Finance:

Federal 'baby bond' bill would give kids $1,000 at birth

Colleges to close even as top schools see application boom

How to access IRS transcripts for a faster refund

As a rule of thumb, the longer a bond's duration, the more likely its price will decline when interest rates rise.

But when interest rates decline, T-bills won't participate in that market value increase, Watson said. "They will start to underperform investment-grade corporate bonds once recession fears start to fade," he said.

How to pick the right T-bill term

While it's possible to sell T-bills before maturity, it can be tricky to pick the best term based on the current and future economic climate, experts say.

"It's always the Fed; the Fed controls short-term interest rates," said David Enna, founder of Tipswatch.com, a website that tracks Treasury inflation-protected securities and other assets.

He said the 26-week T-bill rates seem to reflect that investors expect continued rate hikes until that point. But terms past the 26-week, such as the 1-year T-bill, are "still pretty attractive."

However, the looming U.S. debt crisis may also affect investors' willingness to purchase T-bills maturing around the deadline, Enna said.

"It seems like a very small risk, but people will be aware of that as we get toward the summer," he said.

Correction: This story has been updated to reflect one of the terms for Treasury bills. An earlier version misstated the time frame.