"We're at an inflection point," said Kevin Logan, the chief United States economist for HSBC. "Debt is less of a burden" for households, he said.

Closely watched economic figures released Friday underscore households' nascent sense of strength. Despite tepid growth and still-high unemployment, consumer confidence has soared to a five-year high, according to a survey by Thomson Reuters and the University of Michigan. And economic growth numbers for the third quarter showed household spending picking up pace as well.

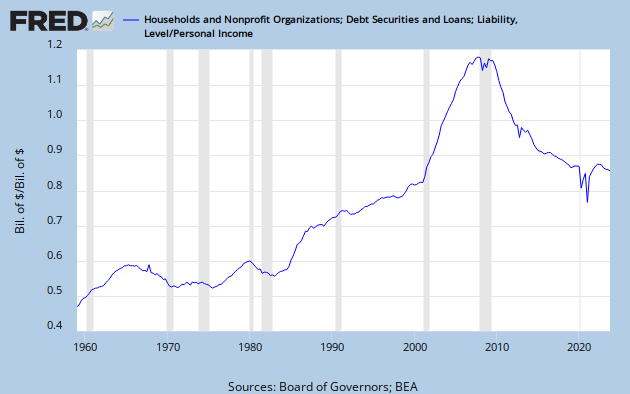

The drop in overall debt is in no small part because of foreclosures, delinquencies and write-offs by lenders which are slowing but not stopping. But the struggle to pay down old debts might not prove such a drag on economic growth in the future.

"We're not getting a tail wind. We're losing a head wind," said Mark Zandi, chief economist at Moody's Analytics, who said of the deleveraging process for households and businesses, "It's basically over."

Experts estimated that the overall level of debt, compared with income or economic output, would continue to fall for the next one to three years — with the earliest prediction for the end of deleveraging coming in mid-2013 and the latest at the end of 2015.

"By just about any metric, we've made a huge dent in a significant problem, but I don't think we're finished yet," said Liz Ann Sonders, the chief investment strategist for Charles Schwab & Company. "The distinction is that deleveraging will no longer be a big drag on the economy, like in the first couple years after the crisis."

In the run-up to the recession, American households took on trillions of dollars of debt that they could not easily afford, given tepid rates of wage growth. The collapse of the real-estate bubble and ravages of the recession have forced them to pay down or prompted lenders to write off more than $1 trillion of it, according to Federal Reserve data.

Still saddled with heavy debt burdens during the weak recovery, millions of American households cut back spending on food, cars and other goods. On top of that, relatively few families have been willing or able to take out loans or lines of credit. Thus, the proportion of household debt to personal income has fallen to its lowest level since the mid-2000s from its recessionary-era peak.

Now, with the economy more stable and interest rates at generational lows, Americans might finally feel more comfortable taking out a loan on a new car or putting money down on a mortgaged home. With their finances more in balance, workers might start spending less of their paychecks paying off old loans and more on leisure or household goods.

Given the importance of consumer spending to the American economy, those changes might translate into a more resilient economy, analysts said.

"Consumer spending still drives 65 to 70 percent of G.D.P. growth," Susan Lund, the director of research at the McKinsey Global Institute, said. "When deleveraging is over and housing picks up a bit, those two factors are going to be strong engines for the United States economy."

American households' biggest debt burden is in mortgages, given that a home is far and away the largest purchase the average family ever makes. As the foreclosure crisis grinds on, the total amount of outstanding mortgage debt continues to fall, Federal Reserve data shows, though more slowly than earlier in the recession.

A broader turnaround in the housing market, which seems to be in its early stages, might be helping to buoy consumers' confidence, economists said, as the combination of low interest rates, thawing credit conditions and an aggressive effort by the Federal Reserve has helped to put a floor under falling home prices.

"The Fed is redoubling its efforts to ease financial conditions right when the economy is getting into a better position, a position where it's more likely to respond to that easing of financial conditions," Paul Sheard, chief global economist at Standard & Poor's, said. "Those two things are dovetailing" and will help households in the future, he said.

Other parts of the household debt and spending picture are looking brighter as well, economists said. A September report by Equifax, a consumer credit reporting agency, showed that the total value of auto lending jumped nearly 14 percent year over last year, with sales of new cars and light trucks climbing sharply. In the first half of 2012, Americans took out more car loans than they had since 2007, before the financial crisis hit.

The trends look likely to continue, Equifax said. "The average age of cars on the road today in the U.S. is the highest ever recorded and consumers are ready to replace these older vehicles," Amy Crews Cutts, Equifax's chief economist, said in a statement. "The financial picture has improved sufficiently that we are seeing auto lending markets become facilitators rather than obstacles."

Americans have also improved their personal balance sheets by slashing their outstanding credit card debt to $855 billion today from more than $1 trillion in 2008, according to Federal Reserve data. But student debt has continued its inexorable march higher, a "worrisome" trend that economists say could stop young workers from starting new households or could eat into their spending on other goods and services.

How Americans feel about debt and credit in after the recession might determine how much debt they ultimately shed, Ms. Lund of McKinsey said. "The Great Depression scarred an entire generation," affecting how households borrowed and spent for decades, she said. "We don't yet know whether consumer behavior has been fundamentally changed by this crisis or not."

{kind=link}