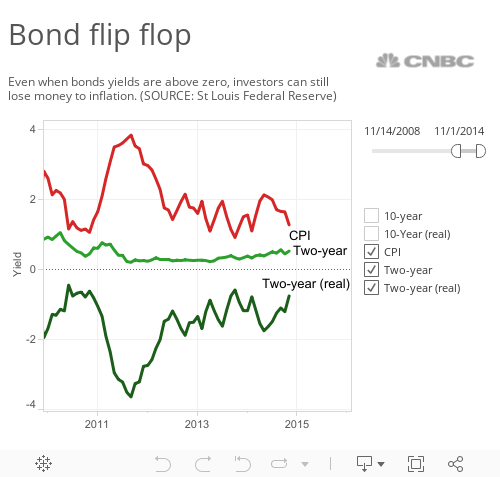

If the German government was thinking of borrowing more money, now would be a great time to do it. Demand for its debt is so strong, in fact, that investors are willing to pay the Bundesbank to take their money.

That's not the way a bond is supposed to work.

The stampede to buy German bonds comes as investors in Europe have plenty of other reasons to fear parking their money elsewhere, like stocks or corporate bonds. Europe' s economy is in the dumps, another Greek debt standoff looms, and sanctions against Russia are cutting into exports.

It's not the first time the yields on German bonds have turned negative, but the fact that the impact is hitting longer term issues shows just how jittery investors have become. (Usually, the longer an investor is willing to lock up their cash in a bond, the higher the yield they get paid.

Here's what's behind the German bond flip-flop.