Brother, can you spare a nickel?

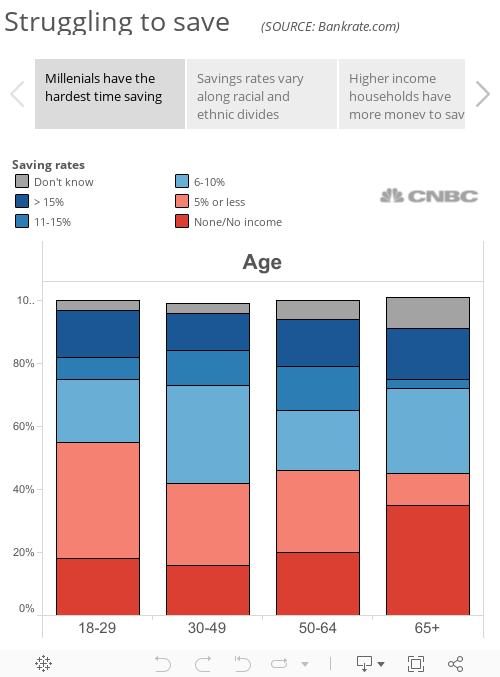

For roughly half of American households they answer is "barely," according to the results of a new survey by Bankrate.com. About half reported they are setting aside no more than 5 percent of their income in savings. One in five said they're not even able to save a penny.

The highest savings rates were reported by those in the middle of the income ladder; more than a third of households earnings between $50,000 – 75,000 said they're saving more than 10 percent of their incomes, a higher rate than those in the highest-income bracket.

Only a quarter of those surveyed are setting aside more than 10 percent of their incomes, including one in seven who said they are saving more than 15 percent of what they make.

a failure?")