When interest rates start rising in the U.S., it will hardly be a surprise.

Officials at the Federal Reserve have been warning for a year that the move is coming. But how, exactly, does a central bank like the Fed raise and lower the price of money?

When a supermarket wants to raise the price of a can of tuna fish, it just sends someone around to print new stickers and slap them on the cans. Gas prices go up and down so often that many outlets have installed electronic signs to change the numbers with a few keyboard licks.

Changing the amount borrowers pay and lenders collect is a little trickier.

Before you get to the "how"—how about explaining "why" the Fed wants to raise rates. Isn't cheap money good for everyone?

It's good for borrowers. That's why the Fed has been having a giant money sale since late 2008 when the bottom fell out of the global financial system. Since then, cheap dollars have flooded through the mortgage market (reviving a dead housing market), the stock market (rebuilding the damage to pensions and 401(k)s) and the bond market (helping companies and governments save money by refinancing their debts at much lower rates.)

Got a question for CNBC Explains? Please send it to explains@cnbc.com.

Cheap money is not good for savers, though. (That may be one reason so many people have put aside enough for retirement.) And now that the U.S. economy seems to be back on its feet, and employers are hiring, the Fed figures it's time to end the Money Sale and let interest rates float back up gradually

How does it do that?

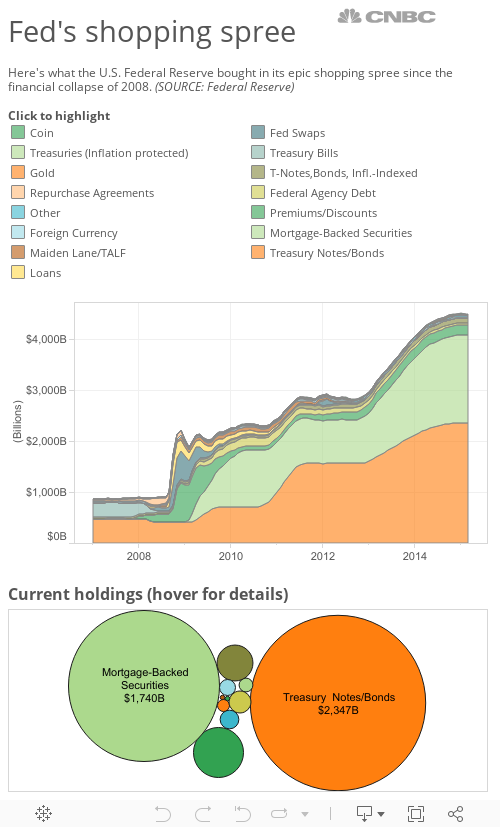

The first thing it did was to end its roughly $3.5 trillion shopping spree for Treasury bonds, mortgage-backed securities and other paper left behind by the lending binge that inflated the U.S. housing bubble.

A 10-year Treasury bond is just a 10-year loan to Uncle Sam from an investor. So interest rates on that 10-year loan are set by the market; rates rise when there are fewer buyers and fall when demand is stronger.

When it buys bonds, the Fed also pays cash to the sellers, which pumps money into the financial system and the economy. That cash is created with each new bond the Fed buys. (It doesn't actually "print money"; the number of paper dollars in circulation has no impact on interest rates.)

Once the Fed started buying every bond that wasn't nailed down, rates dropped to low single digits and stayed there. Now that the Fed has ended its bond shopping, rates are expected to begin rising again. So far that hasn't happened. But in the past, when the Fed wanted to raise long-term rates, it started selling some of its bond holdings.