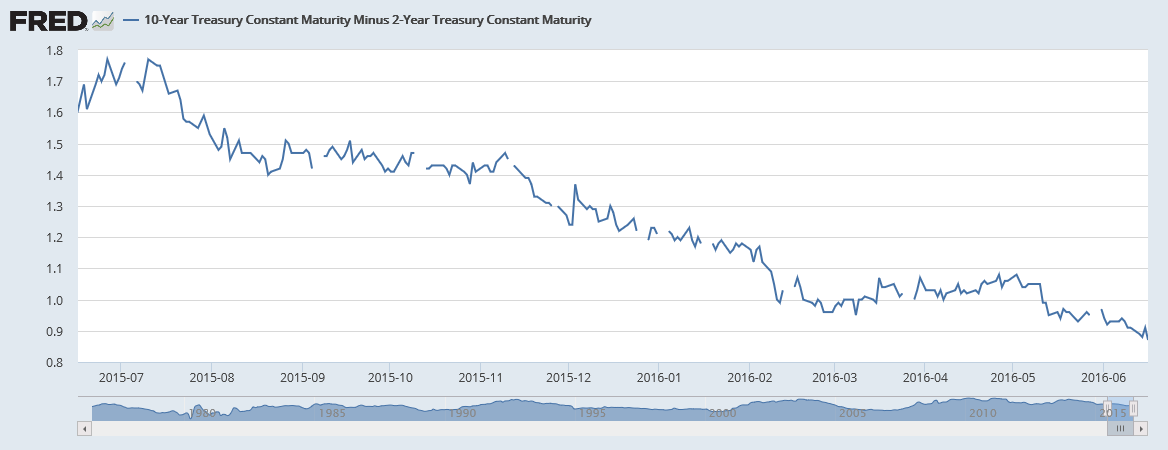

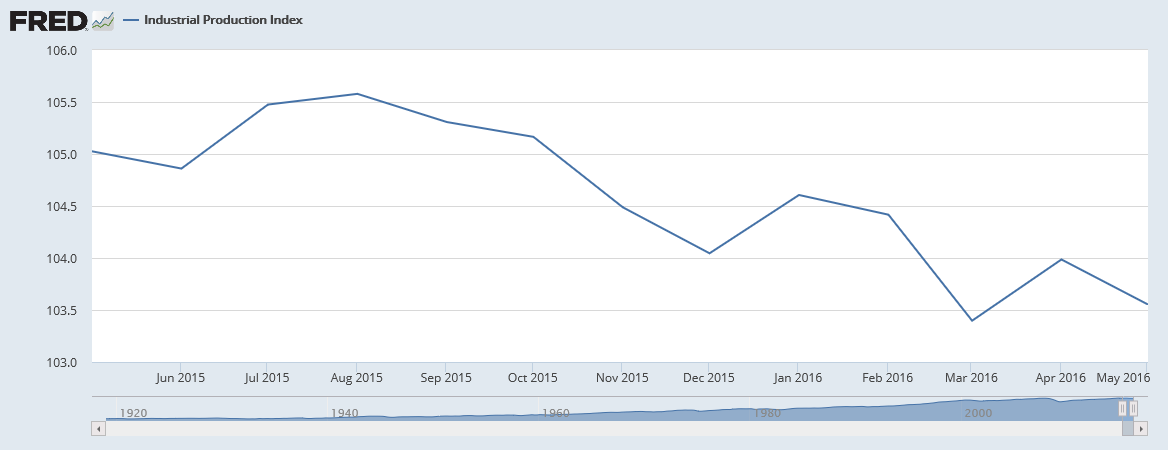

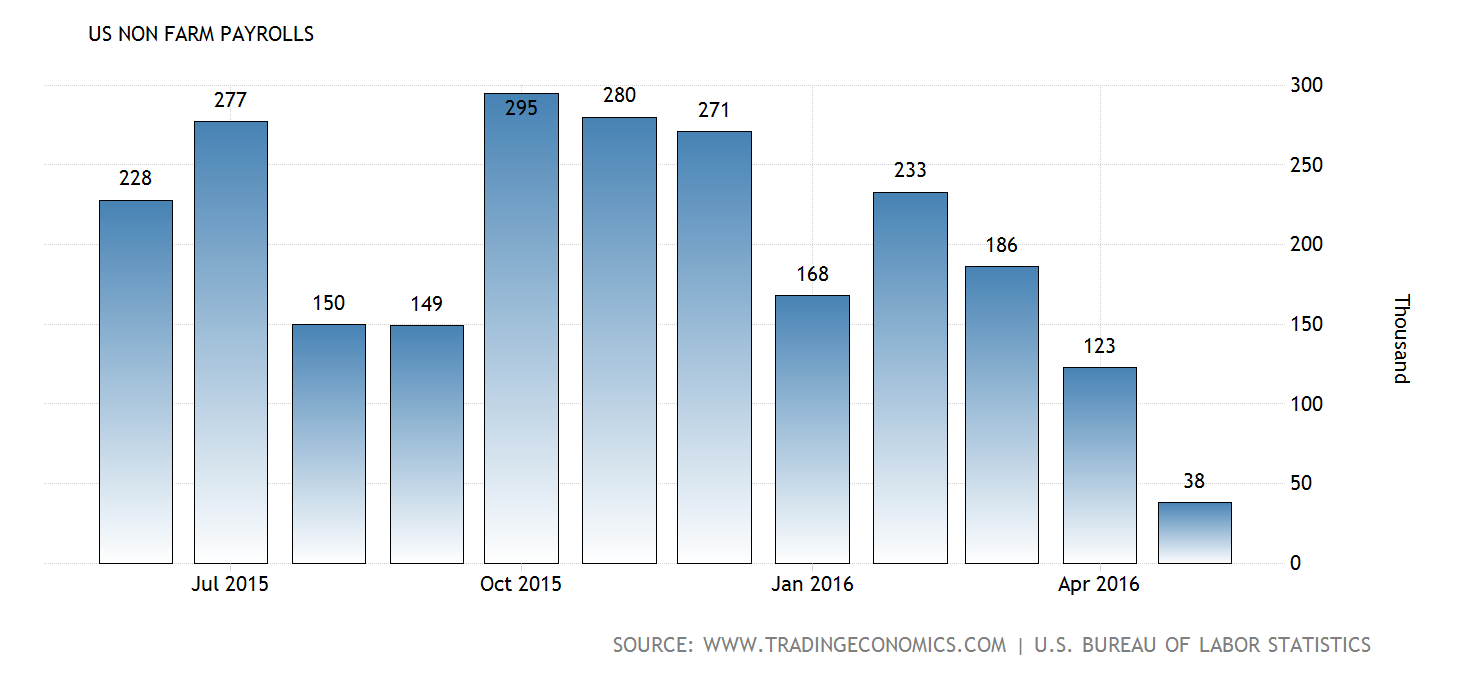

The falling copper price, tumbling global trade, a flattening yield curve, weakening industrial production and the rolling over of monthly job creation all point to an economy headed into contraction.

But as mentioned earlier, to confirm that this recession may have already arrived, we need to look no further than the data published by the Bureau of Economic Analysis (BEA) and the Bureau of Labor Statistics (BLS).

The definition of recession is two consecutive quarters of negative GDP growth, according to the National Bureau of Economic Research, though that is not an official designation. During Q4 2015 and Q1 2016, real GDP posted 1.4 percent and 0.8 percent growth, respectively—so officially we're not in one yet. However, when deflating nominal GDP by the core rate of Consumer Price Inflation (CPI) published by the BLS, you get real GDP of just 0.3 percent in Q4, and negative 0.8 percent during Q1. Therefore, the economy is dangerously close to a contractionary phase; and is already in one when averaging the prior two quarters (at minus 0.25 percent when adjusted by core inflation).

It took 1.5 years to bring the economy out of the Great Recession that began in December 2007. And it took a $3.7 trillion increase in the Federal Reserve's balance sheet, plus 525 basis points of interest-rates cuts to pull us out. The major problem is that stock market is now pricing in a strong recovery from the four quarters in a row that the S&P 500 has posted negative earnings growth. Another year, or more, of falling earnings for equities would result in a devastating bear market.

The Fed already has a bloated balance sheet in relation to GDP and only a few basis points to reduce borrowing costs before short-term rates hit zero percent. Therefore, there just isn't much the Fed can do this time around. Therefore, this next recession could last even longer than the previous one.

The stock market is pricing in perfection and is ill-prepared for a protracted recession that may already be underway. Prudent investors should hedge their portfolios now from such an unwelcome event.