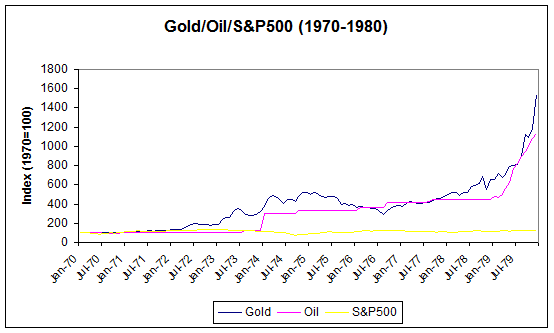

During the high inflation/low growth decade of the 1970's, investors sought protection in gold and oil. Attesting that as money flowed out of bonds, it didn't compulsively move into stocks.

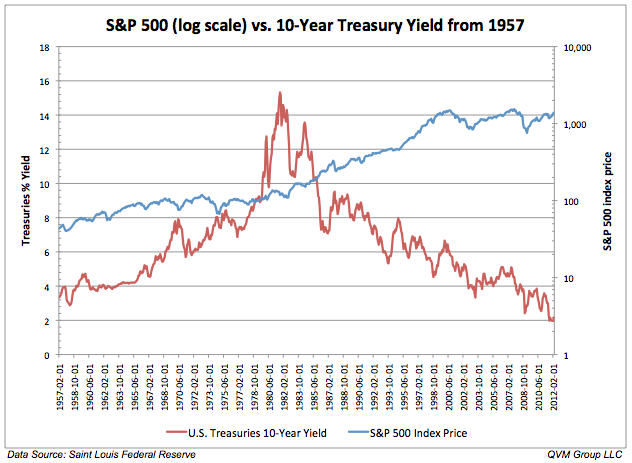

Therefore, a better way to think about the long-term relationship between stocks and bonds is that the bull market in bond prices helped to foster the bull market in the major stock averages. Or, that on average the stock market does better in a period of falling bond yields. Yet, Wall Street chooses to make the opposite argument to allay investors' fears as interest rates begin this huge secular move higher.

Escalating bond yields will finally break the 35-year trajectory of falling interest rates that has led to the decades-long bull market in the major stock market averages. At what yield this line officially breaks is up for debate. Bond King Bill Gross has indicated that 2.6 percent on the 10-Year Treasury will end the bull market in bonds. DoubleLine Capital's Jeff Gundlach argues that 3 percent is the level to watch. But both believe that 2017 will mark the end of the secular bull market in bonds; with Gundlach going out on a limb assuring it is "almost for sure" that the 10-Year is going to take out 3 percent this year.

This time around bond yields will initially rise for three reasons: the first because the credit quality of the government has been severely damaged as a result of the unprecedented amount of borrowing undertaken following the Great Recession, the second due to the fiscal profligacy proposed by President Trump, and third because our central bank has spring loaded interest rates by artificially holding them at record lows for the past eight years.

And that sets us up for the real surge in bond yields—yes, we haven't seen anything yet.

Rising borrowing costs should send our debt-saturated economy into a recession, which by the way is already way overdue. That recession, coupled with the massive fiscal and monetary response to it from President Trump—think massive deficit spending and helicopter money--should engender the second phase of soaring rates that will result from spiking inflation and soaring debt levels. This unprecedented period of turmoil will once again prove that rising bond yields are seldom good for stocks, especially in real terms. And the bursting of this historic bond bubble certainly won't be the exception.

Commentary by Michael Pento who produces the weekly podcast "The Mid-week Reality Check," is the president and founder of Pento Portfolio Strategies and author of thebook "The Coming Bond Market Collapse."

Follow CNBC's Opinion section on Twitter @CNBCopinion.