If ongoing congressional budget battles force a government shutdown next week, homebuyers and sellers could be subject to more headaches than usual before their deals close.

That's because buyers looking for mortgage approval could hit paperwork roadblocks if the shutdown furloughs workers at the IRS or Social Security Administration.

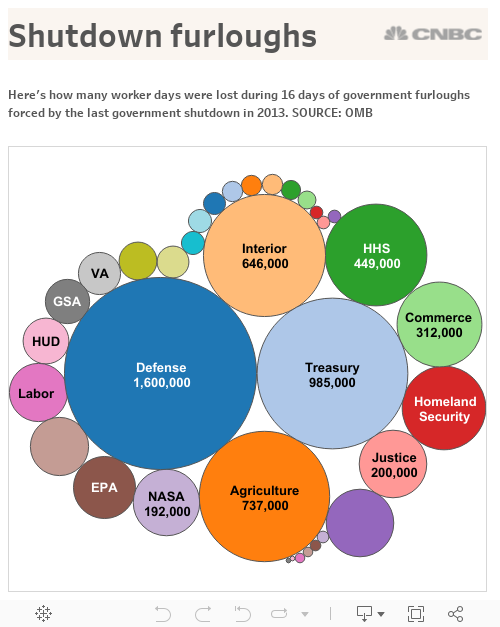

That's what happened in October 2013, the last time budget gridlock forced a 16-day shutdown that sent millions of government workers on furlough and gummed up the works of the U.S. housing market.

Here's how another shutdown could make buying or selling a home even more stressful.

Doesn't the bank decide whether I get a loan? Why does the government have to get involved?

While lenders use government guidelines for mortgage approvals, the decision ultimately belongs to the lenders. That's not the problem.

As anyone who has applied for a mortgage learns the hard way, the application includes a big stack of paper documenting your financial status, including records like tax returns.

In most cases, lenders want to verify all that paperwork, especially after the early 2000s mortgage-lending spree that went light on documentation, an approach that ended badly.

And if the government does shut down, that includes workers at the Internal Revenue Service who are usually asked to verify the tax returns aspiring homebuyers submit to their mortgage lenders. (If you hear there's a problem with IRS Form 4056-T, you may have hit that particular roadblock.)

If the government shuts down, do they really send everyone home?

Some of the more than 2.2 million government workers would be exempt from furlough, including those who provide essential services.

NSA agents would keep snooping on phone calls, TSA screeners would keep examining luggage, and air traffic controllers would show up for work, along with food safety inspectors, border patrol officers and federal prison guards, most FBI agents, doctors and nurses at the VA and other federal hospitals, and any federal emergency and disaster relief workers.

The U.S. Postal Service, which is funded separately, would continue to deliver the mail. And Federal Reserve officials would continue working because they draw paychecks from funds generated by interest on the central bank's assets.

But verifying information and processing mortgage paperwork isn't considered "essential." So those employees would have to stop working.

"There's no 'Wink-wink, keep your laptops and we'll call you,'" said Mortgage Bankers Association CEO David Stevens. "They're barred from the building and barred from using the network for access. So, you have a real shutdown."

What else can go wrong with my mortgage application?

Borrowers who are applying for an FHA or VA mortgage could run into delay if workers from those departments are sent home, and there's no one available to process the loan.

A loan could also be delayed if a lender tries to verify a Social Security number. That's often required if something in an application doesn't match the information associated with a Social Security number in a credit report or other database, even if it's just a typo. If the lender tries to verify the number with the Social Security Administration, and no one at the agency answers the phone, that borrower could be out of luck.

Last time around, the FHA put out an FAQ to help lenders figure out how to work around some of these roadblocks.

What if I can't get approved in time for my closing date?

It's possible the deal could fall through, but it's much more likely the contract will just be extended. The last time the government shut down, some 17 percent of closings were delayed, according to a December 2013 survey by the National Association of Realtors.

But a handful of transactions were scuttled, and a few sellers reported that they lost bids because of the shutdown. Some 3 percent said they got a weaker offer, likely because of the uncertainty buyers faced over the length of the furloughs.

One thing that has changed since the last shutdown: The housing market is stronger than it was in 2013, and the volume of mortgage applications is higher, Stevens said.

That means while the odds of any individual mortgage applicant hitting a roadblock would still be relatively small, the number of buyers affected would be greater this time around.