Leon Cooperman is addicted to investing.

The hedge fund manager's stock-junkie lifestyle starts at 5:15 a.m. on weekdays, when he wakes up in the Short Hills, New Jersey, house he's lived in for 36 years. He then drives to the Manhattan offices of his $10.7 billion Omega Advisors, getting in by 6:30 a.m. (he took the ferry for 30 years before the firm recently moved from Wall Street to midtown). Cooperman then digs in to investing for 12 hours—including a working lunch in the office—bouncing between grilling corporate executives in person or on the phone, consulting with his 18-person research team and reading company reports. By 6:30 p.m., it's off to a business dinner with more CEOs or fellow investors like Mario Gabelli of Gamco Investors and Bill Priest of Epoch Investment Partners. Then it's a quick post-dinner shower and more time in front of a Bloomberg terminal checking international markets before bed at 11 p.m.

"The way to be successful is do what you love and love what you do," Cooperman said this month in an interview. "I get paid normally a lot of money for basically doing something I enjoy doing. And what I enjoy is to hunt—finding something somebody else doesn't see, making a bet and having Mr. Market prove me right."

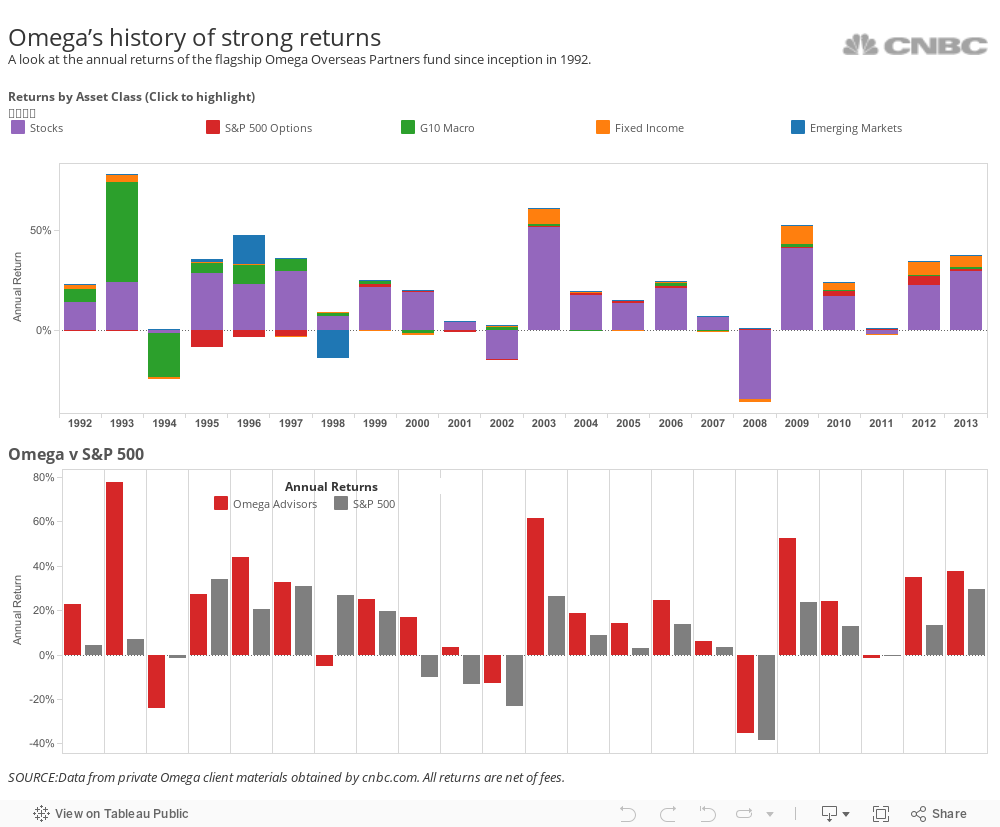

Mr. Market has indeed smiled on Lee Cooperman, making the 71-year-old South Bronx native a billionaire. A maniacal focus on picking undervalued companies combined with the hard work and frugality of someone who came from little have led to a nearly unparalleled track record of investment returns for longer than most people have worked on Wall Street.

Take Cooperman's recommendations at the Delivering Alpha conference, where he is scheduled to speak Wednesday. In 2012, Cooperman made 10 stock recommendations at the joint CNBC and Institutional Investor conference. All gained in value over the next year, many by double digits. In 2013, the hedge fund manager presented 10 more picks. Eight of them are winners.