Congress may have bailed out Wall Street and the auto industry, but it's apparently in no mood to bail out retirees at risk of losing their pensions.

After a flurry of last-minute, behind-the-scenes maneuvering, lawmakers Thursday finalized a deal to shore up the government's pension insurance fund by raising premiums and allowing troubled pension plans covering more than one employer to cut retiree benefits.

The provisions, which drew loud opposition from unions and other groups representing retirees, were expected to come to the floor for a vote Thursday as part of a massive, $1.1 trillion spending bill.

Proponents argued that the changes would keep the failing pension plans afloat and keep benefits flowing to retirees.

"We have a plan here that first and foremost works for the members of the unions, the workers in these companies and it works for the companies," said Rep. George Miller, D-Calif., who worked the deal out with Rep. John Kline, R-Minn.

But some union officials and retiree advocates like AARP slammed what they saw as a sneak attack on a decades-old promise to workers and their families.

"Today, we have seen the ugly side of political backroom dealings as thousands of retirees may have their pensions threatened by proposed legislation that reportedly contains massive benefit cuts," said Teamsters President James Hoffa.

Read MoreFed: Household net worth dipped for first time in three years

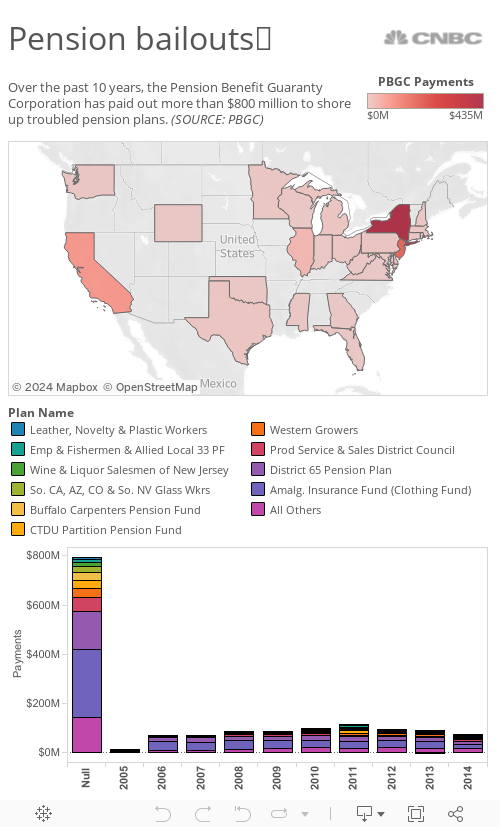

The fix proposed by Congress would allow employers to cut benefits to help cover higher premiums to shore up the Pension Benefit Guaranty Corp., the government insurance fund backing these plans.

"The problem is much more serious than skimming retirement benefits to keep the PBGC on life support," said Richard Greer, a spokesman for the Laborers' International Union of North America. This proposal "would siphon off tens of millions of dollars in hard-earned retirement benefits to try and rescue the PBGC."

There's wide agreement on one thing: The PBGC needs to be rescued before it collapses.