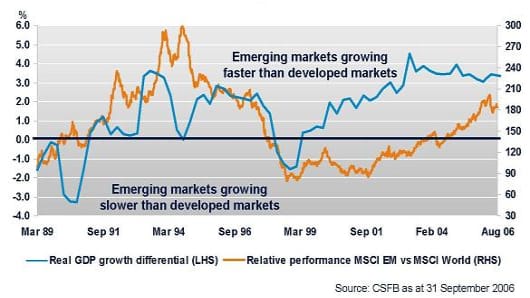

Global emerging markets, or GEMS, entice would-be investors with the potential of big returns. The growth of these markets over the past few years has been impressive. In 2006 alone, the MSCI Emerging Markets index rose 29%, led by an extraordinary 53% gain in its four biggest countries — Brazil, Russia, India and China (BRIC).

Over the short term, however, the risks of investing in emerging markets are high. Like any other economy, emerging markets go through cycles of boom and bust – except they are to the extreme. For example, the currency crisis that led to the collapse of Asia's stock markets in late 1996 and 1997 and the Russian debt default in 1998. The combined effect of these two events at the end of the third quarter 1998 almost halved the value of the MSCI Emerging Markets Index in the trailing 12-month period.

Ironically enough though, one benefit of portfolios with exposure to emerging markets is a measure of risk reduction. Because emerging markets are not as integrated with other global stock markets, events in Brazil, for example, may help offset events in the United States, evening out a portfolio's overall vulnerability.

Then again, the one-day 9% drop in Shanghai this past March, which precipitated a global market selloff, proves the contrary.

This all points to the long-standing fact that the flip side of enjoying exceptional returns is running the risk of exceptional volatility.

Year-to-date (as of 20 April), the MSCI's Emerging Markets benchmark index is up 6.9%, just slightly higher than the 6.1% gain in the MSCI All-Country World Index.

Forecasts are good. According to the Adviser Fund Index, GEMS are expected to be top performers over the next three years. Credit Suisse has also raised its global equity ratings, with emerging markets raised to 30% overweight from 15 % overweight.

Mah Ching Cheng of fundsupermart.comadds that emerging market fundamentals still remain sound given that current price to earnings ratios. For emerging markets including Asia, the P/E stands at 13.8X for the financial year 2007; Earnings growth is at 17.8% and 11.8% for 2007 and 2008.

The biggest risk factor for emerging markets says Mah, is that some large emerging markets such as Russia and Brazil are quite dependent on demand for oil and commodities. They may be affected by the volatile price movements of natural resources. Another risk factor is the slowdown in the U.S. economy, which usually translates into a slowdown in consumption. That has a knock on effect on export-oriented countries in Asia.

The Fund

Schroders is offering a unique approach to GEMS with its ISF Global Emerging Market Opportunities. Schroders’ approach here is based on a number of principles:

- Investing in the best six countries

- Investing in the best-rated stocks

- Flexibility to diversify into bonds (max 30%)

- Flexibility to preserve capital with cash (max 30%)

Instead of benchmarking the fund to indexes like MSCI Emerging Markets, the Gross TR Index or the JP Morgan EMBI Global Diversified Index, Schroders picks the best stocks (and bonds) from its six best-rated stocks using its own country model. This frees it from the constraints of having to invest in big MSCI-benchmarked countries like South Korea, Taiwan or China.

Rather, Schroders reassess the six countries every month and the model is adjusted accordingly. The top six are chosen based on these factors:

- Valuation

- Growth

- Currency/Risk

- Momentum

- Interest Rates

Argentina, Brazil, Hungary, South Korea, Russia and Turkey were the six country picks as of 27 March 2007.

Apart from the top six countries, the fund also picks only the best-rated stocks. This includes the top-rated picks from the non-top countries.

Schroders says the model has returned over 27% per annum since 1989, and outperformed the MSCI Emerging Markets by 15.7% p.a. The fund has a target of 15% returns over three-year rolling periods.

The Affair

The feature that differentiates Schroder’s ISF Global Emerging Market Opportunities fund from other GEM funds is that it is not benchmarked to an index.

Fundsupermart.com’s Mah thinks the advantage of this approach is that it narrows down the scope to only markets that meet Schroders’ framework criteria. These criteria may include good valuations or strong earnings growth. In this case, it concentrates the stock picking effort on markets that already seem healthy fundamentally.

Funds who simply follow benchmarks may have to actually invest in a number of markets even though the fundamentals in these markets may not seem attractive as they are confined to the benchmark. If benchmarked funds do not like certain markets they can only underweight the markets by a certain designated percentage, for example 5% (as stipulated in their objective).

However, Mah points out that investors should look closely at the criteria Schroders uses, which should be broad-based and complete, not overly focused on just value or growth. If the process were overly focused on growth or value, than the overall portfolio of stocks would tend to be less diversified.

Please send your questions and comments to us at fundaffair@cnbc.com. We will answer as many of your emails as possible on "CNBC's Cash Flow" airing on Monday, April 23, 10 a.m. to 12 noon Hong Kong/Singapore time.