Do you think that it is obsolete or discriminatory for a banker to want to know whether a prospective mortgage will be backed by a home in an economically declining neighborhood?

Do you think that favoring applicants with well developed credit histories over those without is, likewise, a sign of discrimination?

When examining the income statement which accompanies a mortgage application, is it wrong to take into account whether that income comes from a welfare check instead of paycheck?

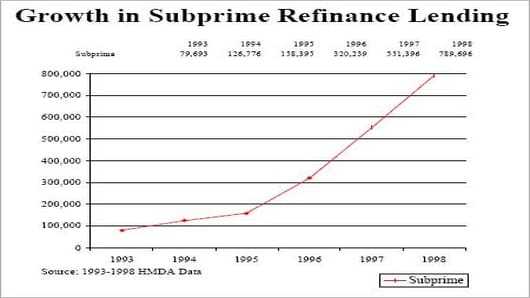

Most of you will answer "no" to these questions. Banks certainly did for many decades. The problem is that the federal regulators answer yes. Case in point, a document published by the New York and Boston Fed, called, Closing the Gap,which is aimed at apprising bank managers and board members of their legal obligation to increase minority home lending.

One section in particular warns banks about their "arbitrary," "biased" and "obsolete" lending practices which interfere with minority lending. The regulators attack traditional lending standards such as: looking at monthly budget obligation ratios, requiring borrowers to pay their own down payments, requiring a credit history, analyzing neighborhood trends, and favoring income based on a steady paycheck (as opposed to welfare, unemployment, alimony, etc.).

Here are some examples (italics mine):

Obligation Ratios: Special consideration could be given to applicants with relatively high obligation ratios who have demonstrated an ability to cover high housing expenses in the past. Many lower–income households are accustomed to allocating a large percentage of their income toward rent…

Down Payment and Closing Costs: Accumulating enough savings to cover the various costs associated with a mortgage loan is often a significant barrier to homeownership by lower–income applicants. Lenders may wish to allow gifts, grants, or loans from relatives, nonprofit organizations, or municipal agencies to cover part of these costs…

Credit History: Policies regarding applicants with no credit history or problem credit history should be reviewed. Lack of credit history should not be seen as a negative factor. Certain cultures encourage people to “pay as you go” and avoid debt…

Property Appraisal/Neighborhood Analysis: Terms like “desirable area,” “homogeneous neighborhood,” and “remaining economic life” are highly subjective and allow room for racial bias and bias against urban areas. The same holds true when lenders evaluate properties based on their market appeal or compatibility with the rest of the neighborhood…

Sources of Income: In addition to primary employment income, Fannie Mae and Freddie Mac will accept the following as valid income sources: overtime and part–time work, second jobs (including seasonal work), retirement and Social Security income, alimony, child support, Veterans Administration (VA) benefits, welfare payments, and unemployment benefits.