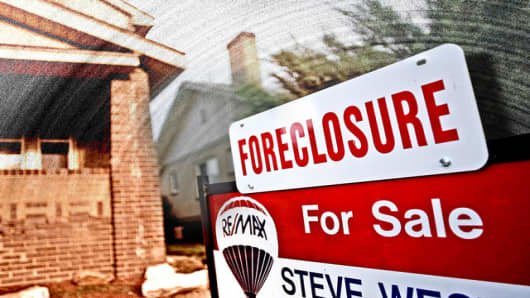

Kathy Lovelace lost her job and was about to lose her house, too. But then she made a seemingly simple request of the bank: Show me the original mortgage paperwork.

And just like that, the foreclosure proceedings came to a standstill.

Lovelace and other homeowners around the country are managing to stave off foreclosure by employing a strategy that goes to the heart of the whole nationwide mess.

During the real estate frenzy of the past decade, mortgages were sold and resold, bundled into securities and peddled to investors. In many cases, the original note signed by the homeowner was lost, stored away in a distant warehouse or destroyed.

Persuading a judge to compel production of hard-to-find or nonexistent documents can, at the very least, delay foreclosure, buying the homeowner some time and turning up the pressure on the lender to renegotiate the mortgage.

"I'm going to hang on for dear life until they can prove to me it belongs to them," said Lovelace, a 50-year-old divorced mother who owns a $200,000 home in Zephyrhills, near Tampa. "I'll try everything I can because it's all I have left."