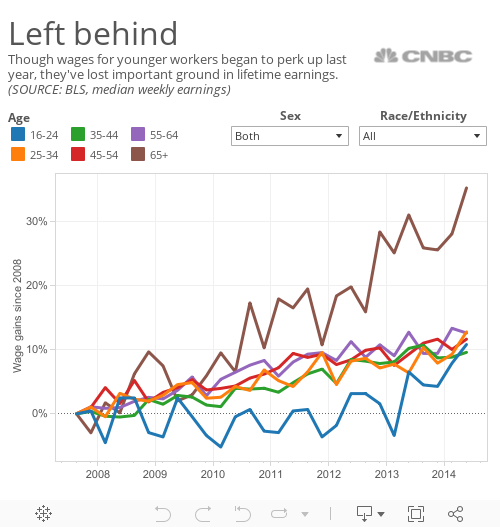

After years of frustrating job searches and low-wage work, millions of millennials are finally catching a break.

But despite recent data pointing to an improved job market and a pickup in wages, this generation of younger workers will feel the economic impact for the rest of their lifetimes. That's the conclusion of a series of economic studies, showing that lost wages early in a career can reduce overall earnings for a lifetime.

The latest study comes from the researchers at the New York Federal Reserve, who crunched more than 200 million pieces of earnings data from 1978 to 2010. What they found was that younger workers who enter the workforce in lower-wage jobs will have a hard time catching up later in their careers.

"Across the board, the bulk of earnings growth happens during the first decade," according to New York Fed economists Fatih Guvenen, Fatih Karahan, Serdar Ozkan, and Jae Song.

Read MoreLow-wage jobs crowding out fatter paychecks

That's largely because as your income rises, your raises typically get smaller. And because you're less likely to find another job that pays substantially more as you get older, you're more likely to stick with the job you have, even if your income rises slowly, the researchers concluded.

"As the attractiveness of job offers decline with the current wage, more job offers will be rejected, and therefore the frequency of job-to-job transitions will also decline with age, implying that most wage changes will be small (within-job) changes," they wrote.

That's not good news for the millions of millennials who entered the workforce during the Great Recession and in its aftermath got off to a slow start up the income ladder.

From 2007 until the pace of hiring picked up last year, the jobless rates for millennials topped other age groups, even among those with freshly earned college and advanced degrees. Many were forced to start their careers in lower-wage jobs, slowing their income progress and dampening their lifetime earnings.