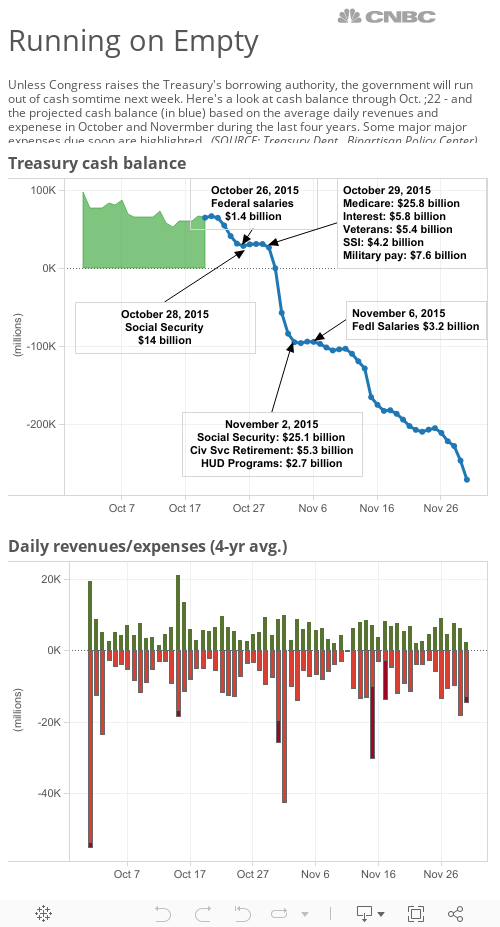

The exact date when the Treasury will have to start bouncing checks is difficult to predict. With some 80 million payments moving through the system each month, the government's revenues and expenses ebb and flow with irregular, sometimes unpredictable, peaks and troughs on the income and payment sides of the ledger. Social Security checks typically go out at the beginning of the month, for example. Quarterly tax receipts, on the other hand, typically cluster around the middle of the month.

But the Treasury is rapidly exhausting its remaining cash. Because Congress authorizes more spending than it mandates in taxes, the Treasury has to borrow the difference. But — unlike every other developed country in the world — U.S. law puts a cap on the department's borrowing authority, which has to be raised as debt reaches that new level. (The debt ceiling has nothing to do with limiting spending; that can only be done when Congress approves the federal budget.)

Since March, when the Treasury hit the current borrowing limit of $18.1 trillion, it's been juggling revenues against expenses to keep the government afloat. But as of last Wednesday, the latest data available, the government had a cash balance of less than $70 billion.

If daily revenues and expenses came in at the average pace of the past four years, the Treasury would run out of money even earlier than the Nov. 3 target. But to head off the looming man-made crisis, Treasury officials have been deploying a series of "extraordinary measures" — the governmental equivalent of looking for quarters and dimes underneath the couch cushions.

Those tactics involve holding off on reinvesting cash in several government investment funds, including those used to back civil service retirement plans or intervene in currency markets when the value of the dollar becomes volatile. But even with those measures, the Treasury is running out of time.