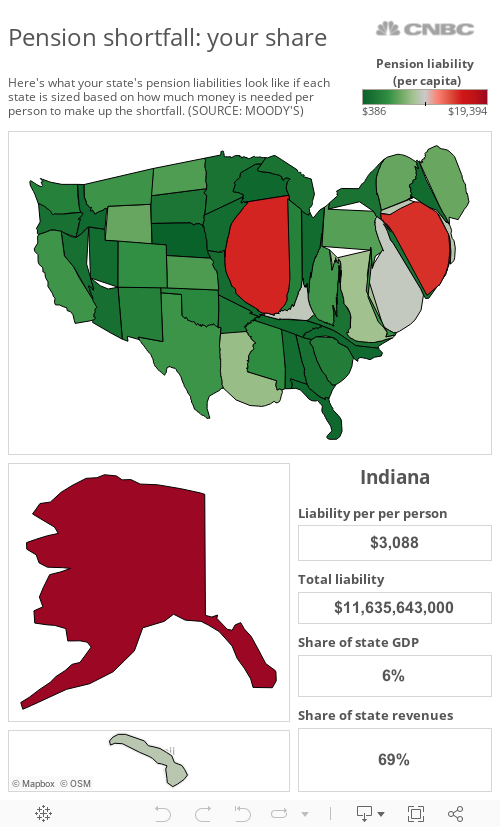

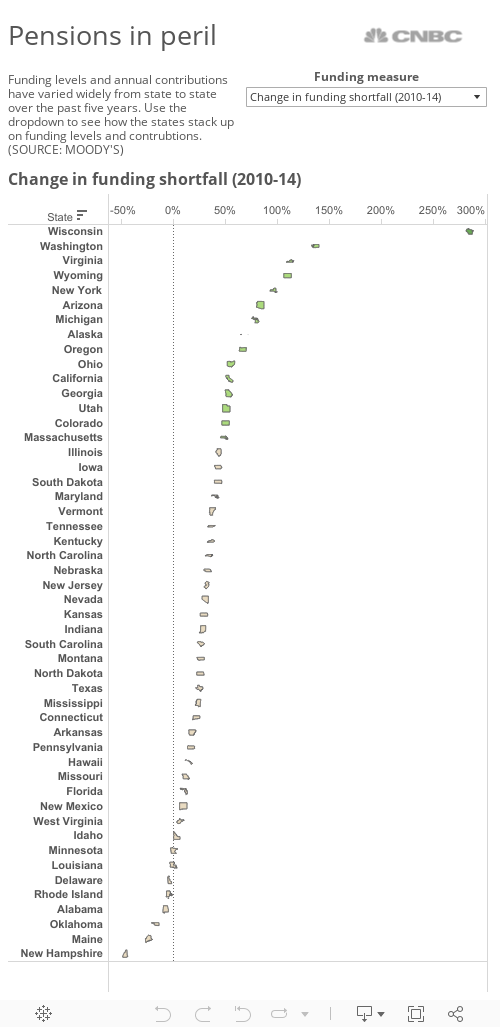

Despite the ongoing economic recovery, state governments are still struggling to keep up with the payments to their pension funds needed to take care of current and future retirees.

And the shortfalls vary widely from one state to another, according to the latest data from Moody's, which assigns credit ratings for state governments.

In Nebraska, for example, the pension liability amounts to about $386 per person, the lowest in the nation. That compares with Alaska ($19,394 per person: the highest in the country), Illinois ($15,158 per person) and Connecticut ($14,769). The average pension shortfall in 2014 amounted to $4,383.

One way to show how your state's pension shortfall is to resize the states on a map based on their pension liability instead of their land area. When sized that way, here's what state pension liabilities look like.