There may be good reasons to overhaul parts of the sweeping Dodd-Frank financial reforms, enacted in 2010 in response to the financial crisis two years earlier.

But concern about a slowdown in bank lending isn't one of them.

President Donald Trump and congressional Republicans have vowed to roll back a wide range of federal regulations — with Dodd-Frank one their top priority targets.

On Friday, Trump ordered the Treasury Department and other financial regulators to review the banking and consumer finance rules created under Dodd-Frank, a law he has called "a disaster."

"We expect to be cutting a lot out of Dodd-Frank," he told a group of bankers and other corporate executives, "because, frankly, I have so many people, friends of mine that have nice businesses that can't borrow money. They just can't get any money because the banks just won't let them borrow because of the rules and regulations in Dodd-Frank."

Trump's order did not specify which regulations he would like to see lifted, a move that will require congressional legislation. But defenders of the law have noted that the Trump administration could choose to relax enforcement of portions of the law it deems too restrictive.

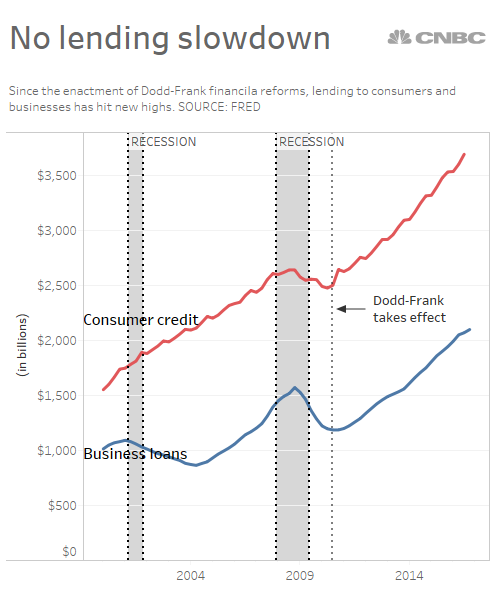

Opponents of the law argue, among other criticisms, that it has clamped down too hard on banks and restricted the availability of credit for businesses and consumers.

"The Dodd-Frank Act is a disastrous policy that's hindering our markets, reducing the availability of credit, and crippling our economy's ability to grow and create jobs," Sean Spicer, Trump's press secretary, said Friday.

But statistics on bank lending don't back up that claim. Since the law took effect in July 2010, bank lending to businesses and consumers has continued to hit new highs.