President Donald Trump on Tuesday repeated his campaign pledge to undertake a major overhaul of bank regulations, arguing that lending restrictions are hampering job growth.

Tighter lending conditions often throw cold water on job growth. A closer look at the data, however, shows that neither of those things is happening in the U.S.

Trump made his remarks following a White House meeting with a group of business executives, noting that his administration is working on giving a "major haircut" to the 2010 Dodd-Frank Wall Street Reform and Consumer Protection Act.

The sweeping measure was enacted following the financial collapse of 2008 that sparked the deepest global recession since the 1930s.

"The banks got so restricted," Trump told the executives Tuesday. "We want strong regulation, but not regulations that make it impossible for banks to lend money to people that are going to create jobs."

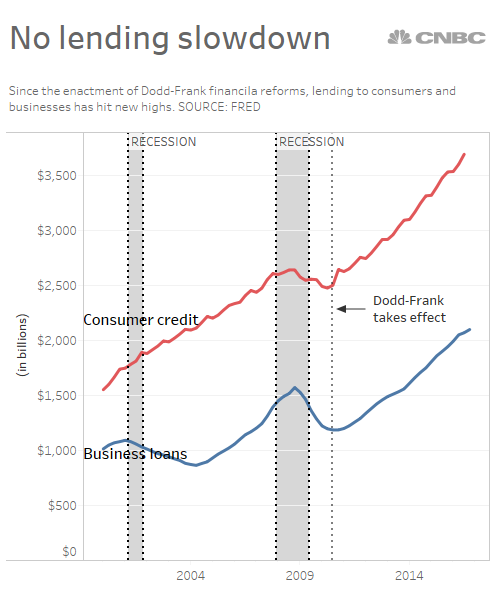

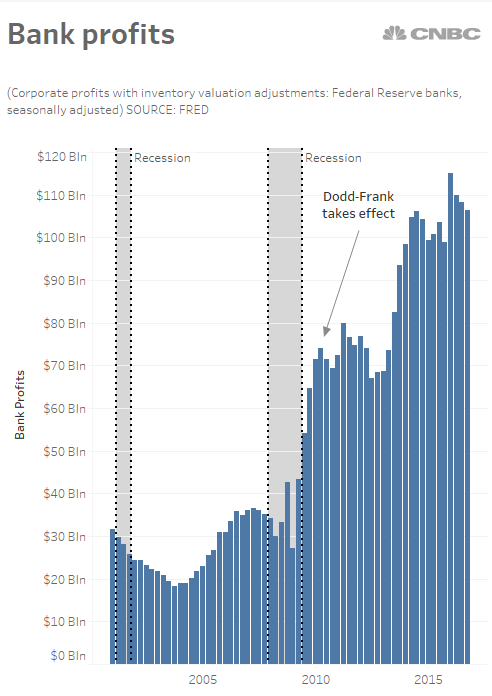

While there may be good reasons to overhaul parts of the sweeping law, concern about a slowdown in bank lending isn't one of them.

Since the law took effect in July 2010, bank lending to businesses and consumers has continued to hit new highs.

Continued strong lending comes as the economy continues to produce hundreds of thousands of new jobs every month, driving the jobless rate below 5 percent.