Add China to the list of countries grappling with the threat of deflation.

Fresh data on Friday from the Chinese National Bureau of Statistics showed that consumer prices rose just 2 percent last year, well below the government's target of 3.5 percent.

Prices of commodities and raw materials at the producer level, meanwhile, were 3.3 percent lower than a year earlier, the 34th consecutive monthly decline and the biggest drop since September 2012.

Oil-consuming countries around the world are seeing inflation fall as the price of crude oil has crashed since last July. By itself, that lowers energy bills and should help boost spending and economic growth.

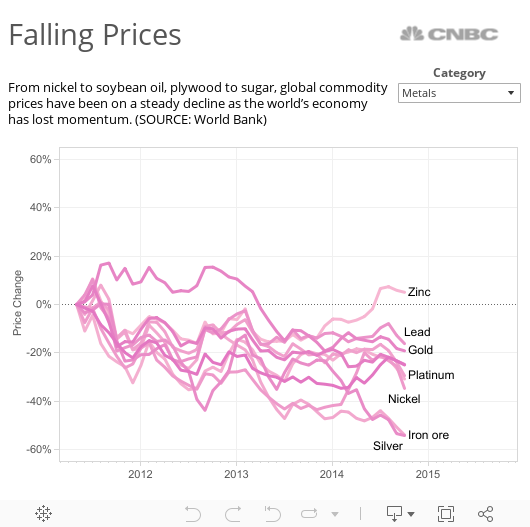

But the global price drop is hitting a wide range of commodities and raw materials, from plywood to sugar. In Europe's slow-moving economy, prices overall shifted into reverse last month—down two-tenths of a percent in December—touching off worries that a prolonged period of falling prices could take hold, dragging economic growth along with it.

Read MoreEuro zone deflation fears may be overblown

So far, that doesn't appear to be happening—in Europe or China. Despite the plunge in oil prices, the costs of other consumer goods are rising, though slower than government officials would like.

While China's economy is still growing at a rate that would represent a boom in the developed world, the pace has slowed since it undertook a massive stimulus of borrowing and building after the global financial crisis of 2008.