However, a fourth theory also merits consideration: leadership has taken the country in a new direction, and this is dampening China's growth. From Deng Xiaoping until the current Xi administration, China has been ruled by an economically liberal philosophy emphasizing economic growth, global integration, and harmonious relations with other countries. With the Xi administration, however, the social compact has become conservative. Nationalism, not economic liberalism, now seems the driver of policy decisions.

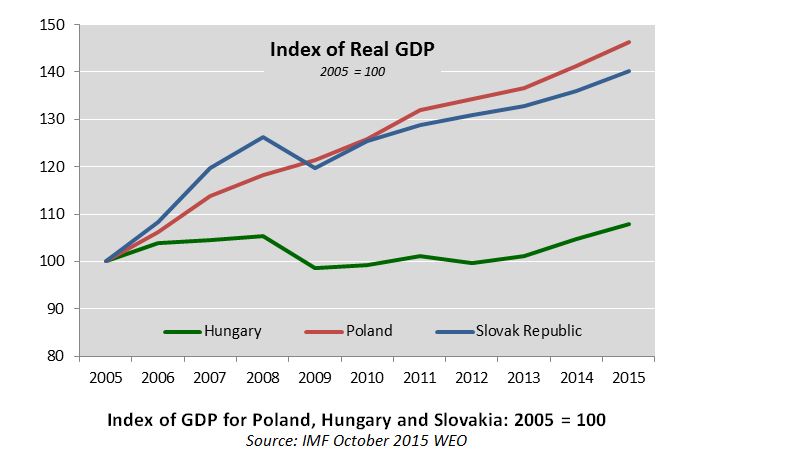

Other post-communist nations have taken this path already. In Hungary, for example, the Orbán government has repeatedly thumbed its nose at European norms, nationalizing pensions, reducing the independence of the judiciary, decreasing fiscal transparency, and restricting media rights. It has proved popular, with Orbán's FIDESZ party winning a qualified majority in Hungary's 2014 parliamentary elections.

But nationalism comes at a price. Hungary's GDP is barely above its 2005 level, even as those of Poland and Slovakia have soared. From 2005 to 2015, Hungary's GDP growth averaged 0.8 percent, versus 3.4 percent for Slovakia and 3.9 percent for Poland. Not all of this is due to the Orbán regime, which took power in 2010. But the Orbán government has exacerbated a turn inward which had started in the early 2000s. As such, Orbán is both a cause and effect of rising Hungarian nationalism. The resulting policies have knocked nearly 3 percentage points from Hungary's GDP growth annually.