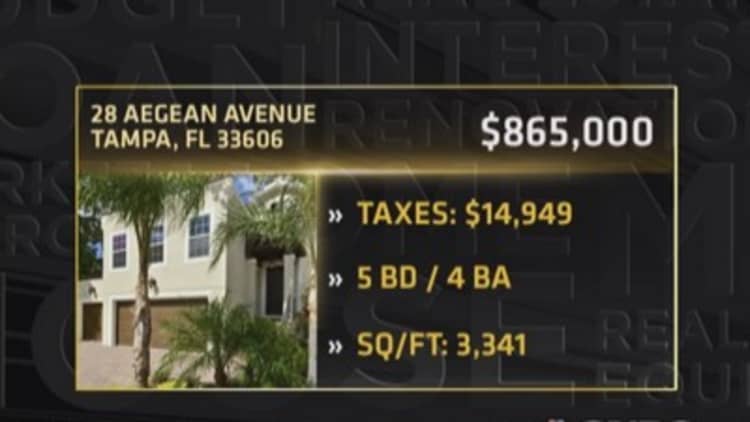

The Tampa, Florida, housing market was one of the hardest hit by the housing crash. As with much of Florida, a steep run-up in prices, fueled by investor-flippers during the loose lending days of the housing boom, led Tampa to a catastrophic crash and one of the nation's highest foreclosure rates. As the state's recovery progresses, Tampa is still seeing some weakness but is finally beginning to return to a normal market pace.

"We had huge investor activity from Wall Street in 2013, but that has slowed down," said John Lum, a developer and real estate broker in the Tampa area. "Job creation is strong. We've been very steady."

Sales of single-family homes in August were flat from a year ago, according to the Greater Tampa Association of Realtors. Sales of condominiums, however, were down over 11 percent. Some of the weakness can be blamed on a lack of supply of homes for sale. The overall Tampa market shows a 3.9 month supply, down from 5.1 months a year ago.

Home prices in Tampa are still rising at a fast clip, up 9 percent in June from a year ago, according to the latest reading from the S&P/Case Shiller Home Price Index.

Read MoreThe good and bad of Portland's rising home prices

Tampa still suffers the remnants of the past; it has the seventh highest foreclosure rate in the nation, according to RealtyTrac. One in every 407 housing units is in some stage of foreclosure. Florida is still weeding through thousands of bad loans, as the state's judicial process has been slow but finally gaining steam.

Unlike Miami, Fort Lauderdale and Orlando, Tampa on Florida's west coast is not getting as much attention from international buyers. That may be behind the big drop in condo sales, but supply is also a factor.

Read MoreCharlotte seeing its homes sell quickly

"There hasn't been any new condo construction in a long time," Lum said. "What is left is tired, used product."

—By CNBC's Diana Olick.