When it comes to the recent improvement in state finances, one retiree's pain is another one's gain.

More than five years after the Great Recession tore a giant hole in their budgets, most states have made big progress in stabilizing their finances.

That's good news for millions of state taxpayers and the millions of investors who hold state-issued municipal bonds—many of whom are retirees that depend on them for a steady stream of safe income.

But the improved fiscal health owes much to a wave of cuts that have whittled away at pension benefits for current and future retirees.

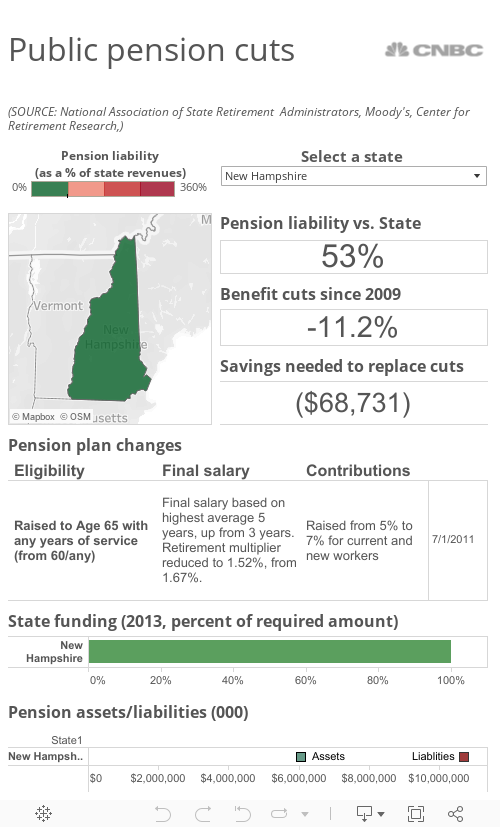

"Nearly every state since 2009 enacted substantive reform to their retirement programs—including increased eligibility requirements, increased employee contributions reducing benefits, including suspending or limiting cost-of-living increases," said Alex Brown, research manager at the National Association of State Retirement Administrators.

More than 45 states have wielded the budget knife on pension benefits, deploying a variety of these changes and resulting in overall benefit cuts averaging 7.5 percent, according to an analysis by the NASRA. That also means new employees can expect to work longer and will need to save more on their own to match the benefits paid to existing employees and current retirees.

Pressure to cut public pension benefits rose sharply in 2007, when the global economy collapsed under the weight of a massive credit bubble, and states fromMaine to Hawaii were hit by the fiscal storm of a lifetime. Surging unemployment cut deeply into income and sales taxes. Collapsing property values undermined a once reliable tax base.

Read MoreIf Detroit cuts pensions, will your city be next?

When the dust settled, state officials were left with multibillion-dollar budget gaps that had to be filled. Since the recession, states have closed some $425 billion in budget shortfalls, according to the Center on Budget and Policy Priorities, a research institute.

This week the Center for Retirement Research at Boston College reported that the health of public pensions nationwide improved last year for the first time since the Great Recession and is expected to keep improving. The study found that state-administered public pension funds now have assets amounting to about 74 percent of what they need to meet the promises they've made to current and future retirees, up from 72 percent in 2012. The researchers project those funding levels will rise to as much as 80.5 percent by 2018.

That improved fiscal outlook has helped states get better credit ratings and borrow new money more cheaply. That, in turn, has helped millions of investors who rely on municipal bond income—many of whom are retirees themselves.