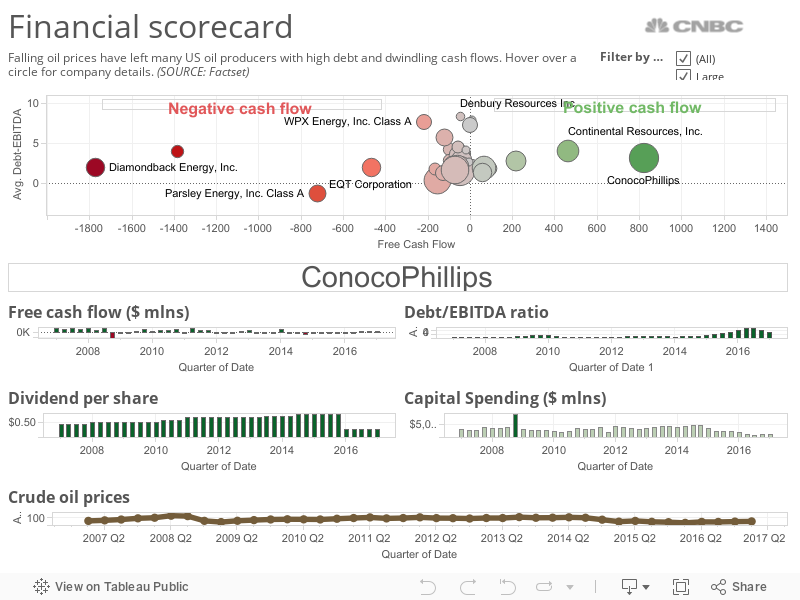

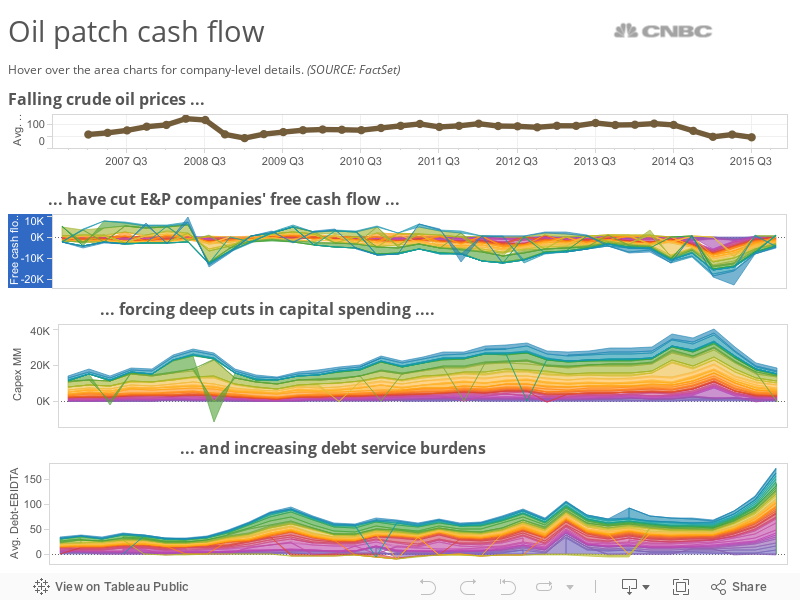

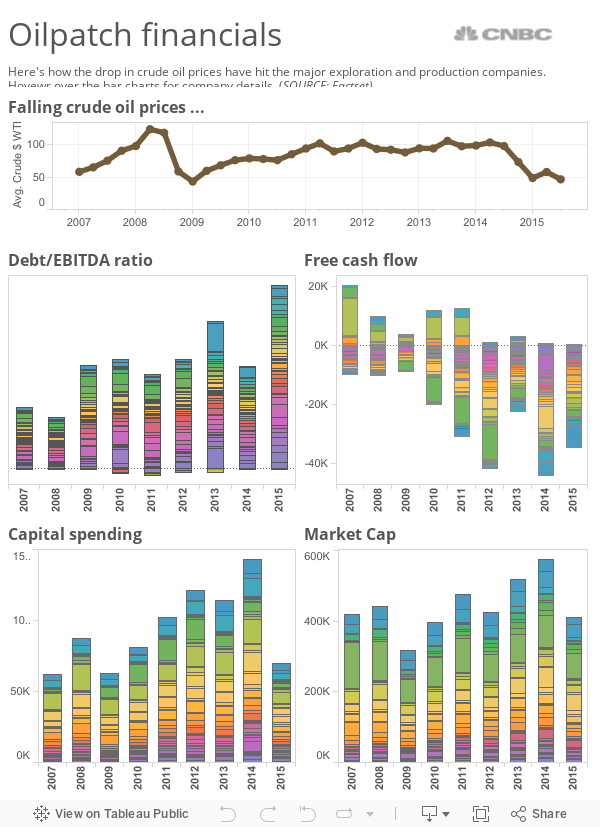

U.S. drillers have mostly weathered OPEC's year-old policy of nonstop pumping in an oversupplied market. But it's left balance sheets battered.

In the last year, publicly traded independent oil and gas companies have seen free cash flow plummet and debt levels rise, necessitating deep cuts to capital spending.

Read MoreHow US drillers weathered OPEC's new oil order

For years, U.S. drillers have spent more than they've earned from operations, leaving them reliant on external financing such as debt and equity offerings and asset sales. As recently as last year, some saw that situation beginning to reverse for top producers.

But as the chart below shows, that scenario has not played out.