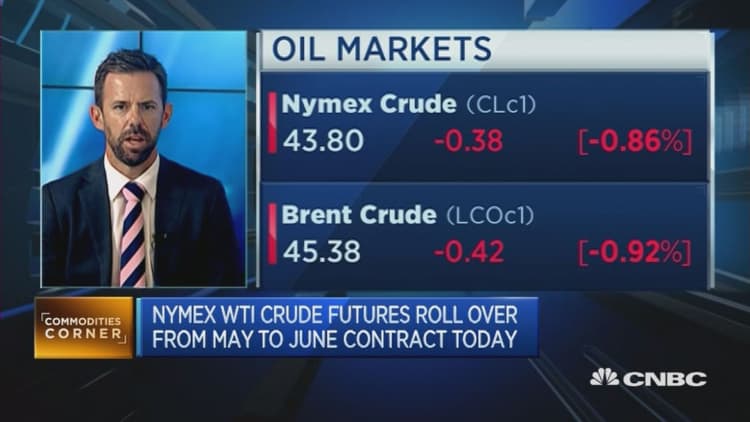

U.S. oil prices slid on Thursday, reversing early gains as a rebounding dollar weighed on commodities denominated in the U.S. currency.

Prices were already lower when market intelligence firm Genscape reported a build of more than 840,000 barrels in U.S. crude in the four days to April 19 at the Cushing, Oklahoma delivery point, traders who saw the data said.

The Genscape data further weighed on sentiment. Market players already were concerned that this month's 14-percent rally could coax U.S. shale crude producers to raise output.

Benchmark Brent crude futures fell $1.16 to $44.64 a barrel, off its session high of $46.18.

U.S. crude futures settled $1 lower, or 2.3 percent, at $43.18, having risen as high as $44.49.

Prices rose early, then retreated after the dollar index rebounded, making crude and other commodities denominated in the greenback more expensive to holders of currencies like the euro.

The 1.6-percent plunge in the Philadelphia Fed Index, which showed stress on the manufacturing sector, also weighed on crude prices, said John Kilduff, partner at Again Capital.

Despite Thursday's slide, Brent and WTI are up about 70 percent from multi-year lows hit between January and February. The rally came despite builds in U.S. crude inventory and failure by major oil producing countries to agree to an output freeze to fight the global supply glut.

"If you were to take the fundamental pieces of the puzzle, they really don't compare with the latest two days of pickup in prices," said Harry Tchilinguirian, global head of commodity strategy at BNP Paribas.

"Should we really be at $43 on a WTI basis? Because the closer we get to $45 mark with a curve that is in contango in the case of WTI, the more you're going to throw a lifeline to US shale producers."

Oil rose in early trade after the International Energy Agency (IEA) said non-OPEC production would fall this year by the most in a generation.

IEA chief Fatih Birol said low oil prices had cut investment about 40 percent over the past two years, with sharp falls in the United States, Canada, Latin America and Russia.

But Russia's energy minister said the country might push oil production to historic highs, while Iran reiterated its intention to boost output to 4 million barrels per day, and Saudi Arabia threatened to flood markets with more crude.

Libya could also rapidly ramp up oil production, the head of Libya National Oil Corporation (NOC) told an oil summit in Paris.

Also on Thursday, OPEC's secretary general said the oil market will begin rebalancing by the third quarter of this year and will turn positive by 2017 despite world's top producers failing to reach an agreement to freeze production during a weekend meeting in Doha.

"Doha or no Doha, we see that the market is turning," Abdullah El-Badri told an oil summit in Paris.

El-Badri also said he expects OPEC members to discuss an output freeze at a previously scheduled June meeting, Dow Jones reported.

— CNBC's Tom DiChristopher contributed to this story.