Stock are rallying as investors appear to be putting fears about a Brexit behind them, but strategists say too much uncertainty remains to sound the all-clear.

"The idea that Britain can economically remain in the EU is growing and contributing to improved sentiment," said Adam Button, currency analyst at ForexLive.com. "That sentiment is hope-based rather than evidence-based."

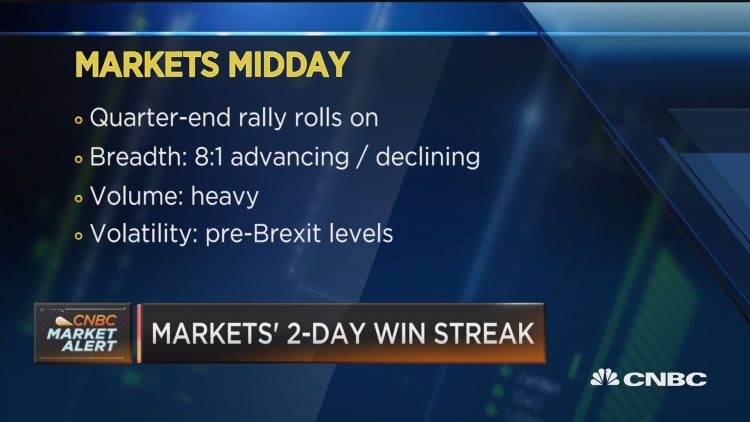

On Wednesday, stocks extended Tuesday's gains to recover more than half their Brexit losses in intraday trade. The CBOE Volatility Index (VIX), considered the best gauge of fear in the market, had its largest one-day percentage drop Tuesday since 2011 and was trading below pre-Brexit levels Wednesday.

The fell 5.3 percent Friday and Monday, on worries that a Brexit would hurt the world economy and possibly lead to the departure of other European countries from the EU. But those worst-case fears faded, and stocks reversed course — even the British FTSE erased all of its post-Brexit losses.

The pound steadied and began to rise after its 13 percent plunge, and the dollar index gave back much of its post-Brexit surge to trade flat on the month Wednesday.

"Markets are able to shrug off European 'tough talk' because nothing happens till (the British) pull the trigger and start the process. It is clear that they are in no hurry whatsoever, thus, Brexit is in suspended animation and thus not a market factor," Art Cashin, director of NYSE floor operations for UBS, said in an email.

Britain voted last Thursday to leave the European Union, triggering a roughly $3 trillion market cap loss in global markets over Friday and Monday.

The EU exit process can't start until the never-used Article 50 is invoked. While leaders of the bloc have urged for quicker move toward officially starting the process, the U.K. has pushed off triggering Article 50. British Prime Minister David Cameron announced his resignation after remain won and left the official move to his successor, who will likely be announced by early September.

That political stalemate has given rise to some speculation that the U.K. will be able to negotiate more favorable terms than initially expected with the EU. There have also been fears that if the EU handles the separation poorly, it is more likely other countries would follow.

"Broadly the financial markets are not convinced you're going to see a disillusion of the euro area. If anything, more integration," said Karl Schamotta, director of FX research and strategy at Cambridge Global Payments. He also noted relative stability in oil prices throughout the initial Brexit shock as an indication of positive sentiment on global demand and growth.

To some, there's also near-term resolution of another major fear after the Brexit vote. Over the weekend, Spain's populist Podemos party gained less ground than expected in the country's parliamentary election, dampening some concerns that a growing global wave of populism would quickly increase pressure on the EU.

"We're not seeing the necessary majorities for launching further referenda in the EU membership by other member countries," said Max Kunkel, ultra high net worth investment strategist at UBS Wealth Management. He said with the Spanish election results, populist sentiment wasn't stopped "but it was limited versus some of the expectations we had."

On Friday after the Brexit vote, UBS Wealth Management lowered its euro/dollar forecast for the next three months to $1.08 from $1.10 and its three-month view on the pound/dollar to $1.32 from $1.46.

On Wednesday, the euro was little changed on the week, near $1.11 after falling below $1.10 to roughly three-month lows last week. The yen was near 102.9 after last week briefly dropping below 100 to its strongest against the dollar in nearly three years.

The edged off 30-year lows to trade near $1.34, but still about 10 percent below its recent peak of $1.50 late Thursday.

Athanasios Vamvakidis, head of G-10 FX strategy in Europe at Bank of America Merrill Lynch, attributed the gains in the pound and euro mostly to "temporary profit-taking and end-quarter flows."

"Markets may also be too optimistic that the U.K. may never activate Article 50. Although not a zero probability, it is very low in our view," he said in an email. "The U.K. economy will have to deteriorate too fast by too much, for the public opinion on the EU to change enough, to justify not activating Article 50. This is too many 'ifs.'"

In addition, the Treasury market may be one of the few markets calling the bluff on the optimism in stocks and currencies. In the last two days shorter-end Treasury yields have edged off recent lows, but the 10-year and 30-year yields are not far from their all-time lows.

"The fact that you've seen risk assets bounce and you haven't seen Treasury yields bounce is pretty noteworthy," said Eric Stein, co-director of global fixed income at Eaton Vance Management.

He also noted European bank stocks, which suffered much more than other risk assets, have not recovered as much. The STOXX Europe 600 banks index is still more than 14 percent lower over the last five days.

— CNBC's Patti Domm contributed to this report.