U.S. stocks closed at all-time highs Monday as Bank of America's quarterly results helped investor confidence going into earnings season.

The Dow Jones industrial average ended about 15 points higher, with Goldman Sachs and Home Depot contributing the most gains. The blue-chips index extended its winning streak to seven days, with a fifth straight day of record closes.

The S&P 500 also ended up about a quarter of a percent at a record high, led by information technology and consumer discretionary sectors.

Following Citigroup and JPMorgan Chase last week, Bank of America is now the third big U.S. financial institution to top second-quarter profit forecasts.

"It will be more positive surprises than negative ones, and my guess is that guidance will give people a sense that we're through the worst," said John Manley, chief equity strategist at Wells Fargo Funds, adding that the three-week equity rally is likely to "stick around" if earnings continue to surprise.

Second-quarter earnings kick into full gear this week.

Bank of America beat Street expectations on earnings and revenue Monday, with earnings per share of 36 cents versus an expected 33 cents, according to a consensus estimate from Thomson Reuters.

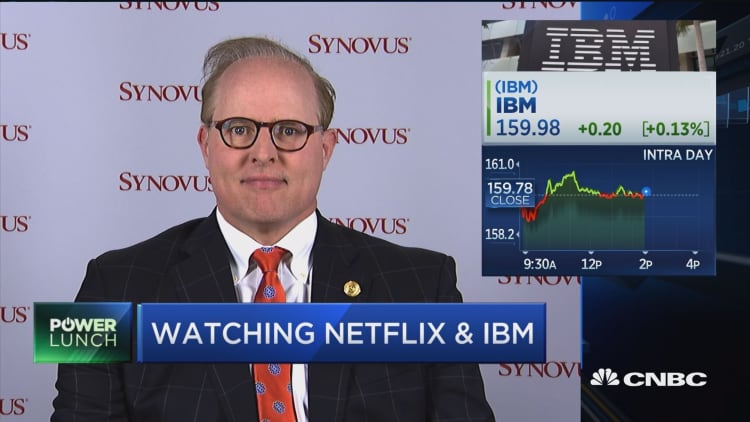

Hasbro also beat consensus estimates, and Netflix reported better-than-expected earnings after the bell, but subscriber numbers missed the company's own guidance. IBM beat analysts expectations with earnings per share of $2.95 versus consensus estimates of $2.89, according to Thomson Reuters.

"Earnings expectations were so low that there was no place else to go," said Bruce Bittles, chief investment strategist at R.W. Baird. Equity markets are likely to continue a rally as global monetary easing continues, he said.

"With record low interest rates, there's no competition for stocks," Bittles said. "The money has to go somewhere." The strongest sectors, he said, have been those with high dividend yields, like consumer staples and telecom.

The energy sector was the biggest drag on the S&P as rising crude stockpiles fueled investor fear that another glut could be building, Reuters reported.

In deal news, Japan's Softbank announced an all-cash offer for chip designer ARM. The acquisition marks the biggest takeover of a British company since June's Brexit vote.

"Coming into today's market with the M&A announcement helps the risk-on tone," said Quincy Krosby, market strategist at Prudential Financial. "That's a positive underpinning for the markets."

The Market Vectors Semiconductor ETF closed 2.9 percent higher after the deal, hitting an all-time high back to 2011. This was the ETF's eighth positive day in nine and its best day since May 20.

The pan-European STOXX 600 closed slightly higher, helped by Softbank's ARM acquisition. London-listed shares of ARM jumped more than 40 percent after the announcement Monday. The U.K.'s FTSE 100 was also helped by the deal, and closed at an 11-month high, according to Reuters.

On the data front, U.S. homebuilder sentiment fell 1 point in July, as foot traffic of potential buyers thinned and construction constraints continued, according to the monthly reading of builder confidence from the National Association of Home Builders.

Chinese home prices slowed for the second straight month in June, particularly in small cities, adding to fear that a construction-led economic rebound might not be sustainable, according to data from the National Bureau of Statistics in China.

In global news, Turkey expanded a crackdown on suspected supporters of the failed military coup against against Turkish President Recep Tayyip Erdogan. The number of people rounded up in the armed forces and judiciary is now roughly 6,000, Reuters reported.

The iShares MSCI Turkey ETF ended the day down by more than 6 percent, recovering some earlier losses. This was the ETF's worst day since June 24. Turkey's 10-year yield rose to 9.61 percent in afternoon trade, its highest level since June 27.

The U.S. dollar fell slightly against the Turkish lira and was mostly flat against a basket of currencies. The euro traded slightly higher against the dollar Monday, at $1.11 while the the dollar rose slightly against the yen, at 106.14 yen.

The British pound rose half a percent to $1.33 after Bank of England policy member Martin Weale said he was unsure about the need for an interest rate cut in August. The hawkish statement contradicts many of Weale's colleagues who said a rate cut is likely, citing expectations that the UK could slip into recession, Reuters reported.

In the U.S., tensions were high after three police officers were killed by a gunman in Baton Rouge Sunday. President Barack Obama condemned the killings, calling for a measured response ahead of party conventions.

The Republican National Convention begins in Cleveland Monday. Prudential's Krosby said the markets won't benefit from protests surrounding the event or anything "that breeds uncertainty".

"Markets want to see clear platform, and as much as possible a fairly united Republican party," she said.

U.S. sovereign bonds rose slightly Monday. Benchmark 10-year Treasury notes moved higher to yield 1.58 percent. Thirty-year bonds yielded 2.29 percent. Bond prices move inversely to yields.

Gold futures settled up 0.1 percent at $1329.30 per ounce after earlier falling to a session low of $1,323.70 per ounce.

U.S. crude futures settled down 71 cents to $45.24 per barrel after ending the previous session up 27 cents. Brent crude futures settled down 1.37 percent at $46.96 per barrel.

Major U.S. Indexes

The Dow Jones industrial average closed at a record high of 18,533.05, up 0.09 percent. DuPont and Home Depot led the gainers, while Travelers was the biggest laggard.

The closed at a new record of 2,166.89, up roughly a quarter of a percent. Information technology and consumer discretionary added the most gains, while energy and telecom led five sectors lower. Consumer staples hit a another new intraday all-time high Monday, but closed slightly negative.

The Nasdaq composite ended 0.52 percent higher for its highest close of the year of 5,055.78.

Advancers were slightly ahead of decliners on the New York Stock Exchange, with an exchange volume of 727.02 million and a composite volume of 2.94 billion.

The CBOE Volatility Index (VIX), widely considered the best gauge of fear in the market, traded near 12.44.

On tap this week:

*Planner subject to change.

Tuesday:

8:30 a.m. Housing Starts

Earnings before the bell:

Goldman Sachs, Johnson & Johnson, Novartis, Philip Morris, UnitedHealth, Comerica, LM Ericsson Telefon, Lockheed Martin, Prologis, Regions Fincl., TD Ameritrade, Wipro, WW Grainger

Earnings after the bell: ATB: Microsoft, Cintas, Discover Financial

Wednesday:

7 a.m. Mortgage Applications

10:30 a.m. Oil Inventories

Earnings before the bell: Abbott Labs, Halliburton, Morgan Stanley, SAP, Canadian Pacific Railway, Illinois Tool Works, M&T Bank, Northern Trust, St. Jude Medical, Imax

Earnings after the bell: American Express, eBay, Intel, Qualcomm, Core Labs, F5 Networks, Mattel, Newmont Mining, United Continental, Select Comfort, SLM (Sallie Mae)

Thursday:

8:30 a.m. Jobless Claims

8:30 a.m Philly Fed Business Outlook Survey

8:30 a.m Chicago Fed Nat'l Activity Index

9:00 a.m FHFA Home Price Index

10:00 a.m Existing Home Sales

10:00 a.m Leading Indicators

10:30 a.m. Natural Gas Inventories

4:30 p.m. Fed Balance Sheet

Earnings before the bell: Biogen, Daimler, General Motors, Roche Holdings, Travelers, Unilever, Union Pacific, Bank of NY Mellon, BB&T, Blackstone, Domino's Pizza, DR Horton, PulteGroup

Earnings after the bell: AT&T, Paypal, Schlumberger, Starbucks, Visa, Capital One, Chipotle Mexican Grill, E-Trade, Advanced Micro, Boston Beer, Pandora Media

Friday:

9:45 PMI Mfg Index Flash

1:00 p.m. Oil Rig Count

Earnings before the bell: BTB: General Electric, Honeywell, American Airlines, Moody's, Stanley Black & Decker

More From CNBC.com: