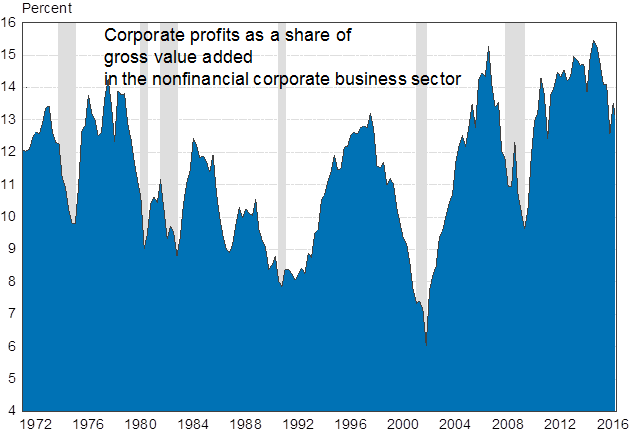

Source:Bureau of Economic Analysis. Shaded areas are periods of recessions.

But let's take a step back first. How did corporate profitability perform so strongly in the first five years after the financial crisis, despite the mediocre growth recovery? Part of the answer lies in a period of remarkable cost-cutting that began in the late 1990s and continued through the Great Recession, which saw U.S. workers replaced with technology (productivity growth) or less expensive labor located in emerging countries (offshoring). Likewise, there is growing evidence that increased industry concentration in many U.S. sectors drove rising profitability over the past decade.

Two additional factors contributed to the high profitability rates of U.S. corporations during the post-crisis years. First, as a result of high unemployment, wage growth was historically low between 2009 and 2015. Second, interest rates have also remained historically low ever since the Great Recession, thus reducing the cost of financing. Corporate profits soared from the confluence of all these forces.

But periods of very high profitability tend not to last very long, and it seems that U.S. corporate profits peaked in the second half of 2014, and are now on a downward trend. Some of the trends that contributed to high profits earlier have reversed themselves in recent years. Offshoring activity has declined substantially from the previous decade, productivity growth has been anemic in the last six years, and tighter labor markets are beginning to accelerate wages. On top of that, the appreciation of the U.S. dollar lowers profits generated in other countries.

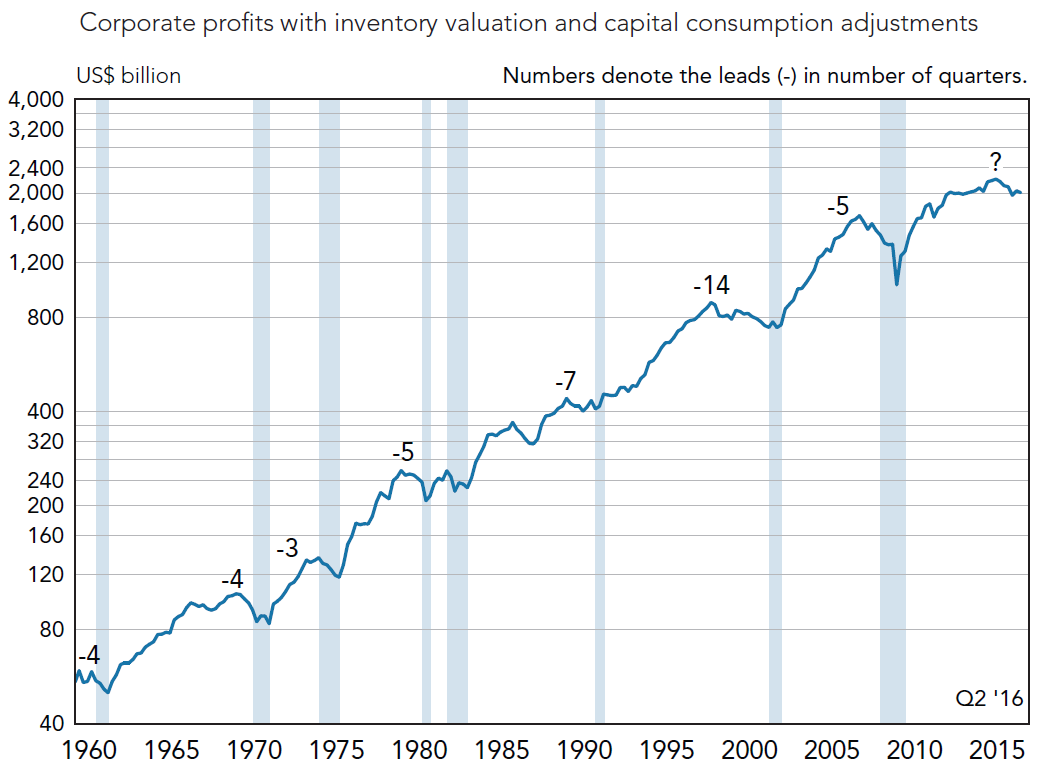

The recent decline in profits has raised the alarm about the possibility of a recession. In almost every expansion since 1959, a recession followed less than two years after a peak in corporate profits (chart 2). We are now about two years removed from the 2014 peak. Is a recession therefore imminent?

Chart 2