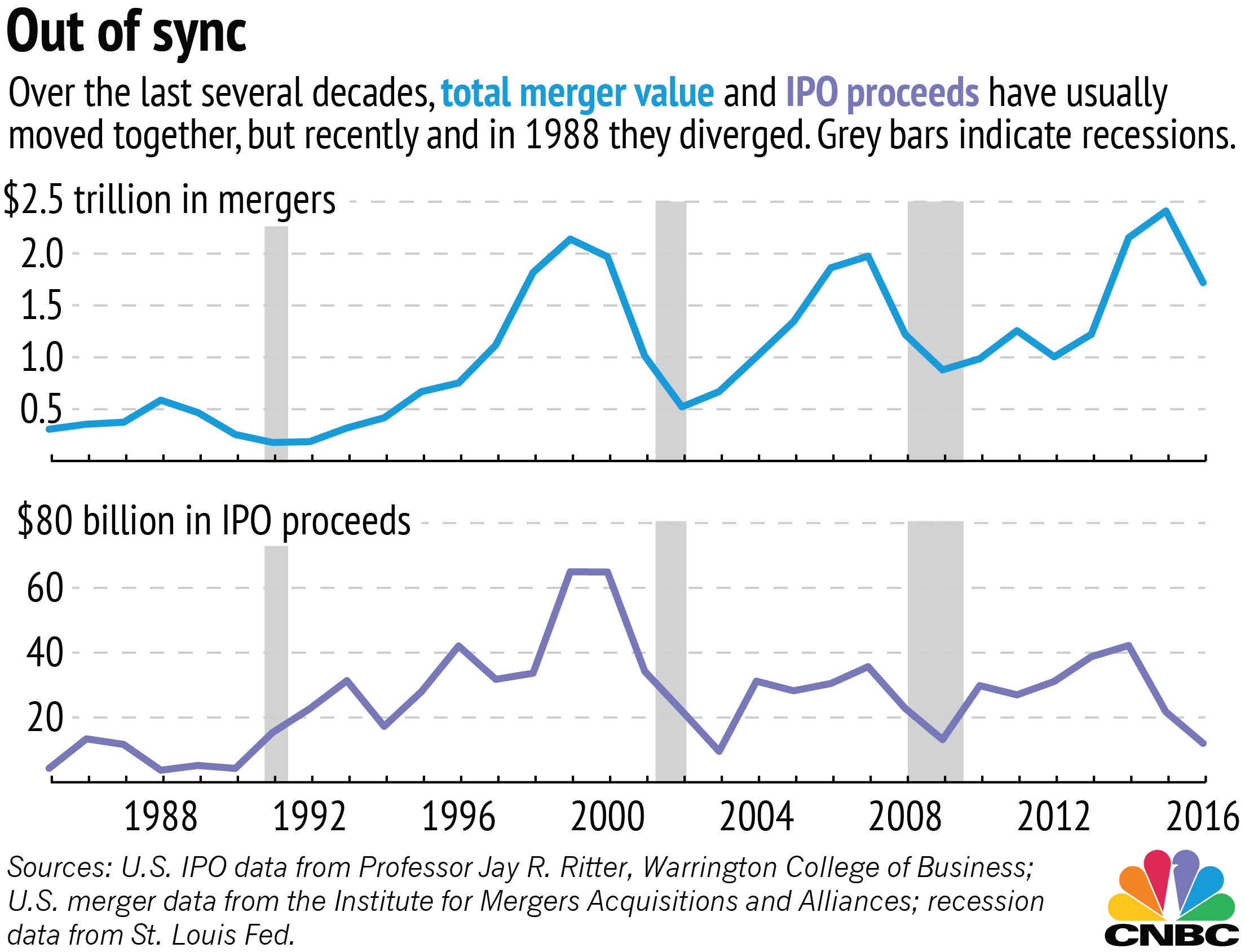

The long-term decline of the IPO is far more obvious in the number of offerings. Over the last 15 years, we've seen an average of 108 offerings annually (excluding REITs, mutual funds and other entities that can also have IPOs but aren't operating companies). In comparison, we saw almost 350 offerings each year on average in the 1980s and 1990s.

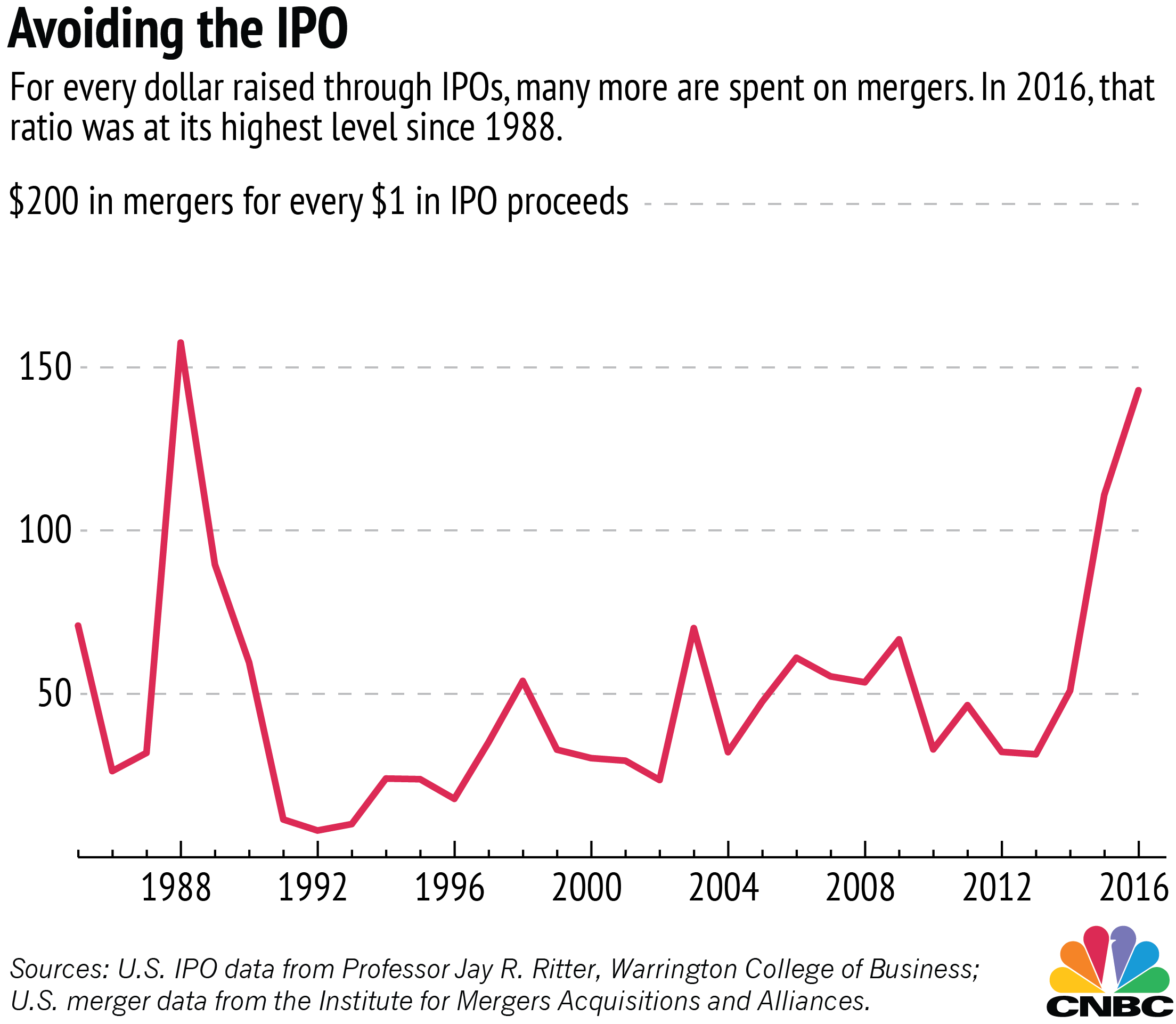

Of course, individual companies have their own reasons for making the decisions they do, but is there any explanation for why companies have turned away from IPOs recently while mergers have flourished? Some observers have been quick to blame onerous regulation, like the Sarbanes-Oxley Act of 2002. But there have also been changes in the market that have made selling out a safer choice than going public for many companies, said professor Jay Ritter, an IPO expert at the University of Florida.

"There has been a worldwide trend going on for a couple of decades where for many industries, especially technology, getting big fast is more important than it used to be," said Ritter. "Going public and growing organically just takes too long, and it's typically not the profit-maximizing strategy."

Globalization and technology have made it harder to be a small company competing against giant conglomerates. In recent years, small companies have become less profitable and offered poor returns for investors after IPOs, according to a 2013 paper co-written by Ritter in the Journal of Financial and Quantitative Analysis.

A small tech company can become profitable quickly by taking advantage of the brand name and infrastructure offered by a massive buyer like Oracle, and small pharmaceutical companies with successful drug trials can easily cash in by accepting a bid from big pharmaceutical companies. With a market hostile to small companies and potential courters flush with cheap money, it's not surprising many smaller private companies have leaned toward mergers instead of IPOs.

Last year was also a particularly bad year for bigger companies like Airbnb or Uber to launch IPOs because no company wanted to have the wind taken out of its sails by a contentious election or Brexit debacle. Those companies that held off last year figured they could boost IPO figures this year, an analyst told CNBC. Ritter agrees that 2017 might have a slight rebound, but it won't be anywhere close to the good old days.

"Unless the market takes a fall, I think there will be more IPOs in 2017, but by the standard of the 1980s and '90s, it will be a very modest number in line with the last 16 years," he said. "In particular, small tech companies have stopped going public, and I don't expect that they ever will again."