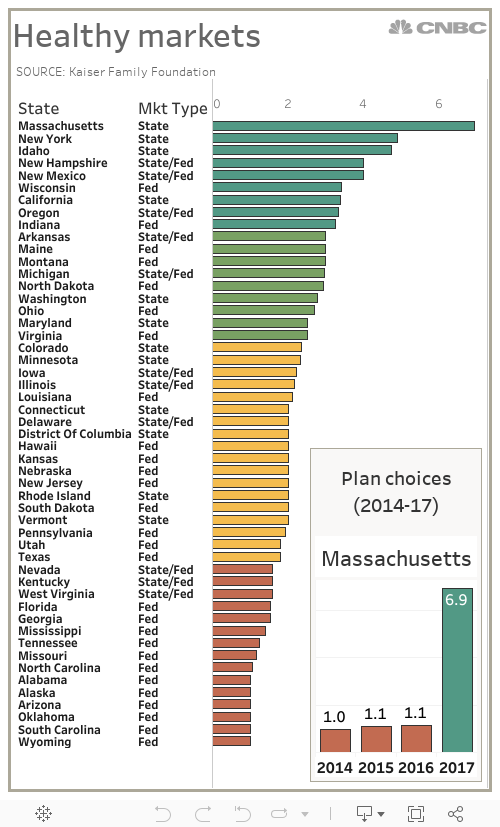

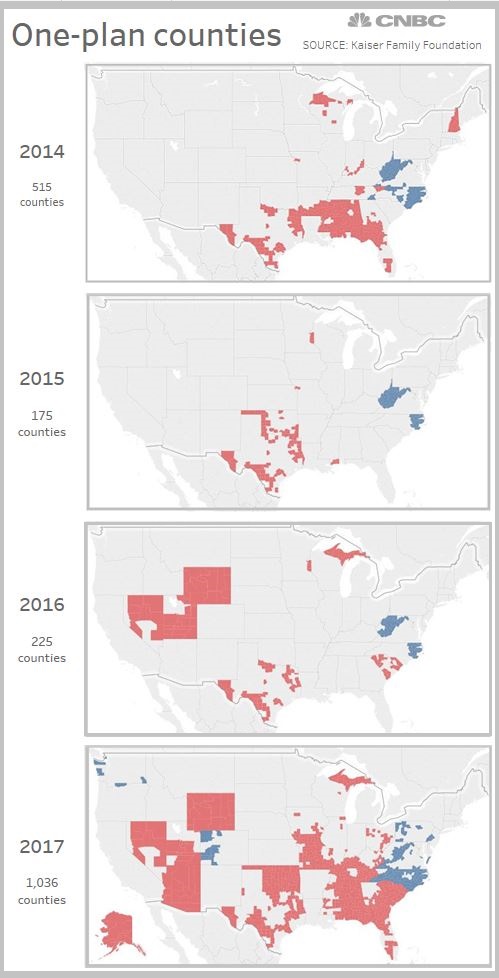

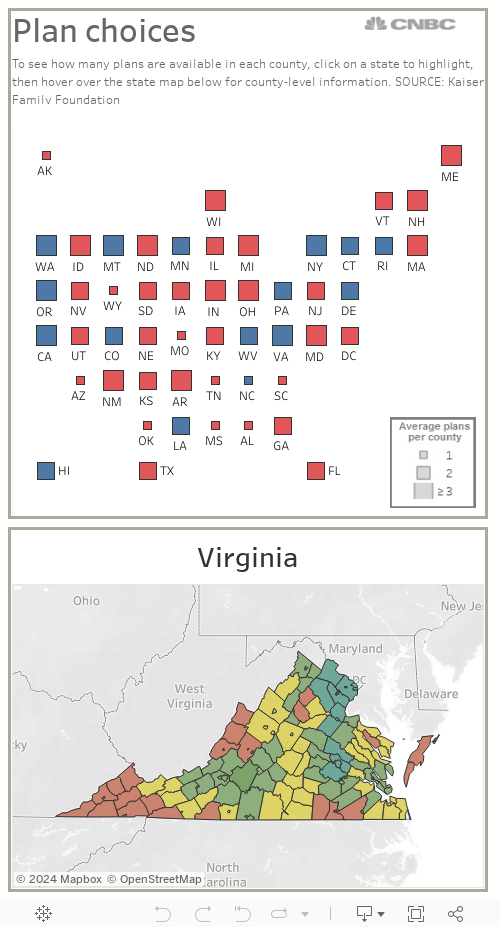

More than three years after the rollout of state and federally run insurance marketplaces, the program is finally stabilizing and insurers are seeing their profits grow, according to a Kaiser Family Foundation report last week.

A major reason for the improved health of Obamacare, the report said, was an increase in premiums approved this year to compensate for a larger-than-expected share of sicker patients.

But more recent data indicate that those premium increases were a one-time market correction, according to the analysis. Slow growth in claims for medical expenses also played a role in insurers' financial improvements, the report said.

To be sure, the future health of the Obamacare depends heavily on whether the Trump administration decides to try to sabotage the program by withholding critical federal funding.

Trump has suggested several times that he could eliminate the so-called cost-sharing reduction subsidies, which help pay for consumers' out-of-pocket health-care expenses. The administration could cut those subsidies as early as next month.

"When those payments stop, (Obamacare) stops immediately," Trump said Wednesday. "It doesn't take two years, three years, one year. It stops immediately."

Like much of the White House rhetoric, the pronouncement is unrealistically dire.

Insurers have already been bracing for an end to those payments, by proposed premium hikes of more than 20 percent for next year to make up for the possible lost funding.

On Tuesday, major insurers called on Congress to intervene and protect the cost-sharing payments with a formal appropriation.

"Our members and all Americans need the certainty and security of knowing coverage will be available and affordable for them," said Justine Handelman, senior vice president in the Office of Policy and Representation at the Blue Cross Blue Shield Association, which represents insurers nationwide.

Even if those cost-sharing payments remain in place, the Trump administration has additional tools at its disposal to undermine the health insurance system.

Earlier this year, the administration backed off more strictly enforcing the so-called individual mandate, which is designed to lower the average premium cost by widening the pool of subscribers to include more younger, healthier people. The failed GOP reform plan would have allowed insurers to offer minimum coverage to those consumers, which would have further driven up costs for older people or patients with chronic conditions.