There are plenty of what ifs that could derail your travel plans. But does it necessarily follow that you need travel insurance?

Nervous travelers have had plenty of real-world examples this summer, from a power outage in the Outer Banks off North Carolina that forced the evacuation of an estimated 50,000 visitors and prevented the arrival of many more, to Tropical Storm Cindy, which affected travel in five states. Last week, the National Oceanic and Atmospheric Administration raised its tropical storm and hurricane forecast, noting this year could be "extremely active."

More travelers are opting in for coverage. Last year, 42.6 million travelers purchased more than 32.3 million travel insurance plans, according to the U.S. Travel Insurance Association. Those numbers are up 23.7 percent and 28.5 percent, respectively, from 2014.

But deciding whether you'd benefit from travel insurance isn't a quick "yea" or 'nay." Experts say it depends on several factors, including the cost and components of your trip, where you live and where you're headed, and what potential problems you're worried about (like that "extremely active" hurricane season).

"There's no simple answer, because everyone's trip is slightly different," Christopher Elliott, who advocates on behalf of travelers through his website, Elliott.org, told CNBC earlier this summer.

These four questions can help you weigh your options:

1) How much money is at stake?

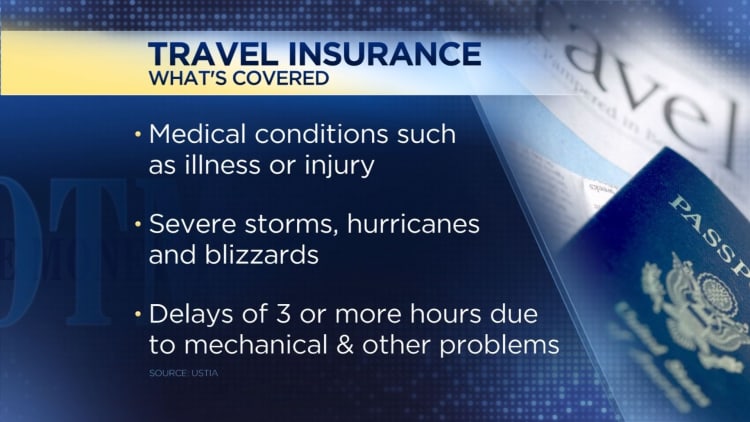

Check the change and cancellation policies for travel components including flights, hotels, cruises and car rentals, as well as any destination activities already purchased, such as theme park tickets. That can help you assess how much money might be lost if you need to cancel or postpone your trip, or head home early.

If that total is more than you're willing or able to lose, then travel insurance is worth a closer look, Loretta Worters, a vice president at the Insurance Information Institute, told CNBC earlier this summer.

2) What are your travel plans?

Big-ticket trips with intricate itineraries are often better contenders for insurance, Elliott said. (Think multicountry European vacation or a bucket-list African safari, versus a domestic getaway to grandma's.) A policy could help cover costs for situations such as the tour company going out of business, or a delayed flight that means you miss your cruise departure.

You might also want to consider travel insurance with medical coverage if you're headed abroad (where your health insurance may not be valid) or to a remote area or on a cruise (where getting to a hospital may require air evacuation), Worters said. Uncovered, those expenses could add up to tens of thousands of dollars.

3) What are you worried about?

Dig into the details to make sure a policy would offer the coverage you want. Broadly speaking, you have two choices: named exclusion (which covers a limited range of events and scenarios), and cancel-for-any-reason coverage (which, true to its name, offers broad coverage). The former generally runs 5 to 7 percent of the cost of your trip, and the latter, 8 to 10 percent, Elliott said.

"Named exclusion is a little more risky," he said, with big variations in what's covered and when.

Say you're worried about hurricane season, which runs from June 1 through Nov. 30. One policy might allow you to cancel your trip as soon as there's an official storm warning in effect for your destination, while another may require a bigger impact like a delayed flight, Steven Benna, a spokesman for comparison site Squaremouth, told CNBC earlier this summer. You won't be covered at all if the storm threatening your trip is named before you buy a policy.

Keep in mind that unless you get a cancel-for-any-reason policy, fear of travel — say, because you're worried about recent terrorist attacks or that you might contract a disease such as Zika at your destination — typically isn't covered.

4) Do you already have coverage?

Before you buy a third-party travel insurance policy, check to see if you already have some protections through other sources. For example, a homeowners or renters insurance policy may cover your belongings away from home, said Worters — helping alleviate worries about theft or lost baggage.

Travel insurance is also a common perk for credit cards, provided you paid for those travel arrangements with the card. (Again, you'll want to scrutinize details carefully.) On the most generous cards, you might have coverage of up to $10,000 per trip, according to a recent Squaremouth analysis.

That might mean you don't need a policy at all, or only need one that fills in gaps — say, to add medical coverage and cover any trip costs that exceed the cap, said Benna. That stacking can help you create a more comprehensive policy at a lower cost, he said.

If you're a frequent traveler, insurance coverage might also be something you look for the next time you're hunting for a new card, Jill Gonzalez, an analyst at WalletHub.com, told CNBC earlier this summer. A recent analysis from the site found that one-third of credit cards offer trip cancellation insurance, with an average $3,200 in coverage. Nearly 40 percent offer lost luggage insurance, and a quarter offer delayed luggage insurance.

"These benefits are probably not top of mind," she said — but they could save you hundreds of dollars.

"On the Money" airs on CNBC Saturdays at 5:30 a.m. ET, or check listings for air times in local markets.