The Fed is about to make history Wednesday, and so far, the market has yawned.

Some strategists say that creates the opportunity for a sudden wake up call and a rush of volatility when the Fed releases its statement at 2 p.m. Fed Chair Janet Yellen briefs the media at 2:30 p.m. ET.

Chances are that the market continues to have a muted response, but some bond pros say the announcement could also jolt the markets one way or other, depending on the Fed's tone and its forecast for interest rates

The Federal Open Market Committee is expected to announce Wednesday afternoon that it will start to reverse quantitative easing, the massive bond buying program it initiated during the financial crisis to save the economy. Now with $4.5 trillion in assets on its balance sheet, the Fed is taking the step of moving away from the final stages of that program, which has been to replenish those bonds as they mature.

"It really is peculiar. You have the Fed doing this, you don't even know in the next couple of months, you have a chance for a fairly decent change in tax policy…The bigger story is there's no market reaction to much of anything lately," said Michael Schumacher, director of rate strategy at Wells Fargo.

He said if the Fed announcement goes as expected, yields could first move lower for a week or two and then rise, based on the past reaction to Fed interest rate hikes.

"It's a first, and you can tell I'm hedging because the Fed has never done this," he said. "Longer term, it really opens Pandora's box. The Fed has never done anything like this. Really no big central bank has done this."

The Fed plans to shrink its balance sheet in a slow and steady process. Even though quantitative easing, or QE, ended long ago, the Fed has been keeping liquidity high with its purchases to replace maturing securities. The Fed plans to slow down those purchases to replace bonds and mortgage securities at an initial pace of $10 billion a month, increasing it by that same amount each quarter until it reaches a total of $50 billion.

"It is, at least in our assessment, a little surprising the market has not really responded more to the expectations for overall balance sheet reduction," said Mark Cabana, head of U.S. short rate strategy at Bank of America Merrill Lynch. "While the total amounts will start small, they're going to increase pretty quickly. Next year we're going to have $230 billion that comes off the Treasury portfolio and $150 billion that comes off the mortgage portfolio… By the end of 2021, you're looking at a cumulative impact of $1.4 trillion. The market should be efficient and be pricing it in already."

While banks and central banks will buy some of the Treasurys and mortgages that the Fed is stepping away from, private investors will also need to step up to buy more. That growing supply in the market could have some impact on rates, pressuring them higher.

"I'm at least of the view that the total cumulative impact of this supply should have an impact on rates markets, raise longer term rates and steepen the curve. The market does not really seem to be too concerned about this," Cabana said.

BlackRock's Rick Rieder, the global chief investment officer of fixed income, said the $10 billion initial step is "a drop in the bucket" but the impact of the program will change a year from now when the Fed's balance sheet reduction is much larger and that could help send yields higher. But rates won't go too high because of global demand for bonds.

"I think we're going to be in a low rate environment for a long time," he said, noting that global central banks are still providing heavy accommodation, and U.S. yields look attractive compared to Japan and Europe. The European Central Bank is talking about paring back its bond buying, but it still will be buying securities.

"We're in an unbelievable conundrum," he said. Rieder said real rates are extremely low given where they should be, based on the economic growth around the world. He said longer dated Treasurys are responding more to the easing policies of the Bank of Japan or ECB in some ways than they are to the Fed.

"There's not enough bonds in the world at an attractive level," Rieder said.

The Fed has indicated it would separate the balance sheet announcement from other policy moves, so it is not expected to raise interest rates Wednesday. But rates at its December meeting. Also in play is whether the Fed changes its long-term interest rate forecast.

As for stocks, strategists say if the Fed surprises by sounding hawkish, that would be a negative for a stock market near record highs. But Art Hogan, the chief market strategist at Wunderlich Securities, said the stock market may also not want to see the Fed lower its interest rate forecast for future years, in a dovish stance.

"That's not a positive…We want them to sound slow and steady," said Hogan, adding cutting back the rate forecast would mean too little economic growth on the horizon. But he did say if the Fed sounds too hawkish about a December hike, now in its forecast, that could also send stocks lower. While the market expects more than a 50 percent chance for a December hike, Hogan said there is some expectation in the stock market that the temporary damage to the economy from Hurricanes Irma and Harvey could

Nomura's head rate strategist George Goncalves also says the market is not pricing in the Fed balance sheet operation.

"It all depends on how they characterize things," Goncalves said. "They want to do it to take away liquidity. Don't make it sound like it's not a big deal. It is a big deal. They have a large balance sheet because of QE which was meant to get the economy going, get inflation going. They ended up instead with asset inflation."

He said if the bond market rallies, meaning yields move lower, "The market would be thinking we are making a policy mistake," he said.

Goncalves said if the Fed downplays the program exit too much, it's possible the strategy could back fire and send investors into the bond market, driving rates higher instead. Bond prices move opposite yields. If the Fed announces the balance sheet reduction and also lowers the forecast for future interest rate hikes, included in a chart it calls the "dot plot," that would sound dovish.

"If there's very little changes in their forecast and the balance sheet gets started, we should view that as the Fed is committed to the tightening process," said Goncalves. Rates could then move higher.

"By the Fed normalizing policy and draining liquidity, if that's happening at a time when tax policies are changing that could really be a watershed moment," said Goncalves. "At a minimum, a healthy backup in rates by the Fed normalizing policy and draining liquidity would just be a validation that market understands it and this is a form of tightening."

How the market will move after the Fed unveils its plans to shrink the balance sheet is also up for interpretation.

Schumacher said it could mean higher yield in the 5-year duration, since the Fed has made more purchases in that area.

Cabana said if the Fed were to cut its interest rate forecasts, that would signal a more accommodating Fed and the yield curve could steepen, or the spread between long term yields and short would expand.

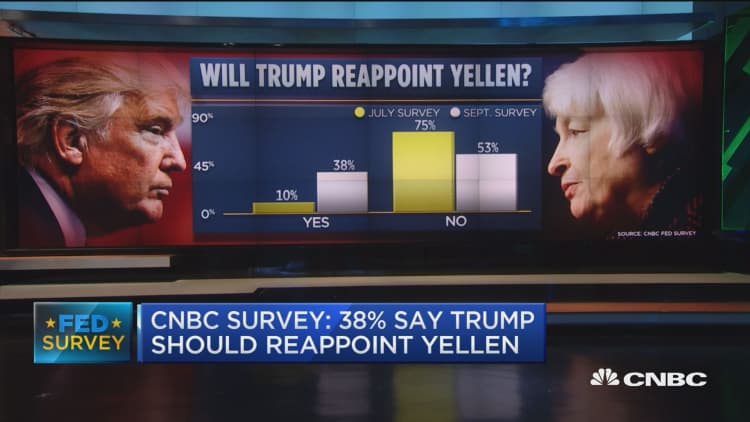

WATCH: Fed survey shows 38 percent believe Trump should reappoint Yellen