Banks, credit card issuers and other financial companies will be able to block customers from banding together to sue over disputes, after the U.S. Senate on Tuesday narrowly killed a rule banning the firms from using "forced arbitration" clauses.

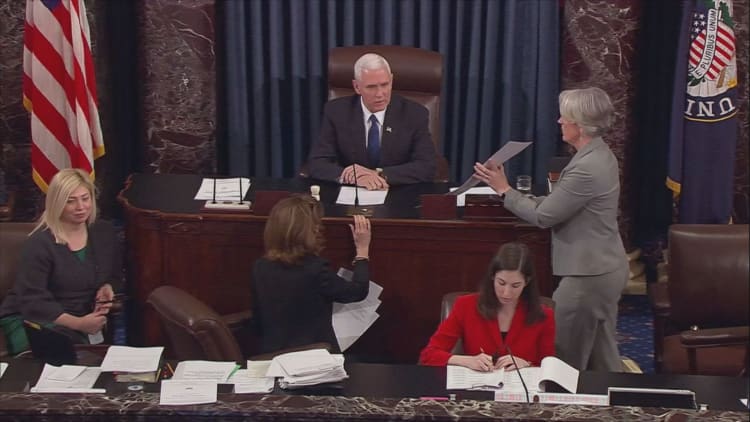

Republican Vice President Mike Pence appeared on the Senate floor at 10:11 p.m. EDT (0211 GMT) to cast the tie-breaking vote as the chamber's president and approve the most significant roll-back of Obama-era financial policy since President Donald Trump took office vowing to loosen the leash on Wall Street. The final count was 51 to 50.

The Republican-dominated House of Representatives has already passed the resolution repealing the Consumer Financial Protection Bureau (CFPB) rule released in July. The resolution also bars regulators from instituting a similar ban in the future.

After a signature from Trump, expected soon, the resolution will abruptly end a years-long fight that has included multiple federal regulators, consumer advocacy groups, and financial lobbyists.

CFPB Director Richard Cordray, a Democrat appointed by former President Barack Obama, rarely comments on congressional action but on Tuesday night said, "Wall Street won and ordinary people lost."

"This vote means the courtroom doors will remain closed for groups of people seeking justice and relief when they are wronged by a company," he added.

Customers must agree to the clauses as a condition of opening accounts, saying they will take any disputes to closed-door arbitration instead of joining class-action lawsuits, where complainants band together to share litigation costs. The clauses are used for nearly every U.S. consumer product and service since the Supreme Court ruled them legal in 2011.

Victims of the Equifax hack were outraged last month when the company included forced arbitration fine print in offering them free credit monitoring. The company later removed the clauses.

At the same time, Wells Fargo customers whose identities were used in last year's phony accounts scandal have had difficulty sueing the bank because they are bound by arbitration clauses in contracts they signed for legitimate accounts. The CFPB rule, set to go into effect next spring, was not retroactive and would not have helped Equifax or Wells customers.

Members of Trump's administration have relentlessly assailed the regulation, and on Monday the Treasury Department laid out arguments against it in a special report.

Acting Comptroller of the Currency Keith Norieka said on Tuesday the Senate's action stopped a rule "that would have likely increased the cost of credit for hardworking Americans and made it more difficult for small community banks to resolve differences with their customers."

Meanwhile, major bank lobbying groups who sued last month to block the rule cheered the resolution's passage.

One of the groups, the U.S. Chamber of Commerce, said Congress had reined in the "overgrown and unaccountable" CFPB, an independent agency created to protect individuals' finances that conservatives say consistently reaches beyond its authority in its rulemaking.

Critics of the rule had said class actions only benefit trial lawyers and arbitration generally wins larger settlement awards for customers. Supporters said forced arbitration harms customers by putting companies in control of the process and taking away the right to sue enshrined in the U.S. Constitution.

The CFPB created its rule after conducting a five-year study that found customers struggle to have banks open arbitration cases about their complaints, but that those few cases have led to slightly higher individual awards than class actions.

"The Senate today prevented a cash grab that would have transferred wealth from consumers to the pockets of wealthy attorneys," said Ted Frank, director of the center for class-action fairness at the free-market group Competitive Enterprise Institute.

Ohio Senator Sherrod Brown, the most senior Democrat on the Banking Committee, meanwhile, said Tuesday's vote "will make the rich richer, and the powerful more powerful."

Watch: Sen. Van Hollen to Wells Fargo CEO Tim Sloan: Don't you understand why class action suits make sense?