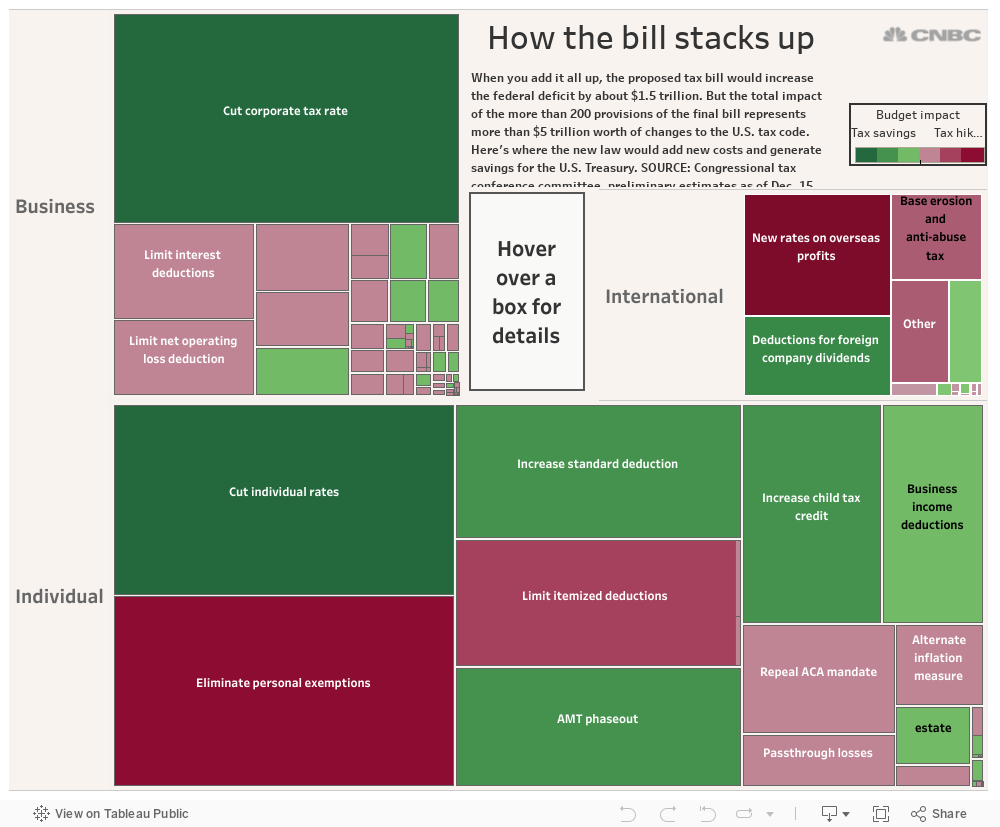

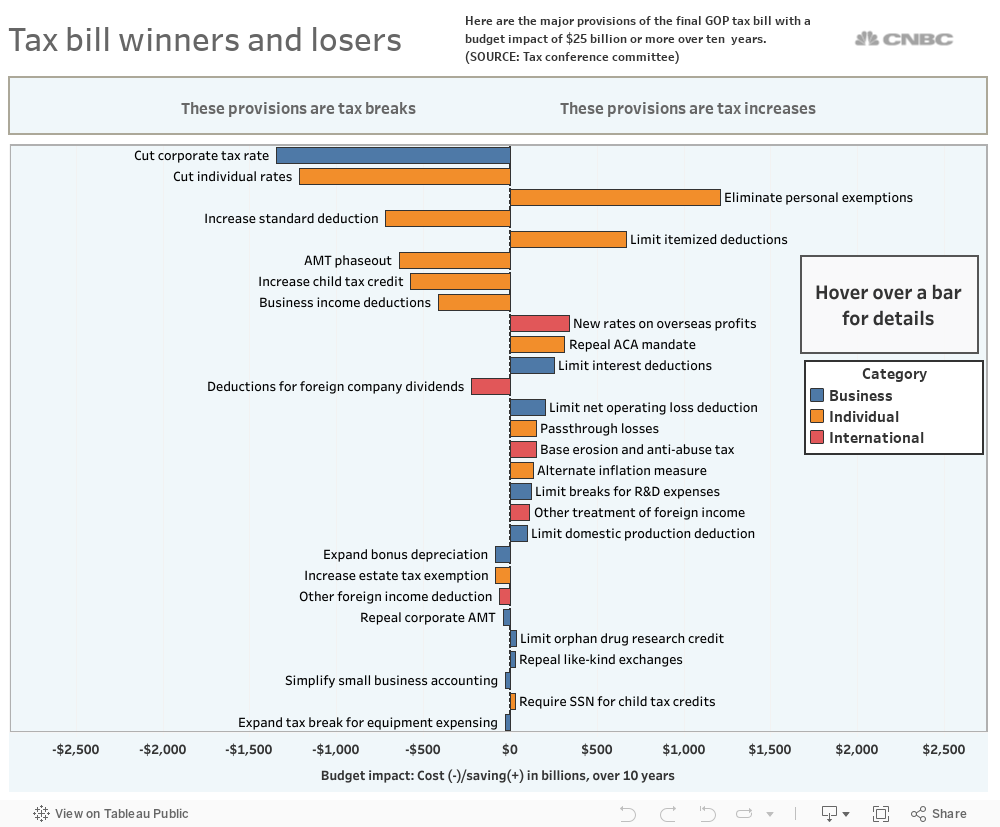

It's being billed as a $1.5 trillion package. But when you add it all up, the changes in the proposed tax overhaul bill set for a vote this week in Congress would create more than $5 trillion worth of tax winners and losers.

Most of the original plan, months in the making but unveiled just weeks ago, has apparently survived intact. And despite some last minute arm-twisting and deal-making, the bill appears to have the votes in both the House and Senate to win approval.

Nicholas Kamm | AFP | Getty Images

President Donald Trump shows samples of the proposed new tax form at the White House in Washington, DC, on November 2, 2017.

Under the latest outline released Friday night, corporations would enjoy a big drop in the tax rate on their profits, but would give up dozens of deductions, exemptions and exclusions that lower their tax bill. Individuals would also see their tax rates lowered, but would give up some important tax breaks that benefit those at the bottom of the income ladder more than those higher up.

The changes won't go into effect until next year, so you won't really know for sure how much you'll save (or owe in new taxes) until the detailed rules are written and you prepare next year's tax return in early 2019. Even the Congressional tax wonks, tasked with forecasting the dollar impact of the bill's dozens of provision, warned in their spreadsheet that their estimates are "very preliminary."

But the broad outlines of the final bill are coming into focus. For individual taxpayers, the biggest savings would come from lower tax rates (worth $1.2 billion over 10 years), a doubling of the standard deduction (another $720 billion over 10 years), the phaseout of the alternative minimum tax (worth $637 billion in savings) and a bigger child tax credit ($573 billion).

In return for those tax breaks, individuals would give up personal exemptions (currently worth $1.2 billion in tax savings) along with popular deductions (worth $668 billion in savings.)

Businesses big and small also catch some new tax breaks and give up some popular deductions in return. The drop in the corporate tax rate from the current 35 percent to 21 percent will save U.S. companies more than $1.3 trillion over ten years. In return, they'll lose part of the deduction for interest expenses (generating $253 billion for the Treasury over 10 years), along with limits on deductions for operating losses ($201 billion) and R&D spending ($120 billion).

The bill's authors also hope to generate some new revenue for the Treasury by offering tax breaks on income earned by U.S. companies and stashed in overseas affiliates, but it remains to be seen how corporations will take to those provisions.

Employees would lose some popular tax breaks, including the deduction for moving expenses. Employers can no longer deduct the cost of helping workers defray transportation costs, and deductions for meals and entertainment expenses have been sharply cut. (Those two measures alone are worth more than $40 billion over ten years.)

The rest of the bill is a grab bag of deductions, exclusions, exemptions credits and other provisions, some of which will help or hurt only small groups of businesses or individuals.

Here's how the final bill stacks up.