House Republicans' update to last year's tax overhaul would open up new opportunities for older workers.

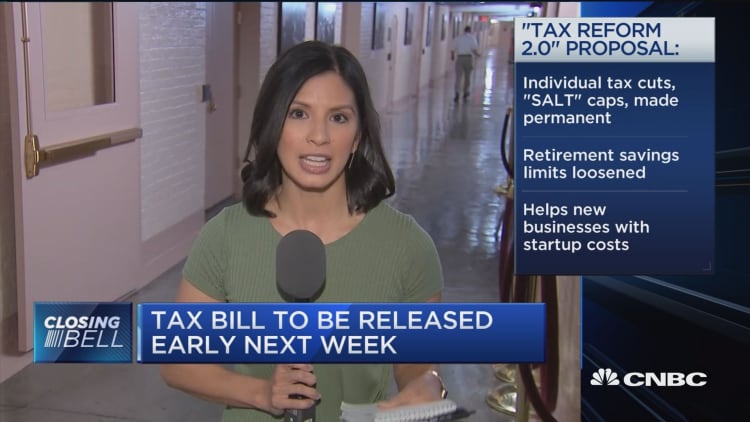

The House Ways and Means Committee released an outline of the provisions in its "Tax Reform 2.0" proposal on Thursday. The proposed legislation would make permanent the $10,000 cap on state and local tax deductions, as well as the individual income tax cuts.

The proposal also included new provisions for retirement accounts, including one that would allow people to continue contributing to their traditional IRAs beyond age 70½.

"Where I see a big benefit is if you're doing a backdoor Roth conversion and you're still working," said Ed Slott, CPA and founder of Ed Slott & Co.

Here's what you need to know.

IRA contributions

Under current rules, individuals can no longer contribute to a traditional IRA beyond age 70½. After that age, you must begin taking required minimum distributions (RMD).

Individuals can put away up to $5,500 in an IRA this year, plus $1,000 more if over age 50.

The age limit for contributions does not apply to Roth IRAs.

The proposed change to the tax law would permit savers to contribute to IRAs past age 70½, benefiting a growing population of older workers. You need to have earned income, however, in order to contribute to an IRA.

Under the current law, self-employed people can contribute to their Simplified Employee Pension (SEP) or SIMPLE IRA beyond 70½ if they're still working.

The proposed law would put W-2 employees on equal footing, allowing them to contribute to traditional IRAs.

The highlights of the proposal gave no indication that there would be changes to required minimum distributions.

Tax experts expect that savers would continue to make them, which is the case for self-employed individuals who are still working and use SEP and SIMPLE IRAs.

"It would be like a revolving door of money: You put money into the IRA and take it out as an RMD," said Jeffrey Levine, CPA and director of financial planning at BluePrint Wealth Alliance.

Backdoor Roth

Individuals who are 70½, working and earning too much money are ineligible to make direct contributions to a Roth IRA.

The applicable modified adjusted gross income limits to contribute to a Roth IRA in 2018 are $135,000 for singles and $199,000 for married-filing-jointly.

Under the proposed law, these older high-income workers can first make a nondeductible contribution with after-tax dollars to a traditional IRA and then convert the amount to a Roth IRA, said Slott.

This is known as a "backdoor Roth conversion."

Money in a Roth IRA grows free of taxes. You may also take tax-free withdrawals of the earnings in retirement, provided you've owned the account for at least five years and are over 59½. Your contributions can be withdrawn at any time.

Tax traps

Be aware that backdoor Roth conversions from nondeductible contributions can be tricky.

If you have other IRAs, including a SEP and SIMPLE IRAs, with pretax dollars in them, you could face income taxes based on the overall value of all the accounts. This is known as the prorata rule.

Further, if you're due to take an RMD from your IRA in a given year, you can't convert that amount, said Slott.

You must take the RMD from the IRA first, then make the Roth conversion.

"It'll give accountants a lot of work," Slott said. "They need to make sure not to convert the RMD. The money still needs to come out whether you do the backdoor Roth or not."

Roth IRAs themselves aren't subject to required minimum distributions.

Spousal IRA

Older savers who are married and filing jointly and who are still working may be able to fund spousal IRAs under the proposed rule.

Spousal IRAs allow the working spouse to contribute to the non-working spouse's IRA.

Under current law, those who are over 70½ are prohibited from making these contributions, so the proposal would open this opportunity up for them, Slott said.

WATCH: Tax Reform 2.0 proposal released by House panel