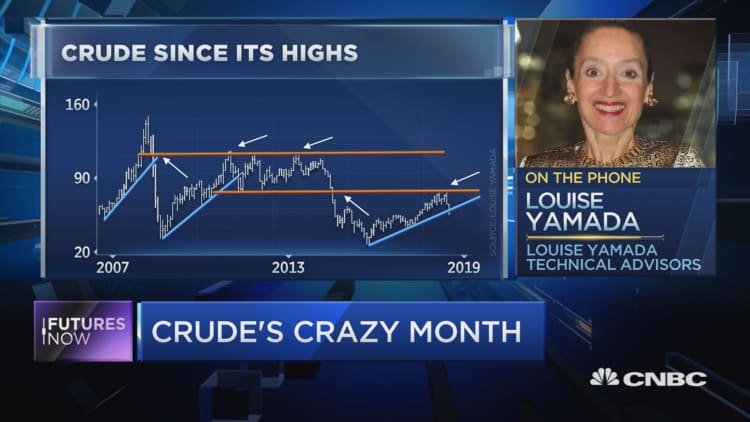

Oil prices pulled back sharply on Friday, after earlier rising on expectations that OPEC and its allies would agree to cut output next month.

Prices remain under pressure on concerns that the global market is oversupplied, with benchmarks posting a sixth straight weekly loss. An oil market sell-off has shaved more than a fifth off the Brent crude benchmark and slashed the price of U.S. crude by 25 percent since early October.

Brent 14 cents higher at $66.76 a barrel on Friday, after earlier rising more than 2 percent. It has been recovering for three sessions since hitting an eight-month low on Tuesday but still ended the week nearly 5 percent lower.

U.S. West Texas Intermediate crude futures ended Friday's session flat at $56.46 a barrel, briefly turning negative and falling $1.50 from the session peak. WTI logged its steepest one-day loss in more than three years on Tuesday. The contract fell 6.2 percent this week.

Ministers from the Organization of the Petroleum Exporting Countries meet on Dec. 6 in Vienna to decide on production policy for the next six months. They have to decide what to do about a growing surplus in world markets.

The United States imposed sanctions on Iran this month, asking international consumers not to buy its oil, and Iranian crude exports have fallen sharply in recent months.

But other oil producers have more than compensated for the lost Iranian oil and most analysts now see a significant supply surplus with inventories building, putting pressure on prices.

OPEC is widely expected to start trimming output soon, fearing a repeat of the 2014 price rout. This could produce a swift price rebound, some analysts say, especially if production falls further in Venezuela and Libya.

"We are likely from December onwards to have at least 1 million barrels per day (bpd) less of (Iranian) crude exports," Harry Tchilinguirian, global head of commodity markets strategy at BNP Paribas, told Reuters Global Oil Forum.

Tchilinguirian said he would not be surprised if Brent recovered to $80 a barrel this year.

Morgan Stanley warned that a cut by the Middle East-dominated group might not have the desired effect.

"The main oil price benchmarks - Brent and WTI - are both light-sweet crudes and reflect this glut," the U.S. bank said.

"OPEC production cuts are usually implemented by removing medium and heavier barrels from the market but that does not address the oversupply of light-sweet."

OPEC's de facto leader, Saudi Arabia, wants the cartel to cut output by about 1.4 million bpd, around 1.5 percent of global supply, sources told Reuters this week.

The Saudis would like Russia to cut output but Moscow has yet to commit to joint action.

Iraq resumed exporting oil from its northern Kirkuk oilfields on Friday, pumping 50,000-100,000 bpd, an oil ministry spokesman told Reuters. Some analysts had expected the volumes to be much higher, at closer to 300,000 bpd.

While OPEC considers withholding supply, U.S. oil production reached another record last week, at 11.7 million bpd, U.S. data showed.

The record output helped U.S. crude oil stocks to their biggest weekly build in nearly two years.

"Oil bulls, us included, have capitulated and we no longer see oil climbing to $95 a barrel next year," Bank of America Merrill Lynch said in a note.

U.S. energy firms this week added oil rigs for a fifth time in six weeks, keeping the rig count at its highest in over three years and crude production from shale basins at a record high.

Drillers added two oil rigs in the week to Nov. 16, bringing the total count to 888, still the highest level since March 2015, General Electric's Baker Hughes energy services firm said in its closely followed report on Friday.

— CNBC's Tom DiChristopher contributed to this report.