Oil prices rose on Thursday, after data showed inventory declines in the United States and as investors began to expect that the global oil market could have a deficit sooner than they had previously thought.

OPEC's output agreement with Russia and Canada's decision to mandate production cuts could create an oil market supply deficit by the second quarter of next year, if the top producers stick to their deal, the International Energy Agency said in its monthly Oil Market Report.

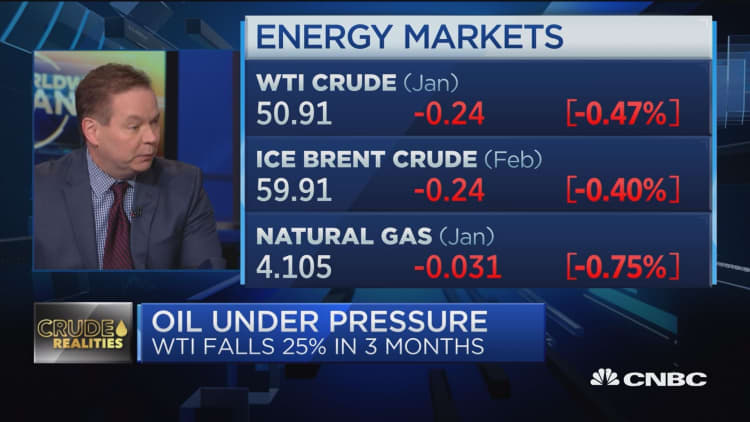

U.S. crude inventories at Cushing, Oklahoma, the delivery point for U.S. crude futures, fell by nearly 822,000 barrels in the week through Dec. 11, traders said, citing data from market intelligence firm Genscape.

Stockpiles fell by 1.2 million barrels in the week to Dec. 7, disappointing some investors who had expected a decrease of 3 million barrels. The data showed stockpiles jumping by 1.1 million barrels in Cushing during that week.

Benchmark Brent crude oil was up $1.19, or 2 percent, at $61.34 per barrel by 2:28 p.m. ET. U.S. West Texas Intermediate light crude ended Thursday's session up $1.43, or 2.8 percent, to $52.58.

"The market over the last week has attempted to stabilize and I still think that's what is happening today," said Gene McGillian, manager of market research at Tradition Energy in Stamford, Connecticut.

"For further weakness in the market you need to see even stronger signs that demand growth is going to deteriorate and supply will continue to increase."

Global oil supply has outstripped demand over the last six months, inflating inventories and pushing crude oil to its lowest in more than a year at the end of November.

OPEC and other big producers, including Russia, said last week they would try to trim surplus supply, agreeing to cut production by a total of 1.2 million barrels per day.

Still, Oil demand growth is slowing, OPEC says.

OPEC said on Wednesday that demand for its crude in 2019 would fall to 31.44 million bpd, 100,000 bpd less than predicted last month and 1.53 million bpd less than it currently produces.

Iranian Oil Minister Bijan Zanganeh said his country has no plans to reduce its oil production, but will remain a member of OPEC, the official news agency IRNA reported.

Factors such as production cuts and output losses elsewhere should keep markets tight in the first half, Jefferies analyst Jason Gammel said. But he added that U.S. production growth "will almost inevitably re-accelerate in 2H19 as incremental pipeline capacity is installed in the Permian Basin. This means that by early 2020 the market could move back into oversupply."

The United States, where weekly crude production has hit a record, is set to end 2018 as the world's top oil producer, ahead of Russia and Saudi Arabia.

Stock market investors worried about U.S.-China trade tensions breathed a sigh of relief as China made its first major U.S. soybean purchases in more than six months on Wednesday.

Crude future also drew support from indications that the trade war between the United States and China may be easing.

In a sign that China wants to lower trade tensions with the United States, the country made its first major U.S. soybean purchases in more than six months on Wednesday. Investors breathed a sigh of relief across broader stock markets.

— CNBC's Tom DiChristopher contributed to this report.