GitLab, a developer of code-sharing software, took the unusual step of announcing a specific date when it plans to go public — Nov. 18, 2020. The day is significant because it marks "five years after the first people got stock options with 4 years of vesting," the company says on its strategy page.

To get to the public markets, GitLab is leaning toward an equally unusual approach: a direct listing.

GitLab CEO Sid Sijbrandij has told board members that he prefers a direct listing over an initial public offering, and the finance department has pulled together a presentation for investors laying out the benefits, according to people familiar with the matter who asked not to be named because they weren't authorized to speak on behalf of the company.

GitLab is in talks with the big banks about its prospective offering but hasn't picked a lead yet or decided definitively which route to take, the people said. The company raised $268 million in a private round in September, giving it plenty of money to go public without an IPO.

"At this time we are considering all our options, IPO or direct listing in 2020," a GitLab spokesperson told CNBC in an email. "We want to go public next year as the market is well-aligned for us with massive opportunity and demand for our product."

Unlike an IPO, where companies raise money by selling new shares to public market investors, a direct listing entails simply registering to go public and then allowing existing investors to sell their stock.

Evangelists promote direct listings as a better way to go public because companies can get the same result without selling a bunch of new stock — and diluting existing shareholders and employees. IPOs offer a steep discount for new investors, who typically get the benefit of any immediate stock pop, while direct-listed stocks debut with market-based pricing. That makes them like every other equity and "almost every other financial asset," said venture capitalist Bill Gurley, one of the loudest critics of the traditional IPO process, in October.

The modern history of direct listings is short, consisting of exactly two case studies. Spotify took that route in 2018 and Slack followed in 2019. Both companies were well capitalized enough that they didn't need to raise money in an IPO. Neither has been a big win for public market investors: Spotify is trading slightly below where it closed on its first day in April 2018, and Slack shares are about 40% below their first-day close in June.

Despite their lackluster performance, the lawyers, bankers and venture capitalists who are closest to today's up-and-coming tech companies say we're at an inflection point, with many more direct listings to come. Greg Rodgers, a partner at Latham & Watkins who worked on the Slack and Spotify deals, predicted at a Goldman Sachs event in October that there would be at least five direct listings in 2020.

At the same time, more executives and directors at private tech companies are taking advantage of the renewed focus on the IPO process to consult with banks regarding the things they like and don't like about typical share sales. Top bankers, eager to maintain their advisory roles with the hottest companies, are getting more flexible with IPOs and showing their willingness to deviate from traditional offerings.

A 'pretty healthy pipeline' in 2020

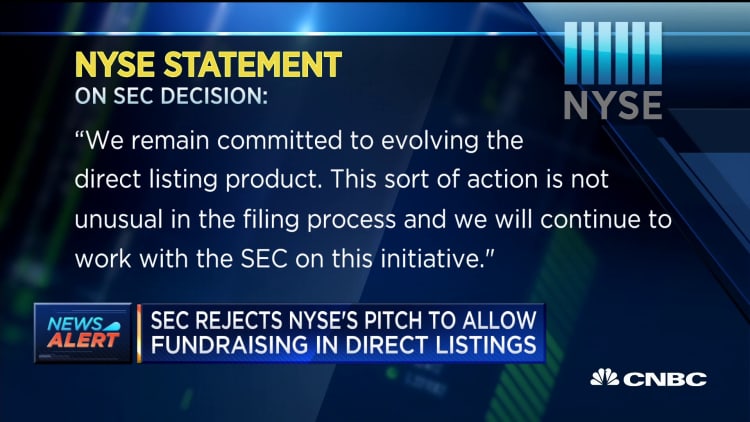

The biggest drawback to direct listings is that they currently offer no way for companies to raise fresh capital, eliminating the key reason for many businesses to go public. In November, the New York Stock Exchange filed paperwork with the Securities and Exchange Commission to change the rules so companies can simultaneously execute a direct listing and raise cash. The SEC rejected that proposal last week, and the NYSE said it will "continue to work with the SEC on this initiative."

But for companies that don't need the money — either because they're profitable or they've raised a war chest in the private markets — the direct listing has a lot of appeal. In IPOs, a select few big investment firms tend to get an outsized allocation, thanks to their longtime ties to investment banks, and often enjoy a big pop right out of the gate. The banks, in addition to their underwriting fees, also get an option to buy shares at the IPO price. In 2019 debuts like Zoom and CrowdStrike, which each jumped more than 70% on day one, and Beyond Meat, which climbed 163%, the companies left hundreds of millions of dollars on the table that they could have used for hiring and expansion.

Airbnb said it plans to debut in 2020 and is reportedly leaning toward a direct listing. Bloomberg reported in November that DoorDash is considering a direct listing, and the Financial Times reported last week that business software maker Asana, started by Facebook co-founder Dustin Moskovitz, is expected to go that route next year.

Other names discussed as potential 2020 candidates include Snowflake, a cloud infrastructure company, data backup vendor Rubrik and investing platform Robinhood.

Snowflake CEO Frank Slootman told CNBC's "Halftime Report" on Monday that he's preparing for a public offering and the only reason to do a direct listing would be if the company decides it doesn't need to raise money.

"The IPO is a price discovery process," Slootman said. "It's not perfect but it's a good process, time-tested. You can't say that about a DL."

Representatives from Rubrik and Robinhood declined to comment.

Momentum for the idea started to pick up last October after a seminar hosted by Benchmark's Gurley, which was attended by hundreds of venture investors and executives from late-stage start-ups. Manny Medina, CEO of software developer Outreach, flew from Seattle to San Francisco for the event, and told CNBC after hearing the presentations that he was going to start looking seriously at a direct listing for his company.

Mike Volpi, a partner at Index Ventures, agrees that the topic is coming up a lot more now.

"In every case, it's part of the conversation," said Volpi, who participated in several recent IPOs, including Zuora and Elastic last year. "Boards are not absolutely going one way or another. They're saying, 'Let's think about pros and cons.'"

Ran Ben-Tzur, a partner at Fenwick & West who specializes in public offerings, said he's hearing about a "pretty healthy pipeline of direct listings" for next year.

"Companies are going to start thinking about what's right for them and what makes sense for their circumstances instead of pigeonholing it into some traditional process that was set up many years ago and doesn't necessarily work for a specific company," Ben-Tzur said.

Getting a precise read on the 2020 pipeline is a challenge. While a number of companies have gotten the process rolling, few have absolutely committed to going public next year, according to about a dozen people involved in the talks. Most say they want to avoid going out in the back half of the year because of uncertainty around the 2020 presidential election results, and the different ways the market could react depending on who gets elected.

Banks showing 'tremendously more flexibility'

Bankers are starting to pay notice and considering more flexibility around the traditional IPO.

Goldman Sachs, Morgan Stanley and J.P. Morgan Chase have each held recent events on the benefits of pursuing alternative routes to the public markets. Topics included loosening the lockup period, so insiders and employees don't have to hold onto all their shares for six months after the offering while new investors trade in and out of the stock, and ways to limit the first-day pop.

In private conversations with companies, banks are talking about staggered lockup expirations that could allow for a certain percentage of shares to be sold after 45 days, 90 days, 135 days and so on.

"Every bank is talking about their willingness to do things in ways that would have been considered non-traditional eight months ago," said Lise Buyer, who worked on Google's IPO in 2004 and later founded Class V Group to help companies prepare to go public. "There is unquestionably tremendously more flexibility in the discussions now."

J.P. Morgan's Greg Chamberlain, who leads the bank's U.S. technology equity capital markets group, echoed that sentiment, telling CNBC that, "It's our job as advisors to clearly set out the different ways of becoming a public company and how to achieve these objectives."

William Connolly, head of technology equity capital markets at Goldman, said multiple options are on the table as his group works with companies to customize their offerings. Connolly said he's seeing enough interest in direct listings to confidently say there will be more next year than we've seen up to this point — so at least three.

He also expects the makeup of the issuers to change. So far, companies pursuing direct listings have been household names with big valuations: Spotify, Slack and Airbnb are all established brands, making it easier for them to appeal to a wider swath of investors.

GitLab, by contrast, is a niche product mostly used by developers. Asana, which makes workplace collaboration software, isn't well known outside of its limited user base.

"If you look at the first two listings, they were $20 billion-plus companies — that won't stay the same," Connolly said, in an interview. "There's been a broadening of the types of companies that are considering direct listings. They won't all be $20 billion-plus, they won't all be $10 billion-plus."

He said that if capital raising becomes an option, the direct listing will become that much more attractive.

"Right now, based on the regulatory paradigm, it will be companies that don't need money," he said. "As I think about next year, there will be one or two companies that don't fit that mold."

— CNBC's Alex Sherman contributed to this report.

WATCH: SEC rejects NYSE's pitch to allow fundraising in direct listings