In the last two months, oil has hit two very different first-of-its kind milestones. In April West Texas Intermediate, the U.S. oil benchmark, plunged below zero and into negative territory for the first time on record. Meanwhile May is shaping up to be WTI's best month ever, going back to the contract's inception in 1983—an astonishing turnaround month-on-month.

Improvements on both the demand and supply side of the equation have pushed prices higher. Data shows that people in the U.S. and China are starting to hit the road again, while producers around the globe have cut output at record rates in an effort to prop up prices.

The contract has jumped more than 70% in May and posted four straight weeks of gains, but some traders warn that the near-term outlook for oil remains uncertain, and that prices could head back into the $20s after settling around $33 on Friday.

Additionally, part of WTI's blistering rally this month is due to the historic low from which it bounced. Prices are still about 50% below January's high of $65.65, significantly cutting into profits for energy companies, which are often saddled with debt. A number of U.S. energy companies have already filed for bankruptcy protection, including Whiting Petroleum, which was once a large player in the Bakken region. If prices stay at depressed levels, there could be more casualties.

Still, the market has shown signs of rebalancing itself, and analysts say that if demand continues to improve and producers keep wells shut-in, the worst could be over for oil.

"The oil market rebalancing continues to gather speed, driven by both supply and demand improvements ... These improvements are taking out the risk of a sharp pull-back in prices although we re-iterate our view that the rebalancing will take time," Goldman Sachs said in a recent note to clients.

"We believe that the next stage of the oil market rebalancing will be one of range-bound spot prices with the most notable shifts being a decline in implied volatility as well as a continued flattening of the forward curve without long-dated prices rising yet," the firm added.

'Tide is turning'

While demand for petroleum products fell off a cliff in April, the outlook is improving as economies around the world begin to reopen. Raymond James, which has been tracking shelter-in-place orders, said that of the 3.9 billion people worldwide who have been under lockdown at some point since January, 3.7 billion, or 95%, have experienced some sort of reopening.

Chinese demand for oil in April rebounded to 89% of what it was a year earlier, according to IHS Markit, and the firm expects May demand to be 92% of 2019′s level. During February's low, demand in China, the world's largest oil importer, fell to just 40% compared to a year earlier.

In the U.S., all 50 states have begun the reopening process to varying degrees, which means people are once again driving. Data from the Energy Information Administration has shown an uptick in gasoline demand, although there's still a way to go before the pre-coronavirus levels are reached.

"All eyes are on demand ... this is mainly a demand problem," said Bernadette Johnson, vice president of market intelligence at Enverus. She sees WTI hovering around the $20s to mid-$30s mark in the near-term, as demand continues to come back. "We're expecting Q3 will look better from a supply/demand balance standpoint. You need a market that's in equilibrium to start seeing higher prices, and so Q3 is really the first quarter where we'll see that happen, because a lot of the demand is supposed to come back," she added.

Evercore ISI echoed this point, writing in a recent note to clients that supply will continue to outpace demand in the second quarter, but that by the third quarter the "tide will turn," at which point demand will exceed supply.

Record production cuts

On the other side of the equation, historically low oil prices forced producers to shut in production at a record rate. Beginning May 1, OPEC and its oil-producing allies took 9.7 million barrels per day of production offline, after agreeing to the deepest production cut in history during an extraordinary, multi-day meeting in April.

Then, earlier in May, Saudi Arabia said that, beginning June 1, it would voluntarily cut an additional 1 million bpd, on top of its portion of the cuts agreed to by OPEC+. Kuwait and UAE were among the other cartel members that followed suit and said they would also exercise additional cuts.

Norway, Canada and the U.S. are among the other nations that also announced well shut-ins as oil prices plummeted.

The latest figures from EIA show that U.S. production has dropped 1.6 million bpd below the March high of 13.1 million bpd. Exxon, Chevron and ConocoPhillips are among the companies that have scaled back operations.

Darwei Kung, head of commodities at DWS Group, said that the rebound in oil prices is riding on lasting production cuts. But if prices rise enough that producers, including those in the U.S., ramp up output again, there's a chance that OPEC+ could abandon its cuts in an effort to gain market share.

"We view the most important consideration for the supply part of the equation is the ability for OPEC+R countries to stay with policy to maintain price stability," Kung said. "In doing so, they have to commit to the production cuts even if a third party, such as [the] U.S., increase production as the oil price recovers."

Second wave of coronavirus cases?

As the oil market begins to re-balance itself, traders say another big risk is a possible second wave of coronavirus cases and subsequent return to shelter-in-place restrictions. Francisco Blanch, head of global commodities at Bank of America, said this would have "devastating consequences."

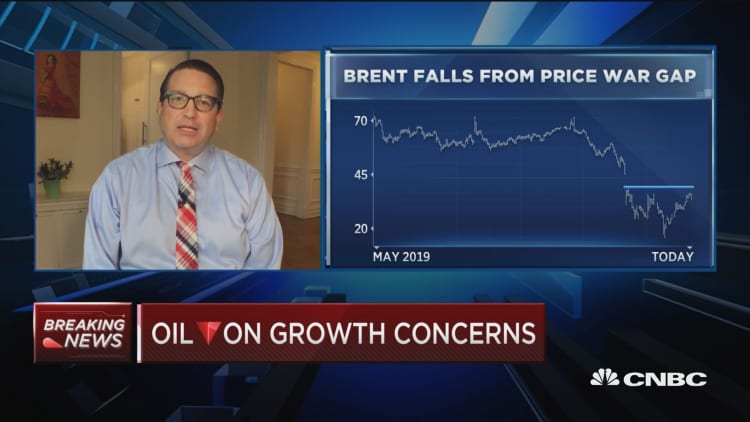

The firm said that the rebound in prices has come faster than expected, and forecasts WTI averaging $32 per barrel this year and $42 in 2021. Bank of America expects international benchmark Brent crude to average $37 this year. The contract settled at $35.13 per barrel on Friday and is also coming off a fourth straight week of gains.

"It is not clear if the rest of the world [outside China] can successfully prevent major reoccurrence of COVID-19 spread, given the disparity between countries or states within a country on containing the disease. A second wave of infection can change the recovery for oil demand significantly," added Kung. He noted that souring relations between the U.S. and China could be another headwind for oil going forward.

'Not out of the woods'

The WTI contract that plunged into negative territory in April was for crude that was set to be delivered in May. With storage rapidly filling, including in the U.S. hub in Cushing, Oklahoma, no one wanted to take delivery of oil as demand was expected to remain depressed throughout May and into June.

Enverus' Johnson said this was the "painful period" needed to force companies to shut-in production, and that prices dipping into negative territory was the market functioning correctly. "We're definitely not out of the woods," she said, before adding that the set-up looks much better in the back half of the year.

Barclays has a similar forecast, writing in a recent note to clients that oil prices will "remain volatile as participants try to find a path through the extreme distortions caused by a fall off the cliff in demand and a lagged supply response." For 2020 the firm sees WTI averaging $33 per barrel, before rebounding to $50 per barrel in 2021.

- CNBC's Michael Bloom contributed reporting.