The Fed has gotten high marks for moving aggressively to unlock credit markets and keep money moving in an unprecedented crisis. What's next is now the challenge.

How much the Fed will reveal about its future intentions and what it says about its view of the economy could be the keys to this week's two-day meeting, and bond market strategists say a number of outcomes could be market moving.

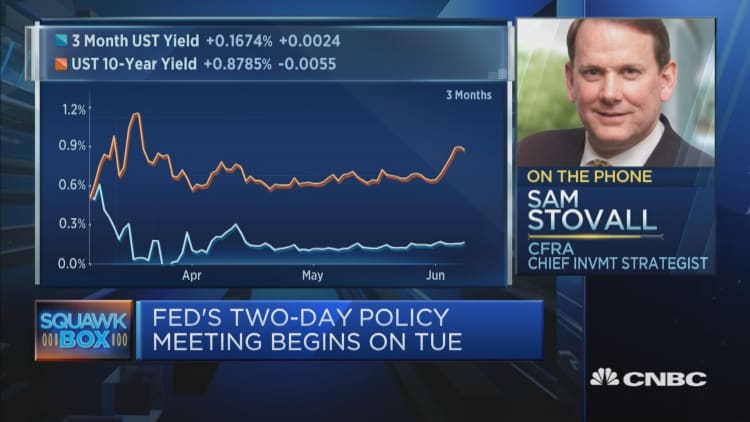

The Fed is not expected to take any action on rates or policy at its meeting, which ends with a statement Wednesday afternoon and is followed by a briefing by Chairman Jerome Powell.

Powell has already taken more actions and at a faster pace than any chairman before him. The Fed has slashed benchmark interest rates to near zero and announced numerous programs to help different parts of the markets and economy.

They include programs to provide lending programs and support municipal bonds, mortgages, commercial paper and corporate bonds. The corporate bond facilities have barely launched but have helped ease conditions so much that companies tapped about $800 billion in the investment grade market since the Fed announced the programs in late March, a confidence booster for the stock market.

When the Fed issues its statement Wednesday, it is expected to release its quarterly economic and interest rate forecasts, which it declined to do at the height of the crisis in March. Now, the Fed has a chance to describe what it thinks the future path might look like, provide forecasts and possibly add clarity about its programs and future steps.

""I think the Fed will keep leaning on the side of being accommodative. In no way will it signal an end to that and in no way will it signal reluctance to be an implicit partner with the U.S. Treasury in supporting the proper and full functioning of various markets, including the Treasury market," said Tony Crescenzi, vice president and member of Pimco's investment committee.

The Fed is not likely to give too much detail on its future plans, because forecasting the path of the economy is so uncertain given its rapid collapse. Economists expect to see a contraction of more than 30% for the second quarter, but they vary on how much and if the third quarter bounces back.

"The Fed wants to be careful about providing it until it has a better sense of the outlook. Friday's payroll data shows the outlook could go either way, though the base case is for a prolonged recovery," said Crescenzi. There were 2.5 million jobs created in May, according to the government's employment report, a surprising contrast to economists' forecast for a loss of 8.3 million jobs.

But some believe the Fed's comments, no matter how carefully crafted, could impact markets. The stock market bottomed March 23, as the Fed announced a battery of new programs, and the S&P 500 is now up more than 47% since then. The Treasury market, until last week, stayed in a ultra-low range with the 10-year yield below 0.75%. As jobs data improved, the 10-year yield, which moves opposite price, jumped to 0.95% last week before backing down. It was 0.82% Tuesday.

No taper tantrum

Markets appear most sensitive to any developments on the Fed's open-ended bond purchasing program. It is currently buying $4 billion in Treasurys a day, and bond market pros have been hoping for a statement from the Fed giving some set size and duration for the program.

The Fed updates its purchase intentions on a short term basis, and the market has been looking for a more definitive plan, as the Fed had provided with the quantitative easing programs during the financial crisis.

Evercore's Fed watchers said they see the Fed "staying dovish to prevent a taper tantrum," as it did when it pulled away from quantitative easing in 2013. They said that without a clear commitment to maintain a high level of purchases, the market is interpreting the Fed as "happy" with the size and speed of the movement in Treasury yields.

"This is a risky game, when market participants know that Treasury issuance of longer dated securities will remain high, putting upward pressure on duration holdings and the term premium," with another potential $1 trillion coming from Treasury for the next fiscal stimulus program, the Evercore analysts wrote.

Congress is considering another stimulus program, and the Treasury has already dramatically expanded its auction sizes including the introduction of a 20-year bond. The Fed has purchased Treasurys at a rapid pace to help keep markets liquid and it has been slowing down those purchases, but its balance sheet has already ballooned to over $7.1 trillion.

"We think they've still got another $3 trillion or so that the balance sheet would go up," said Rick Rieder, head of global fixed income chief investment officer at BlackRock. "One of the things that's going to be really important for interest rates is as the Fed reduces the amount they are buying the Treasury keeps issuing."

Rieder said the amount of debt the Treasury is increasing, in 10-year equivalents, is up 72%. "The amount of supply at the long end of the curve is significant. That's going to be one of the keys," he said.

There has been speculation that the Fed could announce a program at some point to control the yield curve and prevent interest rates from rising too much, as the economy starts to improve.

"I think we're going to hear generalities of where they're going, and they think they'll be at this low rate for an extended period of time," said Rieder. "I don't think we're going to get a specific yield curve control. I don't think they want to go down that path unless things get significantly worse."

John Briggs, head of strategy at NatWest Markets, said the lack of an announcement from the Fed on its Treasury purchases could put pressure on long end rates. He is looking for the Fed to announce some specifics on how much Treasury debt it will purchase and at what durations.

"Say they announce nothing, I think think yields can move back up ... [10-year yields] went all the way to 95 basis points and fell back to 80," said Briggs. "I think they could go back and test 95, and all the way to 100 because the Fed would not be supporting the long end."

Briggs said, in what he calls Covid QE, that the Fed has only made 13% of its purchases in 20- to 30-year Treasury securities. "If they bring it up to 20%, then clearly the Fed doesn't want the long end to rise. If they do this, I think the correction off of higher yields could continue," said Briggs. In the Fed's QE3 program, 27% of its purchases were at the long end, he said.

Interest rate forecast

Jon Hill, senior fixed income strategist at BMO said the Fed's forecast itself may be market moving.

"The point in March was there was so much uncertainty, it would have been harmful to put out a best guess. I expect that we've had enough data, and they've put the staff economists on this for a few months. Now they should at least feel comfortable putting out a best guess and what policy will be appropriate," he said.

Hill said it would be important to see how quickly the Fed sees the unemployment rate dropping from the reported 13.3%. Some Fed watchers say the policymakers could use a higher number as a current base simply because of reporting difficulties around the government's number.

"How quickly does unemployment get back to 5%? Is this a few months, quarters or is this a few years? And the monetary response is very different to each of those," said Hill. "They've been very clear about the uncertainty. The word uncertainty showed up 21 times in the Beige Book. Last Friday, they had a 10 million surprise in nonfarm payrolls. How do they forecast that?"

The Fed provides its interest rate guidance in a so-called dot plot, a chart with anonymous entries from the 17 Federal Open Market Committee officials. "It will be interesting to follow the dots. I don't think you're going to see a negative dot, but it's possible," said Rieder. Powell and other Fed officials have said they were against negative rates.

Briggs said the market may look past any interest rate forecasts because the outlook remains uncertain, and longer term forecasts are likely to change.