Life gets a bit more complicated when you're in your 30s.

You may get married, have children or buy a house. You may also still be carrying student debt. On top of it all, you are supposed to be putting money aside for retirement.

"Retirement is going to come for all of us eventually," said certified financial planner Lauryn Williams, a four-time Olympian and founder of Dallas-based Worth Winning, which offers virtual financial services.

"Once you pass through your 20s and you are well into your 30s, time becomes of the essence."

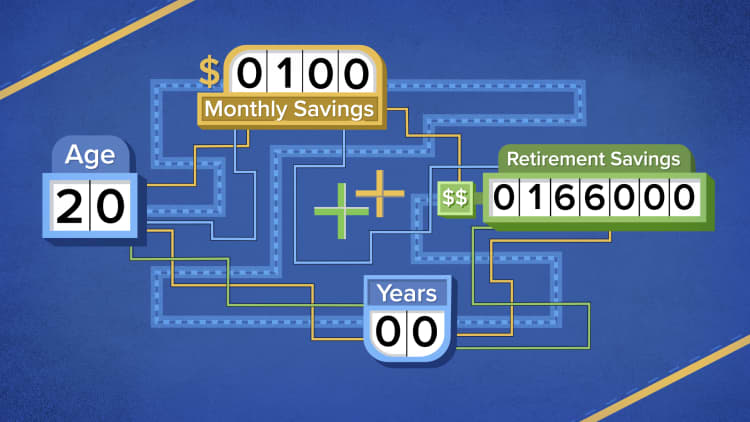

In order to retire comfortably, Fidelity Investments recommends that, at age 30, you should try to have one time your current salary in savings and two times your salary by age 35. By the time retirement comes around at 67, you should have 10 times your final salary saved, the firm noted.

More from Invest in You:

A majority of Americans have no money saved for their children

Here's what you need to know about moving in retirement

How to negotiate the best package for early retirement

When it comes to actual savings, the average 401(k) balance for those ages 30-39 is $42,700, Fidelity said.

While people know they have to save, they may not be planning properly — if at all, said Tyler Huck, an Alpharetta, Georgia-based financial advisor for Oxygen Financial, a financial advisory and wealth management firm specializing in younger generations.

"I don't think there are enough people that are tracking, 'What do I really need to be saving? What rate of return do I need to make on my investments?" he said.

'You get addicted to seeing it grow'

Jay Revell, 33, knew at a young age that he needed to save for retirement. He grew up in a house where finances were discussed around the dinner table.

When he graduated in the spring of 2009 at the age of 22, he landed a local government job in Tallahassee, Florida, and started investing in a 401(k).

He also started putting $50 a month into a Roth Individual Retirement Account, which was made after tax. Therefore, all future withdrawals are tax-free.

"You get addicted seeing it grow," said Revell, who now works for the Greater Tallahassee Chamber of Commerce. "Every year I just kept adding to it and adding to it.

"It is one of the best things I've ever done."

He's now married and has a 2½-year-old daughter, with another on the way. He also has a couple of side hustles to fund his retirement account: He's the author of the book "The Nine Virtues of Golf" and has a media company that focuses on the golf world.

Revell is also now maxing out his Roth IRA, has a 401(k) with his current job and an IRA for the 401(k) balances he rolled over from his previous jobs. He calls his portfolio "healthy and robust."

How to start

If you didn't start in your 20s, don't fret — but do try to get moving. If you've started saving, but haven't made a plan, come up with one.

The first thing to do is to understand your cash flow, said Williams, a member of the CNBC Financial Advisor Council.

"If you go and just spend time going over your budget one good time and get an understanding for the recurring expenses, you'll find the black hole of savings," she said.

Once you see how much you are able to put aside, automatically put that money into savings.

If you don't have an emergency fund, make sure some of that money goes into one. Williams suggests either building a $5,000 to $10,000 "buffer," depending on your income, or three to six months of take-home pay.

If you have a specific retirement savings goal in mind, run the numbers. Determine what you'll need to live on in retirement, and then calculate how much you need to put aside to meet your goal.

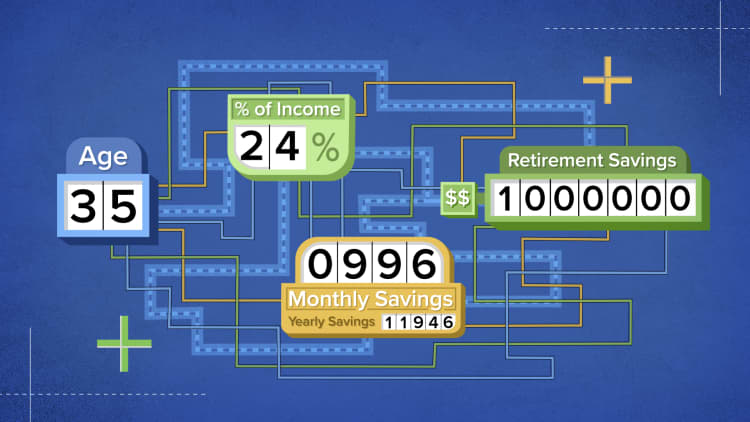

For example, if you are 35 years old with no savings and an annual pre-tax income of $60,000, you'll have to save $750 a month, or 15% of your monthly income, to have about $1.03 million saved by the time you are 67, according to NerdWallet's retirement calculator. The calculator assumes a 3% inflation rate, salary increases of 2% a year, and a 6% rate of return before retirement.

Debt vs. savings

If you have debt, you can find a balance between paying it off and saving towards retirement.

Take student loans. If it is a federal one, you don't have to make payments until January 2021, thanks to the executive order signed by President Donald Trump in August. You can also pursue debt forgiveness or look into an income repayment plan, which is based on what you earn and has loan forgiveness in 20 years or 25 years.

In the case of an income-driven repayment plan, stick with a 401(k) or IRA, which have pre-tax contributions, so that your adjusted gross income will be lower, Williams suggested. That, in turn, will lower your student loan payment.

You want to get really aggressive about paying down your student loan debt, but you don't want to sacrifice savings.Lauryn Williamsfounder of Worth Winning

You'll be putting money away for retirement and you get rewarded for doing so, she said.

If you have a private student loan, you can look into refinancing to get a lower rate, Williams said. Just make sure to pay over the minimum amount due.

"You want to get really aggressive about paying down your student loan debt, but you don't want to sacrifice savings," Williams said.

401(k)

If your company offers an employee-sponsored plan, at least do the employer match.

However, "saving 3% of your income is not going to be enough to get you to retirement," Williams said.

So, try to go as high as you can and have a plan to reach the maximum contribution amount in two to three years, she said. For 2020, that is $19,500.

Huck advises setting up an automatic contribution increase of 1% every year.

Your goal should be socking away 15% of your salary, which can include your employer's match, he said.

Roth IRA

If you meet the income requirements, a Roth IRA may be a good way to save for retirement, many experts advise.

If you are married and filing jointly and have a modified adjusted gross income of $196,000 a year, you can contribute up to the annual limit of $6,000. You can contribute a reduced amount if your income is between $196,000 and $206,000.

"People are really going to enjoy taking that money tax-free in retirement, but it is not one-size-fits-all," Williams said.

If $6,000 is a small percentage of your income, then make sure the Roth is not your only retirement savings, she said. If it is a large percentage, then the Roth may be all you need.

Again, if you have an income-based repayment plan for your federal student loan, a Roth may not be right for you since it doesn't decrease your adjusted gross income, she said.

Pay yourself first

If you have small children, you'll also want to provide for them. That may have you thinking about a college savings account.

However, if you can only do so much saving, make sure to focus on your retirement before your child's education, Huck said.

"When you decide to retire, you just can't go to the local bank and take a loan out," he said. "A child, if there is not enough saved for education can go to the bank and take out a loan," he said.

SIGN UP: Money 101 is an 8-week learning course to financial freedom, delivered weekly to your inbox.

CHECK OUT: 'Nobody ever got rich just by saving money,' says early retiree: Here's how you do it via Grow with Acorns+CNBC.

Disclosure: NBCUniversal and Comcast Ventures are investors in Acorns.