Few expected that we'd emerge from the pandemic with a massive spike in energy prices, but here we are. And just like in the stagflationary 1970s, surging oil prices--exacerbated by foreign wars--are proving to be one of the biggest headaches for households and policymakers. They're depressing consumer sentiment, factoring into rising inflation expectations, and undermining hopes for a "Roaring '20s."

And they're not going away anytime soon. Those who insist that spiking oil prices are a one-off caused by Russia's invasion of Ukraine are missing the fact that global supplies are tight for a variety of reasons, many of them structural, while demand has soared.

Pre-pandemic, in 2019, oil was "a pretty balanced market," notes energy investor Stan Majcher, of Hotchkis & Wiley. Global demand was around 100.3 million barrels a day; supply was around 100.6 million barrels, and that allowed for a slight inventory build of 0.3 million barrels to keep markets smoothly functioning. The U.S. benchmark West Texas Intermediate crude oil price spent most of the year in the mid-$50s per barrel, translating to around $2.50 per gallon at the gas pump.

Fast forward to today, and where are we? Intrinsic demand is thought to be around 103 million barrels a day now, owing to 1% per year global population growth, plus increased wealth--and demand should keep growing at roughly that pace. But supplies aren't nearly keeping up. We're currently producing around 100.6 million barrels (reflecting the loss of about a million barrels from Russia), and the resulting spike in prices is already constraining demand to around 101 million barrels, according to Majcher.

The result is a market that for the second straight year is under-supplied, and drawing down inventories as a result--on top of the drawdown in strategic reserves approved by political leaders to try and lower prices. Bank of America is already warning that global oil inventories have fallen to a "dangerously low point," with certain gasoline and diesel supplies in particular at "precarious levels" as we head into peak U.S. driving season. U.S. oil inventories are already 14% below their five-year average, BofA notes, while distillates (like diesel) are 22% below.

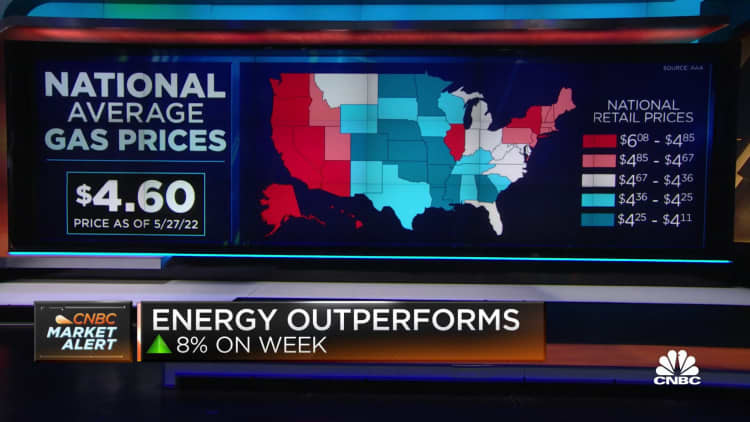

The upward pressure on diesel and jet fuel prices in particular is getting attention in the White House, Amrita Sen of Energy Aspects told Squawk Box yesterday. Diesel prices are up a whopping 75% from a year ago, and the spread between diesel and gasoline prices has also widened considerably. The high cost is creating huge strains on truckers and the supply chain; the Northeast "is quietly running out of diesel," FreightWaves warned two weeks ago.

In fact, Amrita said she wouldn't be surprised if the White House moved to limit diesel exports, noting "ahead of the midterms [they'll] want to be seen as doing something." She warned it probably wouldn't lower prices or help boost supplies, though, because the Colonial Pipeline (yes, that one) which runs fuel from the Gulf to the East Coast is already full and can't take more supply, and using more ships isn't an option because the White House is unlikely to waive the Jones Act, which requires using U.S. ships, which are also in shortage.

Kyle Bass said counterproductive moves by politicians--including in the U.K., which yesterday unveiled a $6 billion "windfall tax" on energy companies to subsidize fuel subsidies and direct payments to low-income households--are one reason he expects energy and food prices to remain stubbornly high even after the recession he predicts is coming. Britain's moves threaten to worsen energy supplies while increasing demand, exacerbating the very problem we're in, he warned.

Indeed, I asked value investor Abhay Deshpande earlier this week why he wasn't more bullish on energy right now, with the sector up a whopping 40% since January and the expectation of high prices for the foreseeable future. Political risk, basically, was his reason. "I am of the view that by the end of the summer the Biden administration will reinstitute the export ban on oil," he said. "That creates a lot of uncertainty when we're investing in the oil space."

That uncertainty could undermine America's ability to ramp up supplies in order to try and fix the chronic global shortage. The oil and gas industry was decimated by the shale bubble bursting last decade, and that reticence plus labor and supply shortages are keeping it from more quickly adding to capacity now. The possibility of an external hit like a windfall tax, export ban, or other such political measures risk keeping potential suppliers on the sidelines.

The U.S. has already increased supply to above pre-pandemic levels, no small feat, and should gradually bring more supply online barring such interventions, Majcher says. But getting more OPEC supply "is a risk," he warns; they're already "struggling to hit quotas," and much higher output would require sanctions relief for Iran. As for Russia, its supply loss is something in the range of half a million to 1.5 million barrels a day, he estimates--a big deal in a market this tight.

Bottom line, if global supplies can't keep up with demand for 103-million-barrels-a-day and counting, higher prices will have to choke off demand. Otherwise, supplies will continue to be drawn down until the risk of shortages becomes real--threatening the return of rationing and gas lines. High prices, in other words, are the cost of not running out of fuel entirely; if politicians try to blunt the hit by absorbing the cost, they're simply changing who pays (the government), instead of solving the problem, and risk running down supplies entirely.

The best-case outcome is a rapid return of Russian supplies, or some other surprise source (Saudi Arabia?) large enough to move the needle. The best thing the U.S. energy industry could do right now is step up and announce a "whatever-it-takes" effort to boost production--but that would risk destroying profits and permanently alienating its future capital base, and would also require a massive lift by politicians to help actually move the product via pipelines, ships, or some other measure.

So it's hard to see how energy prices get back to "normal" anytime soon, and the risk of bigger price spikes and worse supply problems looms very large this summer.

See you at 1 p.m!

Kelly