Revolution accelerated: How digital transformation is shaping the future of banking

REVOLUTION ACCELERATED

HOW DIGITAL TRANSFORMATION

IS SHAPING THE FUTURE

OF BANKING

Like all businesses, banks have had to act fast to respond to the unprecedented human and economic impact of Covid-19.

First, they needed to keep the lights on and ensure business continuity. Second, they had to meet the changing ways customers wanted to engage. Finally, they sought to balance their business priorities with a responsibility to support society. Previous crises cast the banks as part of the problem - this time they are part of the solution.

Banks who have embraced modern banking technology have fared better in meeting these challenges. They’ve moved seamlessly to remote working, kept up service for their customers, coped with huge increases in demand and quickly adapted their products. In contrast, banks using legacy ‘spaghetti’ software have struggled.

A case in point is Virginia-based Atlantic Union Bank. When the coronavirus hit, supporting small business clients was the bank’s top priority. And through the US government’s Paycheck Protection Program (PPP), they had the chance to make a real difference.

It was some task – with stringent requirements, soaring demand and huge application volumes. But through a new digital loan portal – built with Temenos – Atlantic Union Bank stepped up.

The bank approved 6,500 applications – totalling $1.4bn small business funds – in just 13 days. When the program wrapped up, they had helped around 200,000 SME employees.

Covid-19 has accelerated the need for modern banking technology, but it didn’t create it.

Before coronavirus, the 2020s were already being framed as the decade for digital in the banking industry. Banks’ return on equity were too low and their cost-income ratios were too high. Meanwhile, regulation like open banking was disrupting the industry and increasing competition from new entrants like the GAAFAs (Google, Amazon, Alibaba, Facebook, Apple).

Providing seamless digital customer experiences was therefore already a ‘must’.

Every year, Temenos partners with the Economist Intelligence Unit (EIU) for a global study on the future of banking. More than 300 banking leaders are interviewed from retail, commercial and private banks. Over half of these are at C-suite level.

In 2020, the study took place amid the Covid-19 crisis. The results give a fascinating insight into banking leaders’ approach during these unprecedented times. But they also show how they see their industry in the years to come.

And the findings suggest three trends which will shape the future of banking:

Two thirds of respondents to our report said new technologies will have the biggest impact in banking over the next five years. This represents a 57% increase on last year’s figure.

CWB Financial Group (CWB) views explainable AI (XAI) as a key differentiator in the digital experience they’re building for small- and medium-sized business clients across Canada. Using Temenos’ patented XAI technology, CWB will soon become the first bank in Canada to provide clients with fully-informed, explainable AI-automated insights into their financial activities.

Bank customers want to know what drives the decisions banks make when it comes to their business or personal finances and regulators are increasing calling for explainability, too.

This is one reason that ‘regulation around new technology’ was named by banking leaders as the second most impactful trend for the industry over the next five years.

Cloud and SaaS is another technology seeing increased demand from new players and established banks.

Itaú, largest bank in Latin America, is using these advantages to implement a front-to-back digital transformation of its international private bank. It’s using Temenos technology to manufacture and distribute banking products – deployed on Temenos SaaS. With Temenos’ cloud native, cloud agnostic technology, Itaú will create a new universal, attractive and user-friendly digital experience for its clients that is scalable as the bank grows.

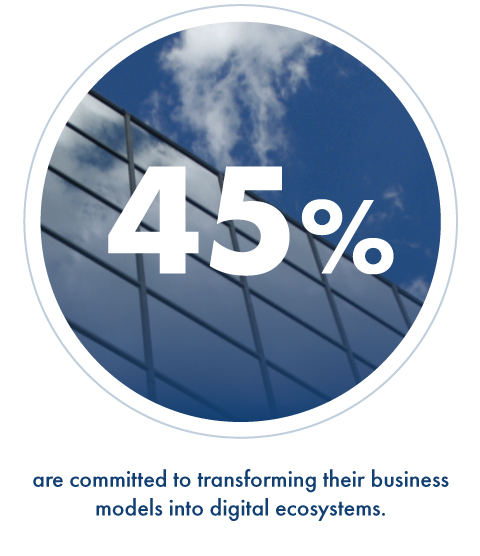

Digital transformation is changing banks’ business models.

Over the past few decades, technology has had an evolutionary effect on banks’ business models. First, services moved out of the branch and onto the internet. Then banks went mobile - with devices giving access to their services alongside the rest of our modern lives. But the services themselves didn’t change, only the method of access.

Ecosystems build entirely new customer experiences. While mobile saw banks become present in our everyday lives, ecosystems integrate our everyday lives with banking. Customers interact with the products and services they need through their banking apps. These are based on intuitive, self-learning software, which allows offerings to be enhanced and added in response to customer needs. Ecosystems bring many key elements of modern banking technology – such as cloud, explainable AI, and open APIs – together into one seamless user journey.

World Bank data shows that visits to branches have been steadily declining globally over the last decade. As a result of coronavirus, customers are now more concerned about visiting their branch, and so even more people are willing to try digital applications.

This combination of pandemic and increasingly transformative advanced technology has led a majority of respondents (59%) to our survey with the EIU to state that traditional branch-based banking model will be dead in just five years. That’s a 34% increase from last year.

Temenos Infinity Engage is a digital front office solution that allows customers to maintain a relationship their trusted advisor virtually. It lets banks retain an all-important human touch, take pressure off call centers and resolve customer issues faster. Banks using Temenos Infinity saw customer engagement increase by up to 300% on their apps in 2020, with the fastest growing segment being among baby boomers and Gen Xers.

The current environment is undoubtedly challenging for banks. But they have the capital, customer relationships and customer data. They are regulated. And most importantly: they still enjoy their customers’ trust.

In short, banks are best-placed to succeed if they commit to end-to-end digital transformation. That means a fully digital front office which creates hyper-personalized experiences and ecosystems. And a back office driving efficient operations and rapid innovation.

Temenos offers banks the winning combination of game-changing advanced technology with rich functionality. Over 3,000 banks in more than 150 countries use Temenos technology.

The Temenos Value Benchmark shows what can be achieved. Our top performing clients achieve market-leading cost-income ratios of 26.8%. That’s twice as good as the industry average. Their returns on equity are 29.0% — three times better than the industry average.

By embracing modern banking technology, banks can support their customers today, create new value for the future and drive new levels of future growth.

It’s a unique opportunity to discover more about how banking leaders are seizing it.

Temenos AG (SIX: TEMN) is the world’s leader in banking software. Over 3,000 banks across the globe, including 41 of the top 50 banks, rely on Temenos to process both the daily transactions and client interactions of more than 500 million banking customers. Temenos offers cloud-native, cloud-agnostic and AI-driven front office, core banking, payments and fund administration software enabling banks to deliver frictionless, omnichannel customer experiences and gain operational excellence.

Temenos software is proven to enable its top-performing clients to achieve cost-income ratios of 26.8% half the industry average and returns on equity of 29%, three times the industry average. These clients also invest 51% of their IT budget on growth and innovation versus maintenance, which is double the industry average, proving the banks’ IT investment is adding tangible value to their business.